Buy now, pay later (BNPL) belongs to the young — especially online.

PYMNTS data, gleaned over the last few months, across 2,500 respondents and across a broad range of demographics show that the greenfield opportunity for paying in installments, online and in-store, is a significant one.

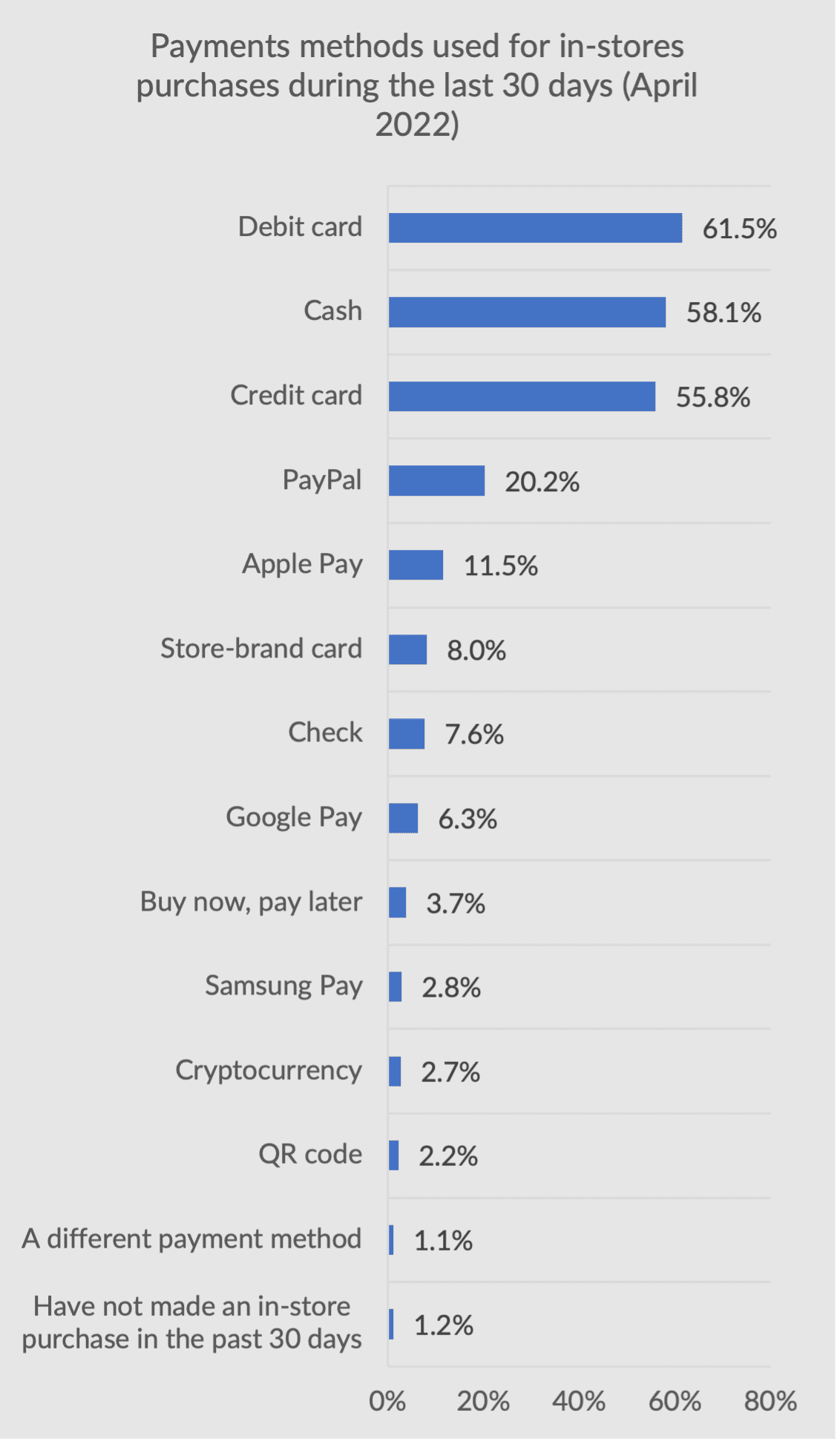

The payment methods that we might deem to be more “traditional” still hold sway, and by a lot, according to our continuing explorations of digital payments. For in-store purchases alone, debit and cash still dominate, and that may make sense given the fact that consumers want to spend the funds that they know they have on hand. BNPL only accounts for about 3.7% of transactions.

