Credit unions (CUs) provide financial services to a community of members often connected by location, work or education. Although many CUs might not have the national or regional scope of traditional banks, their members expect that they provide digital-first capabilities that can compete with what for-profit financial institutions (FIs) offer. Research shows that CUs are rising to the challenge, yet some are doing it better than others. This first-of-its-kind index measures member satisfaction with CUs’ current and future offerings to provide insights into what CUs do well and where they need to improve.

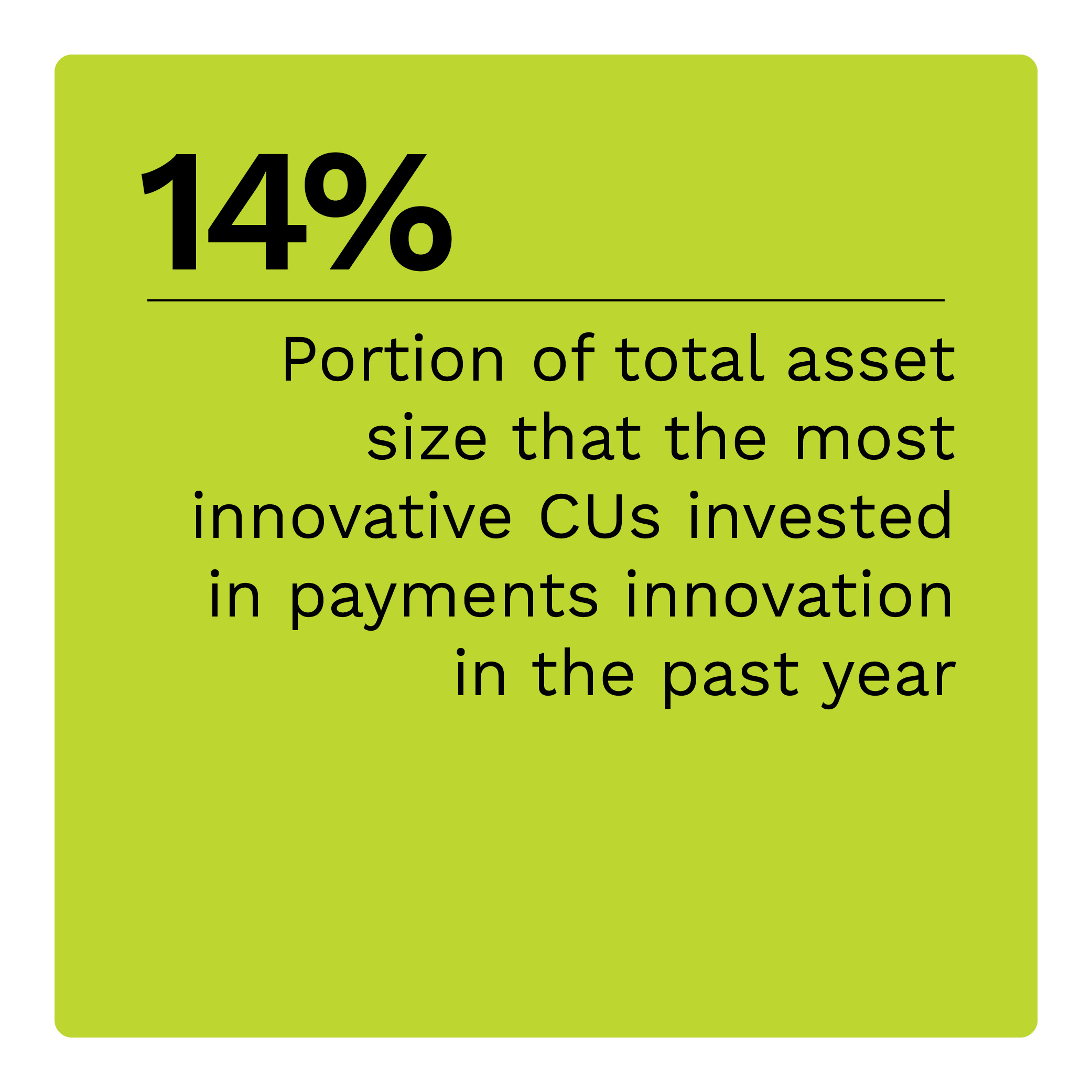

The most innovative CUs, which we have separated into a group of the top 30 performers, match their members preferences roughly 68% of the time. The bottom 30 performers match approximately 40% of what CU members want. Top performers also invest 13% more in payments innovation than bottom performers and benefit from 57% lower member churn as a result. They are also better positioned to grow their membership.

