Hsu on Thursday issued a statement after the FDIC’s board of directors voted to enhance its merger guidance for the first time in 16 years. The OCC introduced similar changes in January.

“Healthy bank mergers — i.e., those that benefit communities, support bank resilience and financial stability, and enhance competition – should be approved,” Hsu said in the statement. “Merger applications that would diminish competition, hurt communities, or present systemic risks should be withdrawn or rejected.”

Coming almost a year after three U.S banks collapsed, it’s understandable Hsu is concerned about mergers triggering “systemic risk,” but absent from his list of concerns is an acknowledgement that most banks continue to rely on outdated legacy technology — a reliance can also put them at risk.

And when bank mergers integrate legacy systems, it can open the door to bank fraud.

“Banking legacy systems are plagued with vulnerabilities that hackers can easily exploit,” said Ron Huber, CEO of Achieve Internet, an API solution provider, in an article. “Banking legacy systems are … an easily exploitable weakness in the financial sector. Banks need to upgrade their legacy systems with modern security controls to stay competitive, protect customer data, and ensure overall bank security.”

But, as PYMNTS Intelligence research has found, fraud concerns are forestalling financial institutions (FIs) from updating their outdated tech stacks to support open banking systems — despite the fact that most customers want their FIs to offer open banking supported innovations, such as faster payments.

In “How Fraud Fears Impact FIs’ Adoption of Faster Payment Solutions,” PYMNTS Intelligence noted that “even as consumers value the faster payment solutions that open banking enables, FIs are reluctant to provide open banking solutions due in part to fears of rising fraud, especially as the speed of payment transfers increases.” The report is based on surveys with 200 U.S-based FIs.

Open banking permits FIs and FinTechs to securely share data to enhance the products and services both entities provide their customers, and faster payments is one innovation most consumers want, according to PYMNTS Intelligence.

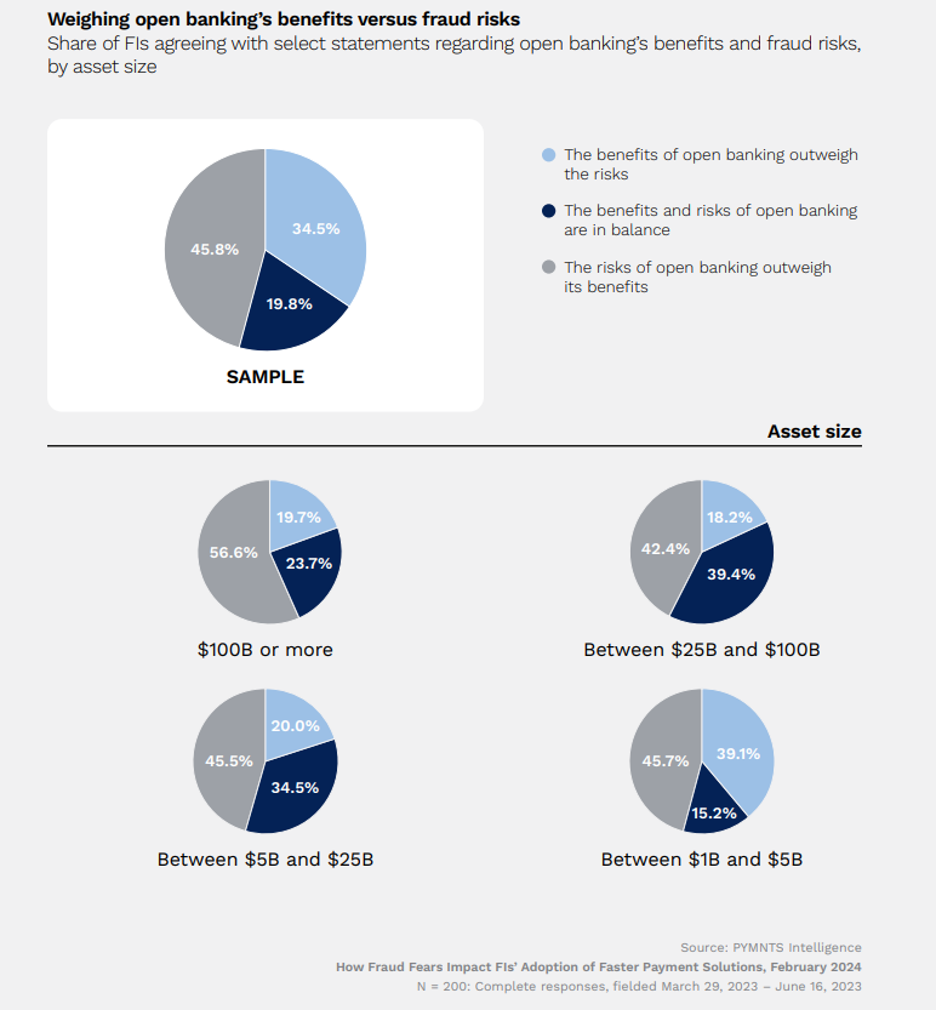

Despite this demand for faster payments, “How Fraud Fears Impact FIs’ Adoption of Faster Payment Solutions,” a collaboration with Hawk AI, found 46% of FIs believe the risk of fraud outweighs any benefits open banking can offer. The percentage of naysayers increases to 57% among FIs that have experienced increased fraud. Only 35% overall believe the benefits outweigh the risks.

The report found that 40% of smaller FIs — those managing between $1 billion and $5 billion — are more comfortable providing open banking solutions. But the comfort level drops off significantly as asset size increases.

Only 20% of those FIs managing between $5 billion and $25 billion believe the benefits of open banking outweigh the risks; while 18% of FIs managing between $25 billion and $100 billion share that viewpoint. When the largest FIs — those managing more than $100 billion in assets — were asked, nearly 57% said the risks of providing open banking outweigh any benefits.

Simply put, smaller FIs may have more to gain by using open banking to develop new products in hopes of attracting new customers. Larger FIs, meanwhile, appear to have much more to lose.