Amid the turmoil rocking the financial services sector, as the flights to safety continue, individual and enterprise customers are weighing what’s important to them.

And depending on where you look — and the audience you examine — there are different priorities when choosing a traditional financial institution (FI) or a non-bank financial services provider.

That last group, the non-bank, well, it’s pretty broad. The designation covers FinTechs, digital-only banks (or neobanks, as the terms tend to be used interchangeably), Big Tech firms and even some retail juggernauts such as Walmart.

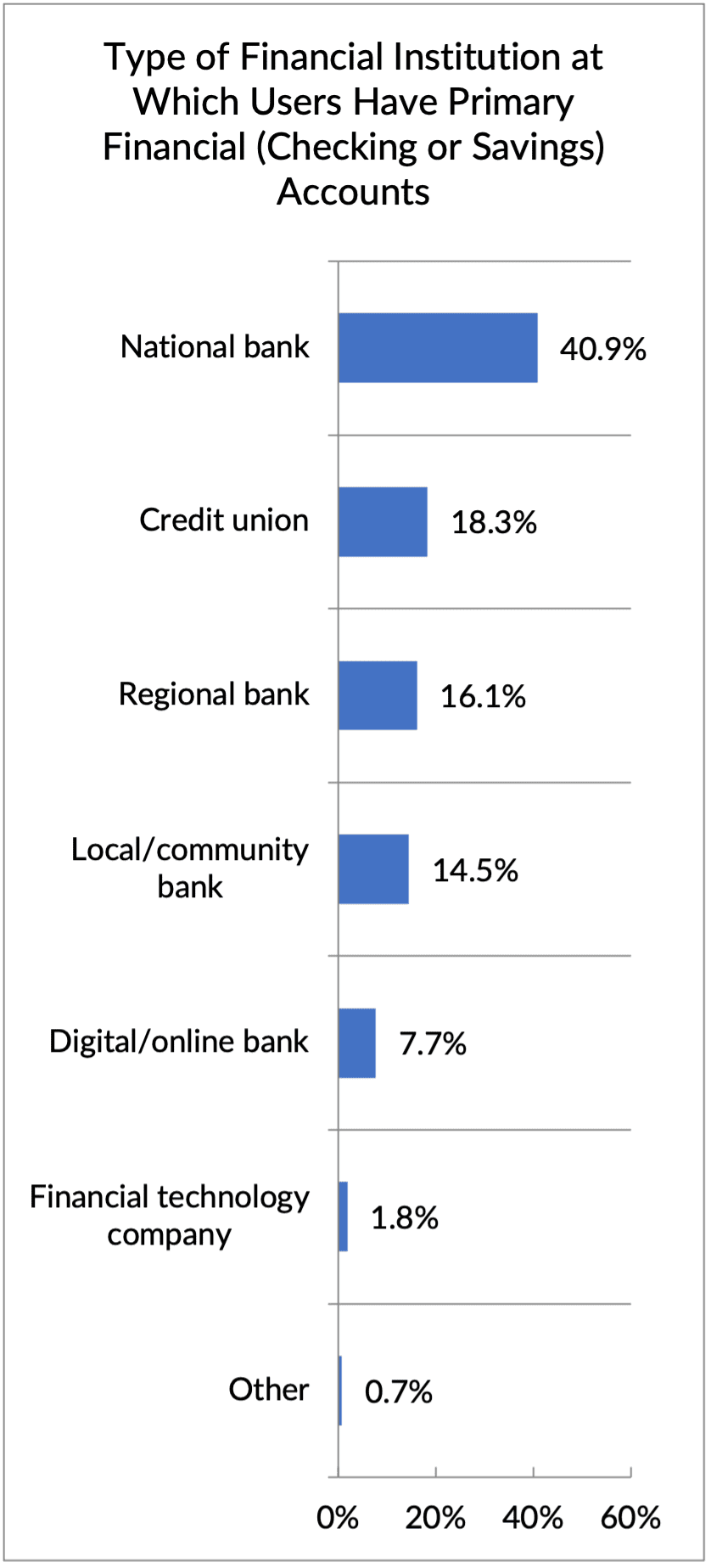

In joint effort with Ingo Money, PYMNTS has found in recent research that traditional FIs — the mainstays of financial institutions — still are the predominant providers. National banks house the primary checking and savings accounts of close to 41% of the nearly 2,000 consumers surveyed. Credit unions have garnered the loyalty of another 18% and regional banks a further 16%. Digital banks have a much smaller share, at less than 8%.

Drill down a bit, and national banks have a significant presence across all generations: More than a third of baby boomers and seniors, Gen X consumers and millennials, right down to Generation Z members have their primary relationships with the national players. Digital banks, at their “peak” market share, have about 13% of bridge millennial and millennial users.

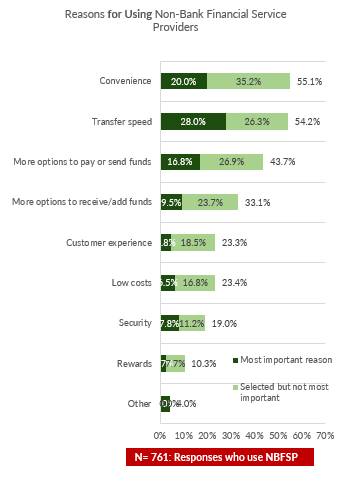

For the consumers who are using the non-bank financial service providers, PYMNTS and Ingo found that convenience tops the list, cited as an important factor by more than 55% of individuals queried. Speed followed closely behind, at 54%.

Security? That came in as a reason for consideration by 19% of users.

But for those consumers opting not to use a non-banking provider — i.e., they’ve chosen, instead, to bank with, well, banks — security was the reason they’ve not embraced the digital-only operators or nascent financial services entrants. Security was top of mind for nearly 39% of the traditional banking adherents.

We note that in the current environment, concerns over data security, and the security of customers’ funds in general, may be among the key features that wind up determining where consumers park their money. Speed is nice, convenience, too. But as we saw in the bank runs that have bedeviled the sector in the few short weeks since Silicon Valley Bank collapsed, there may be something to be said for having physical branches, a human presence, and some reassurance in the mix during hectic times. Some of the digital-only upstarts sprung up from the ashes of the 2008 financial crisis, and now may be tested in ways that had not been anticipated.

That’s especially true of the business banking clients — the ones that have accounts that tend to be above the $250,000 threshold for insured deposits that has been a hot-button issue as of late.

Banks, in the meantime, have been investing and broadening their digital capabilities, as PYMNTS has reported. The innovations and personalization efforts can go a long way toward building on the trust that’s already been established.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More