One data point does not a trend make.

And when it comes to consumer sentiment, you’d be remiss in thinking that things are — over the long term (and we’re talking a few years) — on an upswing.

The U.S. Conference Board’s Consumer Confidence Index got a boost in data that was just reported this week, where the reading rose from 102.5 to 109.7 in June over May’s level. That’s the highest level seen since January 2022. The Expectations Index rose to 71.5 to 79.3, but, we note, remained below an 80 reading, which tends to be a level that is associated with recessions projected to take shape over the next 12 months. Elsewhere, the 12-month forward inflation expectations fell to 6% in June, the lowest reading since the end of 2020.

But if we start to connect other data points, a less sanguine picture emerges. Another measure of consumers’ outlook, via the University of Michigan consumer sentiment measure reported via the St. Louis Fed’s FRED system, the latest reading of economic conditions, for April, was 63.5, which was actually down from 101 in February 2020, the month before the pandemic hit. The economic outlook — which projects out over 12 months — was 50 in May, down from 60 in April, and down from 61 at the end of last year.

Bringing the Data Together

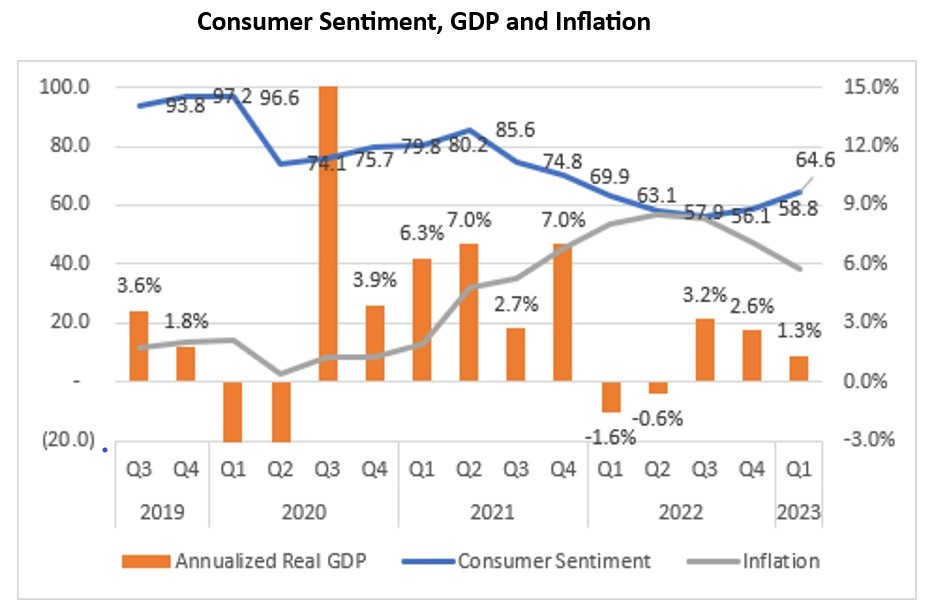

The chart below, as detailed by PYMNTS, brings together a range of economic data, and plots sentiment alongside official inflation readings and gross domestic product. And the data shows that when inflation is below the 2% benchmark that is most commonly used by the Fed as a target, sentiment is driven more by the GDP. It decreased during the acute economic problems related to the early days of the pandemic. However, as GDP growth returned, so did sentiment, at least until inflation exploded through the 2% benchmark and consumers noticed.

Only recently has sentiment been coming off of recent troughs as inflation itself has backed off — from recent peaks of around 9% to 6%. As we see in the chart, at roughly 64 in the most up-to-date data, and around 100 in 2019, sentiment is down by about a third over that timeframe.

No surprise that inflation remains top of mind: PYMNTS found, when we asked at the end of November 2022, when inflation might return to pre-2021 levels, surveyed consumers on average predicted around July 2024. By February, that average date had moved out to October 2024.

Even if the Conference Board data sees inflation running at about 6% for the next several months, that’s still well above the 2% rate that’s favored by the Fed, and above the rate where sentiment really peaks. And it’s sentiment, after all, that’s going to drive merchant sales, and boost the fortunes of Main Street businesses.

These firms, of course, are seemingly girding for rough seas: 40% of small and midsized businesses (SMBs) remain more worried about inflation than one year ago, and 15% report being concerned about declining revenues. Roughly 50% of SMBs see that they will tap credit more heavily in the year ahead, which would serve as a way to help navigate inflationary pressures, while still maintaining operations.