Source: PYMNTS (n=2,500)

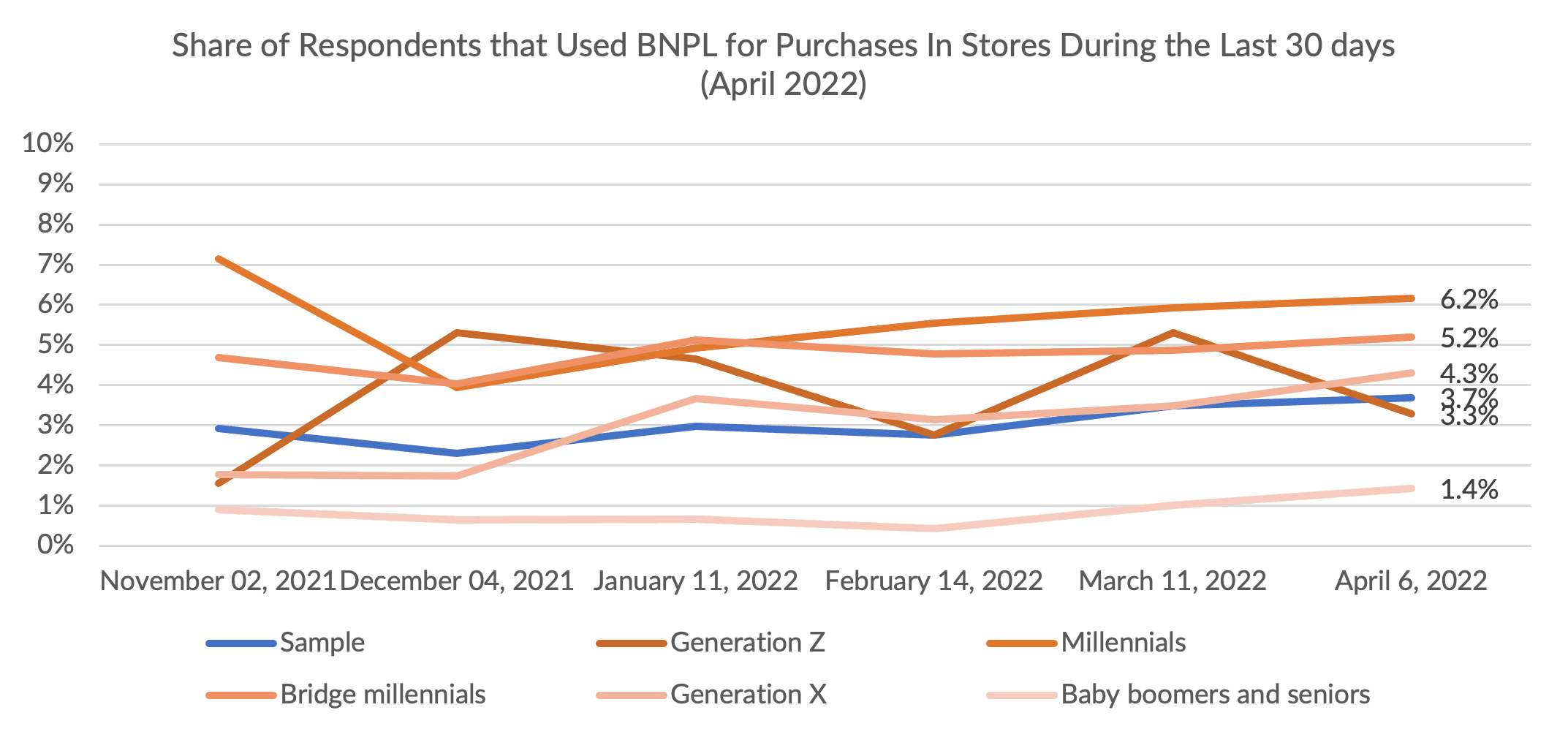

But for in-store commerce, depending on where you look, and especially among younger consumers, BNPL usage is higher than the overall sample’s average. As many as 6.2% of millennials and a bit more than 5% of bridge millennials have used BNPL to get what they need in brick-and-mortar settings, as seen in the chart below. That percentage trumps the 1.4% of baby boomers and seniors who do so.

