New and existing customers are coming to interact with their financial institutions (FIs) using digital channels first.

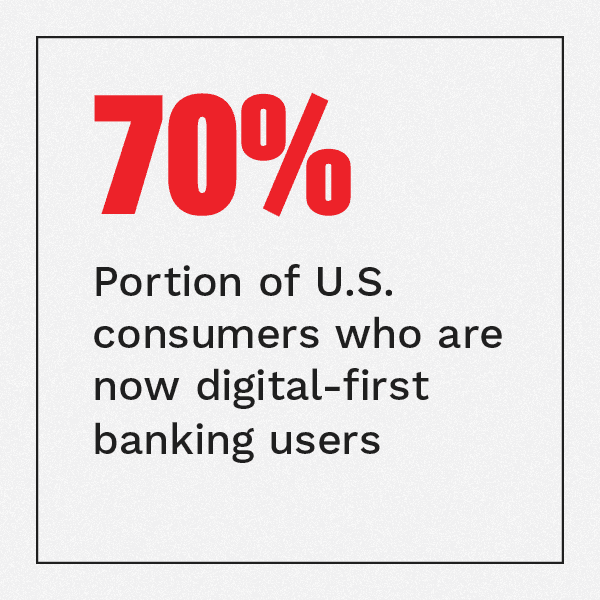

PYMNTS data found that 70 percent of United States consumers now count as digital-first customers, for example. That the pandemic has accelerated this ongoing trend should be unsurprising to the banking industry, but what is more notable is how the ongoing global health crisis has impacted users’ views on data privacy and digital identity.

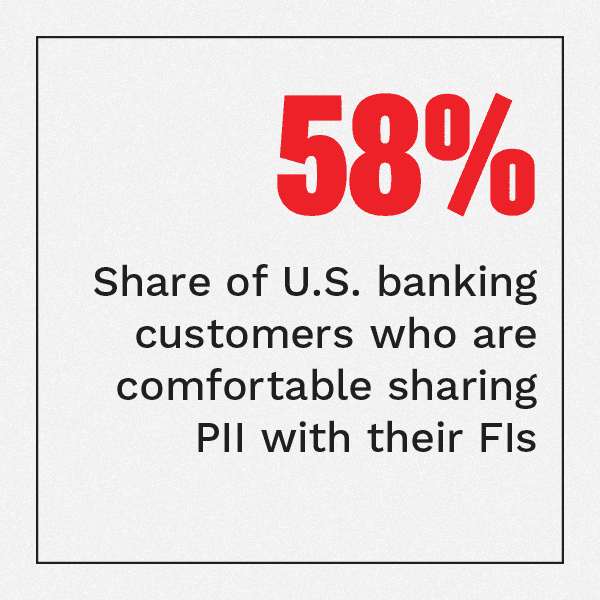

Consumers’ comfort levels with digital data sharing have exp anded alongside their trust in digital banking, with PYMNTS data showing 58 percent of consumers are perfectly fine sharing their personally identifiable information (PII) with banks when onboarding. The authentication measures and security solutions consumers trust are slowly shifting, however, and the impact of the ongoing pandemic has only accelerated this change. More consumers are now comfortable with biometric authentication measures, for example, and they are expecting banks to match their new digital identification needs and preferences accordingly.

anded alongside their trust in digital banking, with PYMNTS data showing 58 percent of consumers are perfectly fine sharing their personally identifiable information (PII) with banks when onboarding. The authentication measures and security solutions consumers trust are slowly shifting, however, and the impact of the ongoing pandemic has only accelerated this change. More consumers are now comfortable with biometric authentication measures, for example, and they are expecting banks to match their new digital identification needs and preferences accordingly.

In the inaugural Digital Onboarding Tracker®: Building Banks’ Digital Front Door, a collaboration with Acuant, PYMNTS analyzes how the pandemic has changed users’ digital identity wants and needs, as well as how banks can keep up with these shifts. It also examines the role of emerging technologies, such as biometrics, in these spaces and how FIs can tap them to better engage and satisfy their customers.

Around The Digital Onboarding World

More consumers are heading online first when it comes time to find new banks or open new accounts, a trend that is only expected to accelerate over the next several years. One study predicted 330 million new accounts will be opened via online banking channels in 2025, a sharp uptick compared to the 184 million such accounts that were opened this way by the end of 2020. Determining how to keep this experience seamless and secure for customers is a must for FIs to stay competitive, with the study also predicting banks will increase their use of automated technologies to do so. Tapping artificial intelligence (AI) and related tools could help to make the onboarding process more efficient, potentially saving FIs a collective $460 million in onboarding costs, for example.

