In the United States where credit scores are a critical factor in determining whether you are approved or denied for a mortgage, auto loan or student loan, having good credit is not a nice-to-have — it’s a near necessity.

Despite the value credit offers, millions of consumers still lack access to this financial resource.

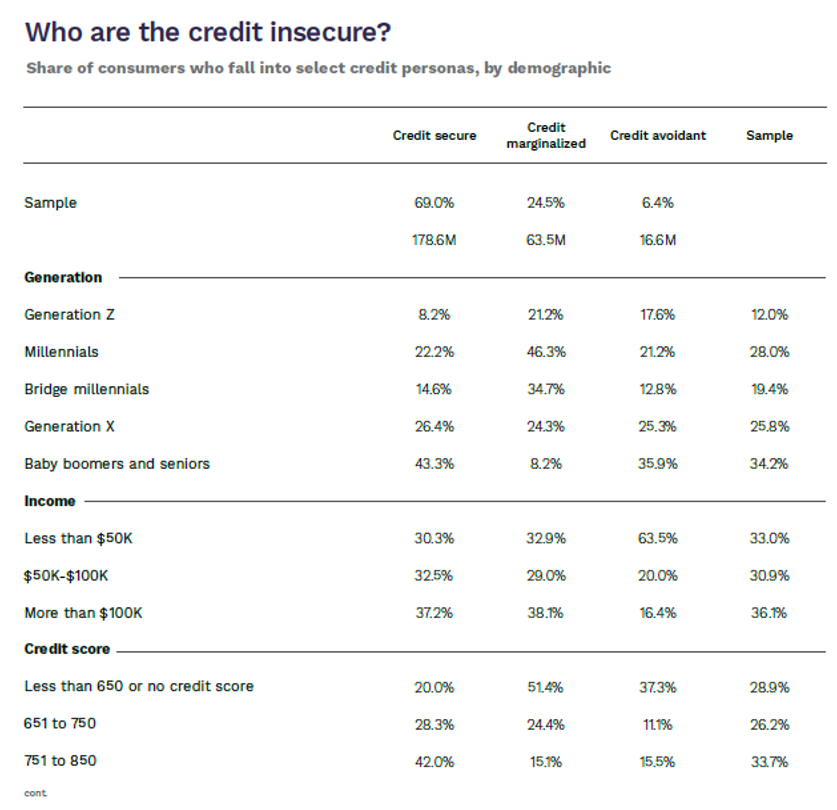

For “How Credit Insecurity Is Changing U.S. Consumers’ Borrowing Habits,” a PYMNTS and Sezzle collaboration, nearly 2,700 consumers examined nine distinct credit-related actions and identified how those actions contributed to boosting credit scores. Consumers were then grouped into three categories: credit secure, credit marginalized and credit avoidant.

Findings captured in the report showed that approximately 80 million consumers, or one-third of the population, have experienced some form of credit insecurity in the past year.

Among these credit insecure consumers, about 25% or an estimated 63.5 million are credit marginalized individuals who have been rejected for credit products at least once in the past year, likely driven by a change in their finance situation or a decline in their credit score. As a result, they are more likely to face difficulty qualifying for new credit products and resort to high-interest loans.

Credit marginalized consumers are also more likely to have overdue payments on payday loans and high-interest credit builder loans, further exacerbating their financial challenges.

They are less likely to apply for new credit products due to low credit scores and a fear of rejection. The lack of understanding of how to improve credit scores and qualify for credit products compounds the issue, with only a small percentage of consumers having a good understanding of credit-related actions.

The data also revealed that millennials make up nearly half of the credit marginalized group, at 46.3%. Bridge millennials — the cusp generation representing older millennials and the youngest members of Generation X, generally considered to have been born between 1980 and 1989 — come up next, making up about 35% of this cohort.

Baby boomers and seniors, on the other hand, make up less than 10% of this group, likely because of their experience managing fixed or lower incomes, as well as their reduced engagement in applying for credit.

In terms of gender, men account for 61% of the credit marginalized cohort, “possibly because men are still the primary domestic breadwinners and more likely to apply for credit,” the study found.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More