Financial stumbles may have long-lasting impacts on consumers whose credit scores have been affected by these trip-ups. This is evidenced in the report “The Credit Accessibility Series: The Credit Insecure Need More Education,” a PYMNTS and Sezzle collaboration, which explored the dollars and cents cost of being a subprime borrower.

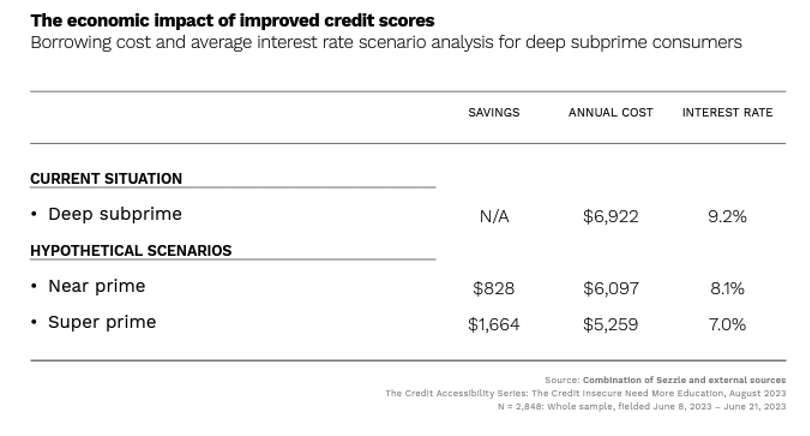

The average interest rate for deep subprime consumers, whose credit scores ranged between 580 and 619, was 9.2%. These consumers paid an average of $6,922 in interest, which the report found represented 13% of their income. In the race to stay afloat when it comes to day-to-day expenses, it may be little wonder then that subprime borrowers are increasingly reliant on credit cards and other lending products, even as delinquencies rise.

The average interest rate for deep subprime consumers, whose credit scores ranged between 580 and 619, was 9.2%. These consumers paid an average of $6,922 in interest, which the report found represented 13% of their income. In the race to stay afloat when it comes to day-to-day expenses, it may be little wonder then that subprime borrowers are increasingly reliant on credit cards and other lending products, even as delinquencies rise.

These increased costs have led some consumers to make difficult decisions. In an interview with PYMNTS, Genesis Credit Chief Commercial Officer Ed Haluska described the choice consumers now face and why their current financial situation may be different than past downturns experienced.

Haluska noted that consumers have “come out of this period of time where money was falling from the sky. There was a huge amount of access to credit and a huge amount of liquidity” from government stimulus programs.

Now the government programs have dried up and people are faced with tough decisions, he said.

“The choice among the lower socioeconomic groups is, ‘Do I pay for milk and bread, do I put gas in the car … or am I going to get elective medical?’”

Some FinTechs are making inroads to assist consumers with subprime credit scores to get on more even financial footing. In May, i2c and Access Finance announced a partnership to bring the latter’s Juzt Mastercard program from Europe using i2c’s payments platform. Aimed at credit-challenged consumers with little or no credit history, the international consumer credit card on the Mastercard network offers higher approval rates, as well as access to Apple Pay and Google Pay to its customers.

Other players, too, such as Bond, offer consumers with subprime credit secured cards to forge a path toward building or rebuilding their credit.