For traditional financial services providers — chiefly credit unions — the future belongs to youth.

For FinTechs, in looking at Gen Z consumers, well, things are a bit more cautious. They feel, to put it bluntly, that the juice is not worth the squeeze.

PYMNTS Intelligence, in delving into the mindset of more that 200 credit union (CU) executives and more than 100 FinTech executives, found a bit of bifurcation in how these providers think about consumers who were born between the years 1981 to 1996 and who are now in their late 20s to early 40s.

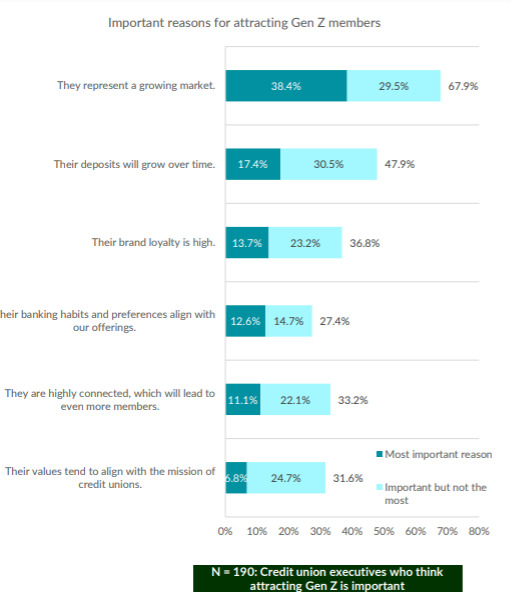

In terms of headline numbers, 95% of CUs find attracting more Gen Z members highly important, primarily because they represent a growing market, as the accompanying chart shows.

Conversely, only 42% of FinTechs feel that attracting this demographic is “very” important. Of the respondents who placed a lower “level” of importance on attracting those younger customers, nearly 53% said that these individuals did not have enough money to offer up in terms of deposits. And about 45% said, overall, that they’d be quick to leave even if they joined.

There’s some room to grow here, for the FinTechs. PYMNTS Intelligence has found that about 41% of Gen Z consumers have used PayPal as their most-used digital choice, trailed by Chime, at about 7% and Ally at about 3%.

The deposit question is an interesting one, we note. Only 18% of the 5% of credit unions that are less interested in luring Gen Z denizens say that they do not have enough deposits … which indicates a key difference between the CUs and the FinTechs that might seek to offer banking services. Sixteen percent of the FinTechs we spoke to say they are competitors, and sometimes even client/competitors, to CUs, so there is some consideration of market share and share of wallet.

The credit unions, after all, have tens of millions, hundreds of millions, even a few billion dollars worth of deposits already on hand (depending on the size of the CU) and thus have enough activity going on to help fund operations and take on even the smallest depositors. They can play the long game, so to speak, and look to have the (smallest) deposits grow over time (a factor cited by nearly half of CUs interested in attracting more Gen Z clients).

As to what Gen Z consumers want from their providers, PYMNTS Intelligence found last year that more than a third of these clients would switch from their financial institution in search of new innovations — including a broader range of payment options. Elsewhere, our data show that 59% of Gen Z customers say they are more interested in personalized rewards programs and 49% of Gen Z cardholders prefer receiving offers through mobile apps.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More