In the current economic environment, Generation Z consumers struggle more than older consumers. Nonetheless, they are a growing demographic that financial service providers — including credit unions (CUs) — need to watch.

This generation is made up primarily of digital-first consumers who manage and spend their money via digital channels. Financial institutions (FIs) can increase engagement among Gen Z consumers by offering innovative products and services.

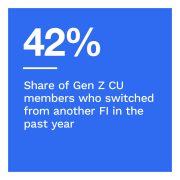

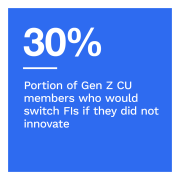

Data shows, however, that Gen Z consumers can be fickle. For example, 4 in 10 Gen Z CU members say they switched FIs in the past year. In contrast, only 4 in 100 baby boomers and seniors switched. Lack of innovation drives Gen Z away. In fact, Gen Z are 2.5 times more likely than baby boomers and seniors to say they would leave FIs that don’t innovate.

There is a disconnect between CUs’ innovation roadmaps and what Gen Z members want. CUs must align their innovation agendas with Gen Z’s needs and expectations.

These are just of the findings from “How Credit Union Innovation Can Drive Gen Z Engagement,” a PYMNTS Intelligence and Velera (formerly PSCU/Co-op Solutions) collaboration. The report examines how innovation on products and services can help CUs retain their current Gen Z members while attracting new ones. The report is based on two surveys. First, a survey of 201 CU executives conducted from Oct. 4, 2023, to Nov. 16, 2023, to learn about CUs’ current product and feature offerings as well as their plans for future innovation. Second, a census-balanced survey of 4,525 U.S. consumers that investigated which products and features consumers want and expect from CUs conducted between Nov. 2, 2023, and Dec. 6, 2023.

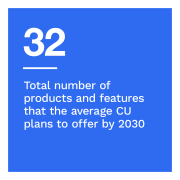

Gen Z consumers have high expectations, and CUs need to have the right innovation roadmap. The average Gen Z consumer has used 10 products and features in the past year and would use another 18 if offered, reaching a total of 28 products and features. Data shows that top-performing CUs are better positioned to meet Gen Z’s demands. In fact, top performers currently offer 40% more products and capabilities than bottom performers.

Gen Z shows a relatively strong interest in financial service offerings that help them pay friends and manage their spending. In fact, these younger members want their CUs to innovate P2P transactions and tailored debit cards more than other members. These young consumers value financial products and services that match lifestyles centered on social activities and discretionary spending.

Many CUs are not planning to offer the products and features Gen Z wants. For example, 41% of CUs have no plans to offer Zelle by 2030. In addition, 85% have no plans to offer young adult and teen debit cards by 2030.

CUs that best meet Gen Z’s needs can reduce member churn and attract new members in the future. Download the report to learn more about how CU innovation is necessary to engage Gen Z consumers.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More