In 2022 alone, consumers reported losses of nearly $9 billion to fraud, with bank fraud cases rising by 25% compared to the previous year. This growing wave of criminal activity poses a serious threat to the financial services sector, as customers rely on their platforms for secure transactions.

To address these security challenges, FIs are embracing a range of technology solutions. These include artificial intelligence/machine learning (AI/ML) systems, fraud prevention application programming interfaces (APIs), data encryption, customer transaction alerts, biometric and web-based multi-factor authentication.

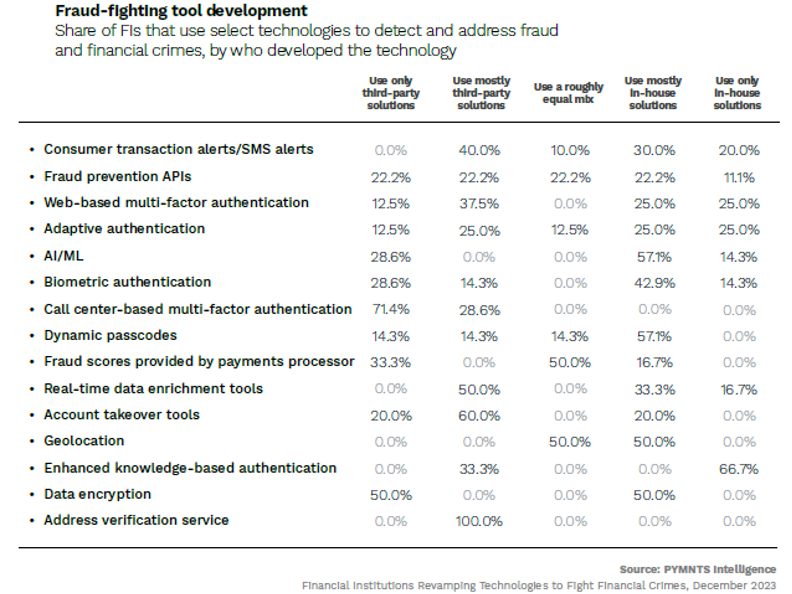

However, each of these solutions present unique sets of challenges in terms of innovation and integration. Consequently, third-party providers play a crucial role in this landscape. Despite this reliance on external assistance, FIs still maintain a significant level of in-house development, developing 48% of the technologies and 57% of the processes utilized to combat fraud.

For instance, 70% of FIs utilize both AI and ML in their efforts to counter fraud, with nearly 60% using mostly in-house solutions. Additionally, just 14% of FIs use only AI/ML tools they’ve developed in-house, while nearly 30% rely exclusively on third-party solutions to provide these.

Per the study, “in-house development of AI and ML tools requires substantial costs, which can help explain why this share is low.”

The study also found that 50% of FIs mostly rely on data encryption tools to fight fraud, with an equal share exclusively utilizing third-party data encryption solutions.

It is also worth noting that an equal share of FIs (22%) reported utilizing fraud-prevention APIs across all categories: those exclusively relying on third-party solutions, those predominantly reliant on third-party solutions, those employing a balanced mix of both, and those primarily relying on in-house solutions. Overall, the survey revealed that 90% of FIs use fraud prevention APIs to detect and address fraud.

Adaptive authentication and web-based multi-factor authentication are also widely adopted fraud-fighting tools, with 80% of FIs incorporating each tool into their anti-fraud strategies.

When it comes to selecting third-party solutions, FIs prioritize the reputation of the provider, which is considered a top factor in decision-making for nearly all FIs surveyed. This factor, coupled with ease of integration, outweighs other considerations such as evidence from other FIs, customer needs, and employee feedback.

Looking ahead, FIs have plans to revamp their efforts over the next three years. Specifically, 80% of FIs intend to continue relying on a mix of third-party providers and their own technology, while 20% will integrate third-party technologies into their existing systems instead of developing their own. The findings suggest that this decision may be driven by cost considerations.