These are just some of the findings from the “2024 Credit Union Innovation Readiness Index” (CU-IRI), a PYMNTS Intelligence and PSCU collaboration. The report examines how CUs can reap the benefits of digital innovation to gain members and reduce churn. The index is based on two surveys. First, a survey of 201 CU executives was conducted from Oct. 4, 2023, to Nov. 16, 2023, to learn about CUs’ current product and feature offerings as well as their plans for future innovation. Second, a census-balanced survey of 4,525 U.S. consumers was conducted between Nov. 2, 2023, and Dec. 6, 2023, to investigate what products and features consumers want and expect from CUs.

Other key findings from the report include:

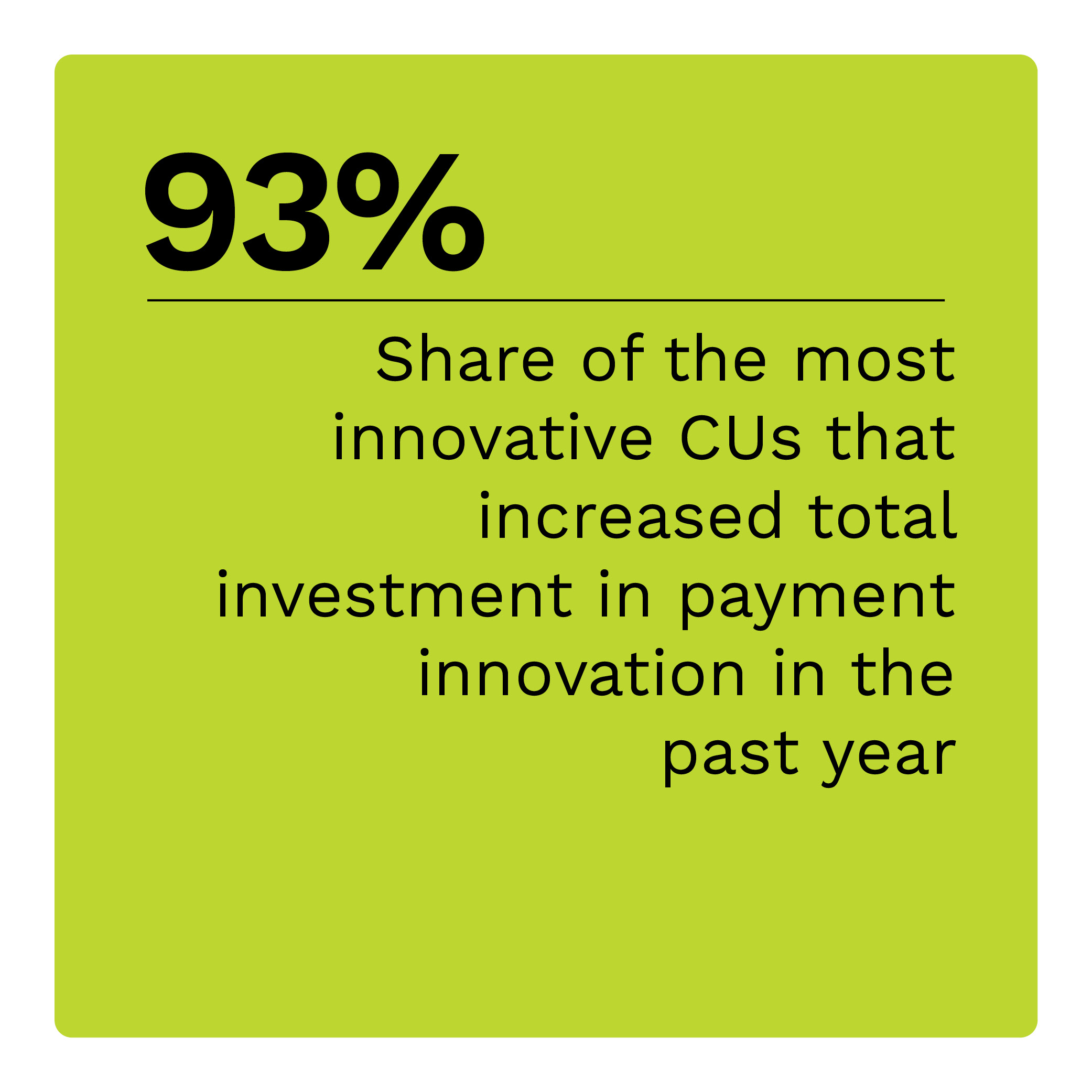

We found that 93% of top IRI performers increased their total investment in payment innovation in the past year, compared to 58% of bottom performers. Top-performing CUs made more successful investments in innovation than others: 90% saw a positive ROI from their payment innovation investments, compared to 63% of bottom performers. The most innovative CUs have also performed better across other metrics this year.

Nearly three-quarters of top-performing CUs say providing a highly personalized user experience is essential to attracting more members in the next three years. Just over half of bottom performers say the same. Instead, less innovative CUs are more likely to prioritize a simple and intuitive user experience. This suggests that prioritizing products with broad but generic appeal may not set CUs up for success.