Mobile banking usage has also increased since the start of the pandemic, becoming the preferred channel for more consumers when it comes time to interact with their FIs. Fifty-five percent of consumers now claim this is the case, compared to the 47 percent who noted the same prior to the start of the global health crisis. This makes it essential for FIs to be able to integrate robust security measures on these channels that can protect users’ data, especially as concerns over cybersecurity grow. Eighty percent of bank executives noted data privacy and digital security were presently two of their top worries, for example, while other research found consumers’ own perceptions regarding the safety of their digital data is also shifting.

their digital data is also shifting.

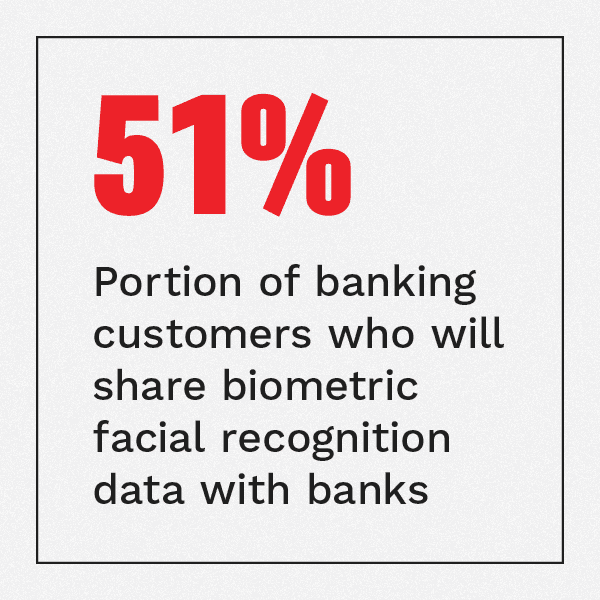

Username and passwords are no longer among the top three identification methods preferred by consumers, according to one study — rather, consumers now prefer to authenticate themselves using biometric traits, such as fingerprints or voiceprints, through text messages or by using behavioral biometric solutions. Younger consumers are also slightly more trusting of biometrics, with 48 percent of those below 40 years old stating they feel comfortable providing biometric data to their banks in order to verify their identities. This is compared to 37 percent of those customers over that age.

For more on these and other stories, visit the Tracker’s News & Trends.

Why Flexible Identity Verification, Onboarding Solutions Are Key To Capturing Consumer Trust

The ongoing pandemic has accelerated consumers’ preference to interact with their existing banks or to find new FIs digitally, and it has also highlighted the importance of online privacy. Consumers’ perceptions of what constitutes a safe and secure onboarding or login experience is changing as they grow more familiar with digital banking, making it imperative for FIs to be able to offer robust digital identification measures to new and returning users to convey this sense of security.

Placing control of the digital identification process in the hands of consumers can help to enhance this sense of trust, explained Rami Thabet, vice president of Digital Product at Royal Bank of Canada (RBC), in a PYMNTS interview.

To learn more about how identity verification needs are evolving and why FIs must restructure their onboarding processes accordingly, visit the Tracker’s Feature Story.

Deep Dive: How FIs Can Tap Biometrics To Meet Digital-First Consumers’ Shifting Online Identification Needs

FIs looking to better engage with the growing number of new customers seeking dig ital or mobile banking experiences must ensure they foster trust from the very beginning of the onboarding experience. This means assuring customers of the safety and security of their personal information, as online account fraud and identity theft volumes rise. Research found 56 million Americans were the victims of new account fraud in the 12 months preceding the study, for example. Protecting against such fraud, where bad actors use previously stolen data to open accounts in the name of legitimate customers, is therefore critically important for banks.

ital or mobile banking experiences must ensure they foster trust from the very beginning of the onboarding experience. This means assuring customers of the safety and security of their personal information, as online account fraud and identity theft volumes rise. Research found 56 million Americans were the victims of new account fraud in the 12 months preceding the study, for example. Protecting against such fraud, where bad actors use previously stolen data to open accounts in the name of legitimate customers, is therefore critically important for banks.

To learn more about how banks can use emerging technologies, such as biometrics, to meet changing digital identity needs, visit the Tracker’s Deep Dive.

About The Tracker

The Digital Onboarding Tracker®, a PYMNTS and Acuant collaboration, analyzes the latest digital onboarding and identification trends and developments. It also examines how emerging technologies, such as AI and biometrics, are coming to play a key role in data privacy and cybersecurity as the need for more tailored identification solutions grows.