The holidays are upon us. The credit card debt has been racked up. The broad deluge of earnings reports has slowed to a trickle.

The data and commentary show that U.S. consumers are feeling stretched and pinched into the last few weeks of the year — and beyond.

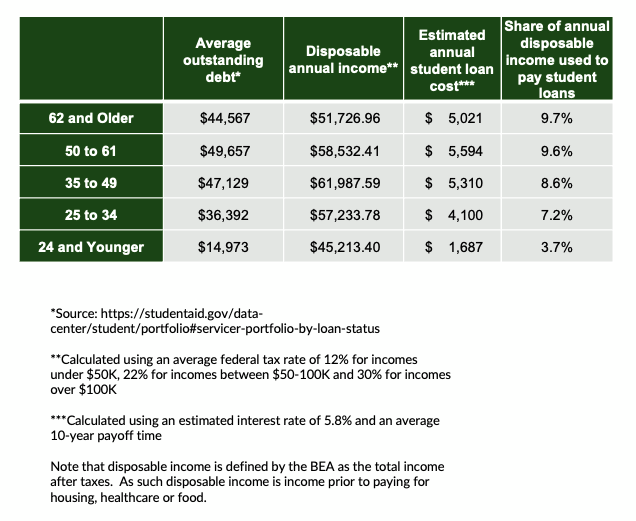

Student Loans Are Having an Impact

In recent months, PYMNTS Intelligence found that nearly half of consumers said the resumption of student loan payments would hurt their ability to save. And 35% said they worried about affording everyday expenses.

There’s evidence that the impact is real, and the impact is now. Depending on the generation, and the student debt load, the “bite” out of disposable income ranges from the mid-single-digit percentage points to the low-double-digit percentage points.

Commentaries from the likes of Walmart and Target have discussed, qualitatively, that student loan payments have been pressuring consumers, or at least rendering them more cautious in the aisles. It’s an added pressure in the paycheck-to-paycheck lifestyle that has affected about 60% of consumers.

Commentaries from the likes of Walmart and Target have discussed, qualitatively, that student loan payments have been pressuring consumers, or at least rendering them more cautious in the aisles. It’s an added pressure in the paycheck-to-paycheck lifestyle that has affected about 60% of consumers.

During Walmart’s earnings call with analysts, management noted the softening of consumer spending in October (which led to cautious guidance for the rest of the year), and Chief Financial Officer John David Rainey said, “You’ve got the repayment of student loans, which affects about 27 million Americans. All of these things could be contributing” to the slowdown.

Separately, Target CEO Brian Cornell said on his firm’s earnings call (where comp sales slipped year on year) that “overall, consumers are still spending, but pressures like higher interest rates, the resumption of student loan repayments, increased credit card debt, and reduced savings rates have left them with less discretionary income, forcing them to make trade-offs in their family budgets.”

October Marked a Spending Reversal

Walmart’s experience in October dovetails with government data, which showed this week that retail and food service sales declined for the first time in seven months. Spending at department stores was 1.2% lower and eCommerce sales were flat, as measured month over month.

Revolving Card Balances Are Stubbornly Entrenched

Credit has been a key means of making it possible to keep on spending where we are spending. But there are signs that this payment method is becoming a bit, well, strained. PYMNTS Intelligence in the report “Credit Card Use During Economic Turbulence” found that 15% of consumers have reduced their credit card spending, which means everyone else has kept that spending at the same pace or increased the pace. But roughly half of consumers who said they have been adversely impacted by inflation carry revolving balances.

BNPL Is on More Consumers’ Radar Screens

Given the pressures of inflation, student loan repayments and credit card obligations, it comes as no surprise that buy now, pay later (BNPL) is becoming a key choice in the bid to make expenses — even everyday expenses — more affordable. PYMNTS Intelligence found that 16% of consumers — or 40.5 million people — in the U.S. used BNPL over the past several months. The data showed that 16% of BNPL users made purchases via the option at least weekly, and another 25% did so monthly. This means that nearly 4 out of 10 U.S. consumers used BNPL products at least once a month. Preserving cash and lines of credit is the primary reason for most BNPL users to choose this payment method, and it has gained wide embrace as a budgeting tool.

Sentiment Is Waning

Sentiment determines intent — to spend, that is. The University of Michigan earlier this month found that consumers expect inflation a year from now to stand at 4.4%, up from last month’s 4.2%. Looking out over five years, consumers expect a 3.2% inflationary increase — the highest five-year level seen since 2011. Earlier this year, PYMNTS surveyed a broad swath of consumers who said that inflation will be firmly in place until October 2024, so it will be about a year before we reach pre-pandemic levels. As many as 85% of consumers do not see or feel that their incomes are keeping pace with inflation.

For consumers, and for the merchants relying on them, it could be a long, cold winter — with a chilling effect all around.