The cash cushions are dwindling. The credit card balances are a monthly obligation, of course.

The paycheck-to-paycheck consumer continues to strive to make ends meet. But the high-wire balancing act of managing obligations and the money that comes in (from the paychecks) becomes ever tougher.

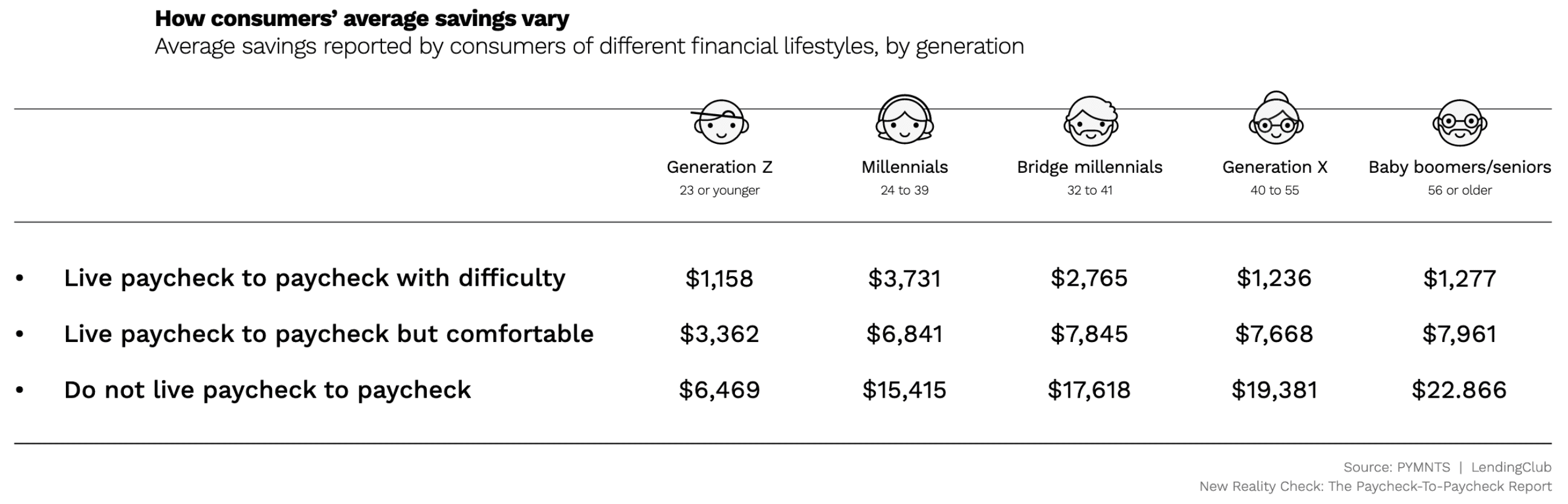

And the pinch might be most acutely felt by the older demographics, with comparatively smaller cash cushions in place.

Triangulating some of the insights gleaned from the recent spate of reports on the state of the paycheck-to-paycheck economy show that the higher costs of living are hitting home, literally.

As noted in recent studies, Generation Z consumers who live paycheck to paycheck and have issues paying their monthly bills report the lowest average savings at just $1,158, according to the report. Millennials living paycheck to paycheck with issues paying their monthly bills report the highest savings, with an average of $3,731.

Savings amounts decrease and then level off as consumers grow older. Go “up the ladder” in terms of age demographics, and baby boomers and seniors who are still living paycheck to paycheck have only roughly $1,250 in savings — and a growing percentage of this cohort is living paycheck to paycheck, at 54% versus 40% last year. The consumers who don’t live paycheck to paycheck (which is, again a minority), have higher savings balances (Boomers have $7,900 in the bank and seniors have nearly $23,000.).

Read also: Millennial Minute: 70% of Millennials Live Paycheck to Paycheck

By way of contrast, the younger generations — the Bridge Millennials and the Millennials, have seen their “shares” of paycheck-to-paycheck living remain relatively unchanged, as measured year over year. More Gen Z consumers report living P2P than last year, at 65.4% vs. 55.4%. Roughly two-thirds of this cohort who say they struggle to pay their bills say they cannot afford a $400 emergency and have savings of about $1,100.

Separately, we found that the paycheck-to-paycheck consumers, overall, are three times more likely to have credit card debt and carry higher balances than those who don’t live P2P. We found that of those consumers living P2P, with difficulty, the average “carry” on their credit card balances was $3,863, with limit on their primary card of $4,702 — indicating that there is not all that much wiggle room.

Separately, we found that the paycheck-to-paycheck consumers, overall, are three times more likely to have credit card debt and carry higher balances than those who don’t live P2P. We found that of those consumers living P2P, with difficulty, the average “carry” on their credit card balances was $3,863, with limit on their primary card of $4,702 — indicating that there is not all that much wiggle room.

Read also: New Reality Check: The Paycheck-To-Paycheck Report: The Credit Edition

Triangulating all this indicates that, given the cash cushions, the debt in place, the ceiling on that credit card debt — and increasingly rising costs of everyday expenses … well, something’s got to give way. We may see a financial fine-tuning where consumers continue to cut down on all but the nonessential expenses.

Read also: 61% of Consumers Shopped Mostly for Essentials in March

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More