Nearly three-quarters of top-performing CUs say providing a highly personalized user experience is essential to attracting more members in the next three years. Just over half of bottom performers say the same. Instead, less innovative CUs are more likely to prioritize a simple and intuitive user experience. This suggests that prioritizing products with broad but generic appeal may not set CUs up for success.

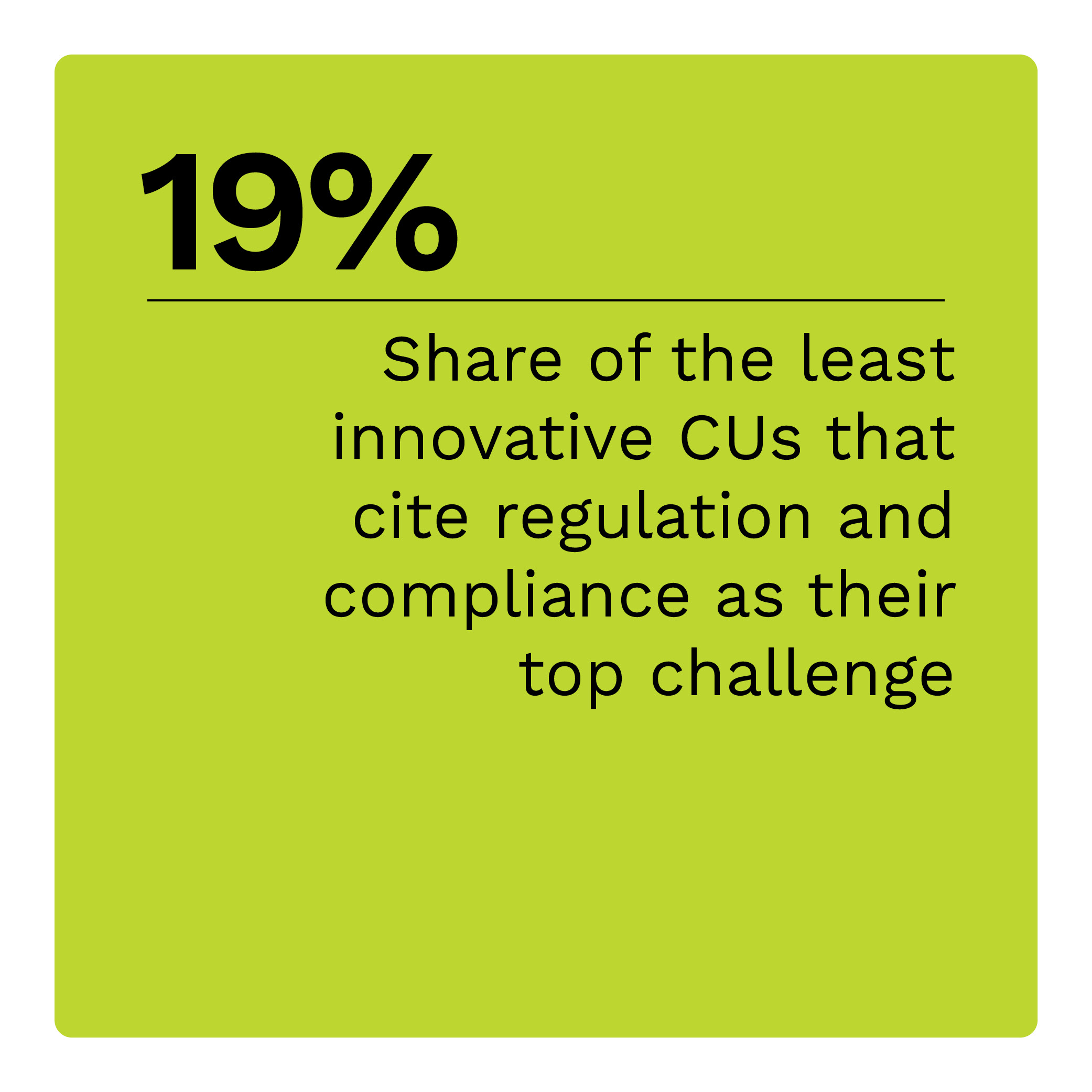

Bottom-performing CUs are more likely than middle- and top-performing CUs to cite regulatory and compliance issues and lack of budget as their most significant challenges in bringing payment innovations to market. Although budget concerns are the second-most cited challenge, they may be the most concerning: 16% of bottom-performing CUs cited a lack of budget, compared to just 3.3% of top-performing CUs.

With greater investments in innovation, top index performers are clearly committed to providing members with the products they want. Download the report to learn how CUs are leveraging innovation to provide the digital-first banking experiences consumers want.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More