Banks, consumers and merchants have all raced to adjust their operations over the past year, changing their once-routine approaches to payments as open banking developments sweep across the globe. Financial institutions (FIs) and FinTechs are collaborating with increasing frequency to enhance open banking’s availability and reach, especially in the United States, where creating seamless and safe payment experiences is becoming more and more critical for merchants looking to keep customers engaged.

Consumers are coming to expect security and speed regardless of where they shop, with recent PYMNTS data finding that 86 percent of Americans with annual incomes above $100,000 believe businesses should protect their data at all costs. Enabling this convenience and security requires merchants to adopt open banking solutions that can allow for easy payment on the customer side and swifter data sharing on the merchant end, allowing businesses to create more tailored marketing and product offerings  and to take control of the customer relationship.

and to take control of the customer relationship.

In the latest U.S. Open Banking Tracker®, PYMNTS analyzes why merchants must stay on top of emerging payment trends, including real-time and open banking developments, to meet consumers’ needs and take control of the customer relationship. It also examines the growing importance of contactless and account-to-account (A2A) payments within this space and how merchants can take advantage of these tools.

Around The U.S. Open Banking Space

Contactless payments’ use has accelerated over the past year as customers move away from cash and cards and toward digital methods. One recent study found 91 percent of U.S. consumers are now using touchless payment methods such as mobile wallets or contactless cards when shopping, for example. This makes it imperative for merchants to embrace open banking solutions that can offer the convenience and flexibility consumers crave to stay in control of the customer relationship.

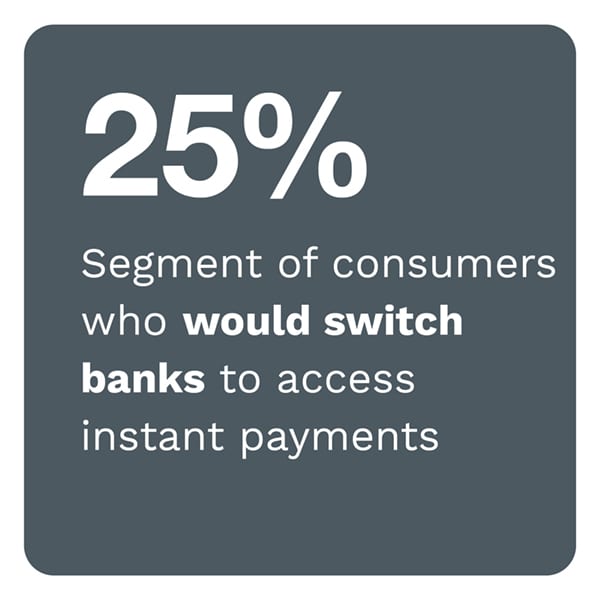

Getting shoppers to adopt open banking-supported payments first requires getting them to trust said payments, but one recent study found that 52 percent of consumers globally still remain unaware of what open banking means. It also found that 61 percent are sure they have not used open banking to make payments — making education the first step to developing the trust necessary to drive open banking-supported payments forward. Merchants and banks must move swiftly to ensure consumers understand how open banking solutions work and what benefits they offer, including how they can support speedy and convenient payment methods such as mobile wallets.

Banks are also working closely with FinTechs to b olster open banking initiatives and support financial innovation as the need for them expands. FinTech and application programming interface (API) provider Plaid recently announced a partnership with U.S. Bank that will allow the latter’s customers to seamlessly connect with third-party FinTech apps, for example. The two also aim to connect Plaid’s beta Portal solution with U.S. Bank’s MyControls app to enable more connectivity and ease of use for customers. These and other such collaborations between banks and FinTechs in the U.S. are expected affect Americans’ payment preferences and needs in the years ahead.

olster open banking initiatives and support financial innovation as the need for them expands. FinTech and application programming interface (API) provider Plaid recently announced a partnership with U.S. Bank that will allow the latter’s customers to seamlessly connect with third-party FinTech apps, for example. The two also aim to connect Plaid’s beta Portal solution with U.S. Bank’s MyControls app to enable more connectivity and ease of use for customers. These and other such collaborations between banks and FinTechs in the U.S. are expected affect Americans’ payment preferences and needs in the years ahead.

For more on these and other stories, visit the Tracker’s News & Trends.

TD Bank On Why Supporting Data-Driven Payments Is Key To Engaging Consumers

Consumers are searching for flexible payment experiences wherever they shop, putting pressure on their favored merchants to keep pace. Retailers must enable diverse payment methods across all channels to keep their customers engaged and transacting, and integrating A2A payments and digital wallets could help them do so, Barry Baird, head of payments capability and delivery at TD Bank, said in a recent PYMNTS interview. To learn more about how integrating digital payments underpinned by open banking can help merchants take control of the customer relationship, visit the Tracker’s Feature Story.

Deep Dive: How Adopting Real-Time Payments Can Help Merchants Retain Mobile-First Customers

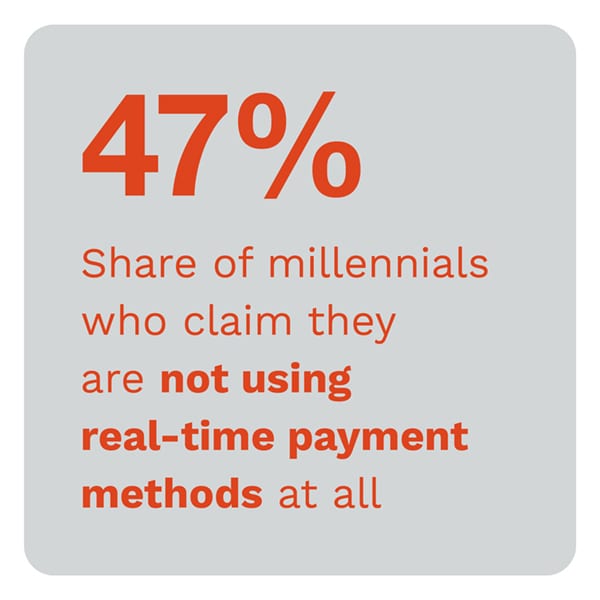

More consumers now reach for their smartphones at the point of sale (POS), gravitating toward contactless or peer-to-peer (P2P) digital payment methods instead of cash or cards. This growing interest in emerging payments, in turn, represents a key opportunity for U.S. merchants to incorporate real-time or open banking-supported payment methods. To find out more about how integrating real-time payments could help merchants gain a competitive edge when it comes to engaging and retaining today’s digital-first customers, visit the Tracker’s Deep Dive.

About The Tracker

The U.S. Open Banking Tracker®, a PYMNTS and Endava collaboration, examines how open banking developments are affecting U.S. retail payment trends and future developments.