The study “Digital-First Bankingn: Experience-Oriented Digital-First Banking,” a PYMNTS and NCR collaboration, found that all age groups, led by younger generations, are moving toward making digital-only banks their primary providers. However, total consumer adoption of these neobanks is a long way off, with just one in 10 primarily using them. Digital-only banks, therefore, have been looking to gain consumer trust (and thereby market share) through enhanced customer service.

FinTechs’ strategy of being more customized and experience-oriented than their traditional competitors seems to be getting results. While full adoption remains low compared to brick-and-mortar institutions, 59% of consumers said they are somewhat interested in using digital-only banks in the next 12 months, and another 36% are very or extremely interested — indicating growing curiosity, even if most consumers aren’t entirely ready to make the jump.

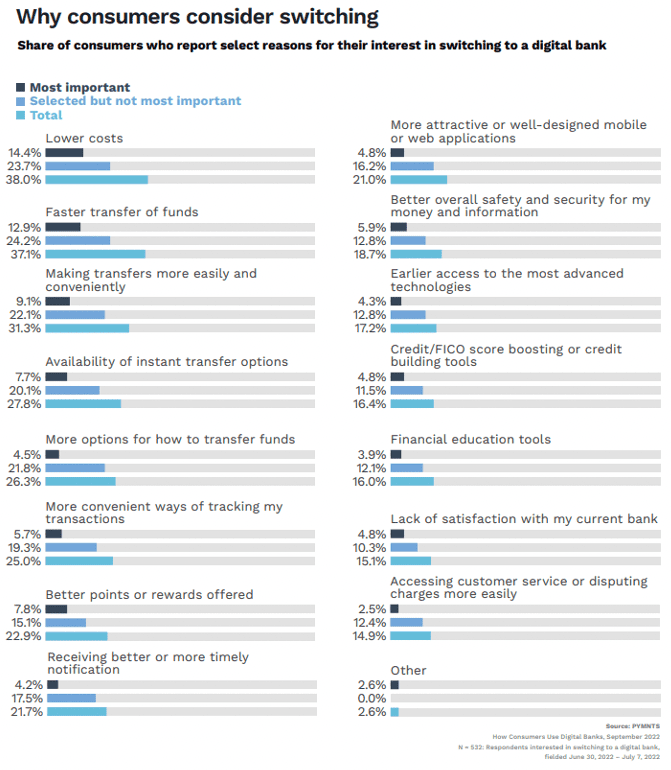

The reasons consumers consider switching primarily to digital-only institutions fall under the larger umbrella of experience-oriented banking. While most larger banks offer some form of digital tools and services, neobanks differentiate themselves by enhancing these offerings.

Amid this year’s record-high inflation rates, digital-first banks like Bunq have rolled out enhanced budgeting tools that allow European users to set different budgets for various household expenses. Bunq detects which category a payment belongs to and assigns funds from the correct sub-account.

One of the biggest loyalty strategies digital-first banks can provide is high-yield savings. Aside from potentially increasing customer retention, the strategy also unlocks additional capital that can enable neobanks to invest in more innovative technology.

Grant Sahag, executive vice president at the neobank Novo, spoke with PYMNTS about how personalization and automation tools can help small businesses stay competitive. If major banks fail to provide these tools, customers will likely find alternative ways to access those capabilities.

“That is why [these tools] have been so disruptive [to the banking market],” Sahag explained. “And that disruption feels [to customers] like getting a more personalized experience.”

Traditional financial services companies seeking to differentiate themselves might take note of how digital-first banks have updated and innovated the tools that brick-and-mortar institutions already offer. The only wrong choice is dismissing these upstarts altogether — because a growing base of digital-minded consumers certainly isn’t.