Source: PYMNTS (n=2,500)

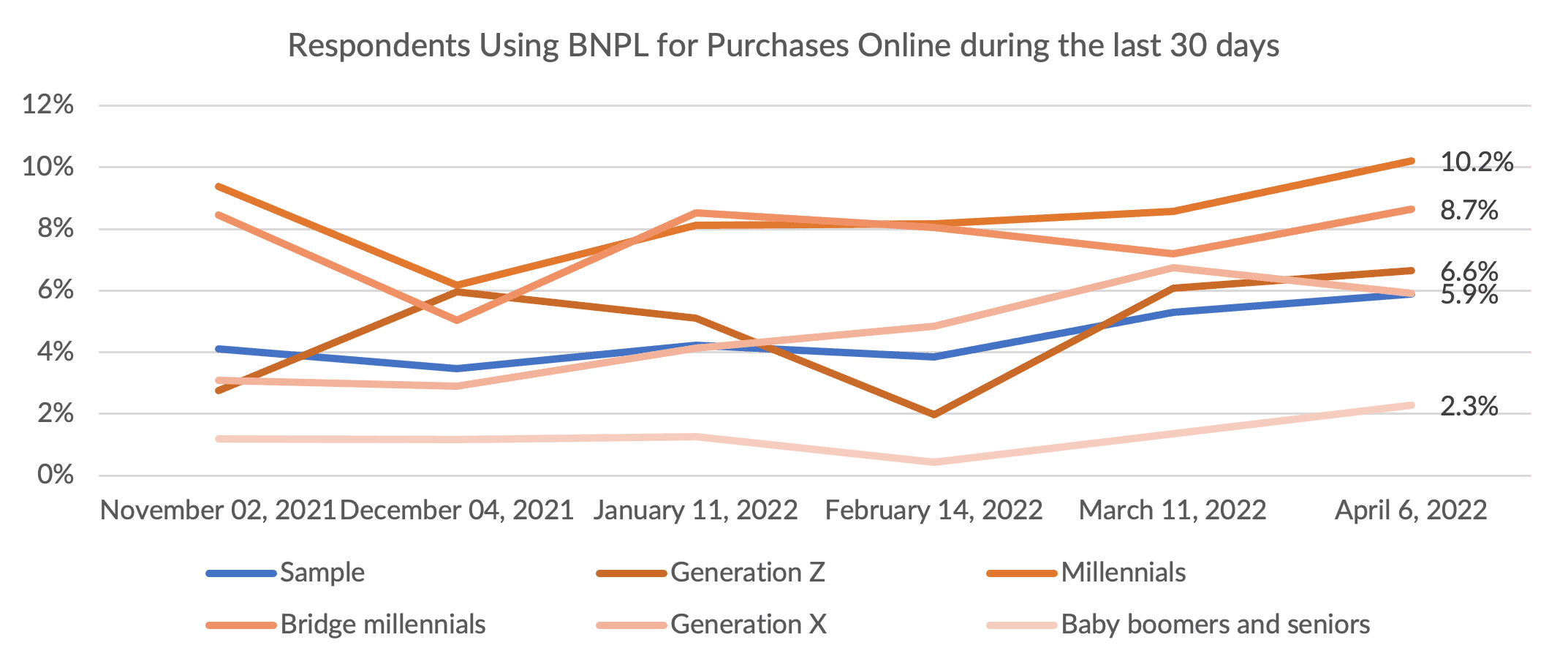

The bifurcation between older and younger consumers becomes even more apparent when shoppers go online to transact. Here we see that 10.2% of millennials have used BNPL — and that’s on a monthly basis. There’s also been a notable bounce in the Generation Z users, as measured from the winter of 2022 into spring of this year, to nearly 7% where the tally had been only 2% earlier.

Source: PYMNTS (N=2,500)

We might assume that BNPL holds particular appeal in the midst of the paycheck-to-paycheck economy. Consumers are keeping a closer eye on their respective pocketbooks in an inflationary environment where paying the bills gets harder and harder. Separate PYMNTS data indicates that as many as 70% of millennials live paycheck to paycheck.

Generation Z consumers who live paycheck to paycheck and have issues paying their monthly bills report the lowest average savings at just $1,158, according to PYMNTS’ findings. Millennials living paycheck to paycheck with issues paying their monthly bills report the highest savings, with an average of $3,731. Savings amounts decrease and then level off as consumers grow older.

Read also: Millennial Minute: 70% of Millennials Live Paycheck to Paycheck

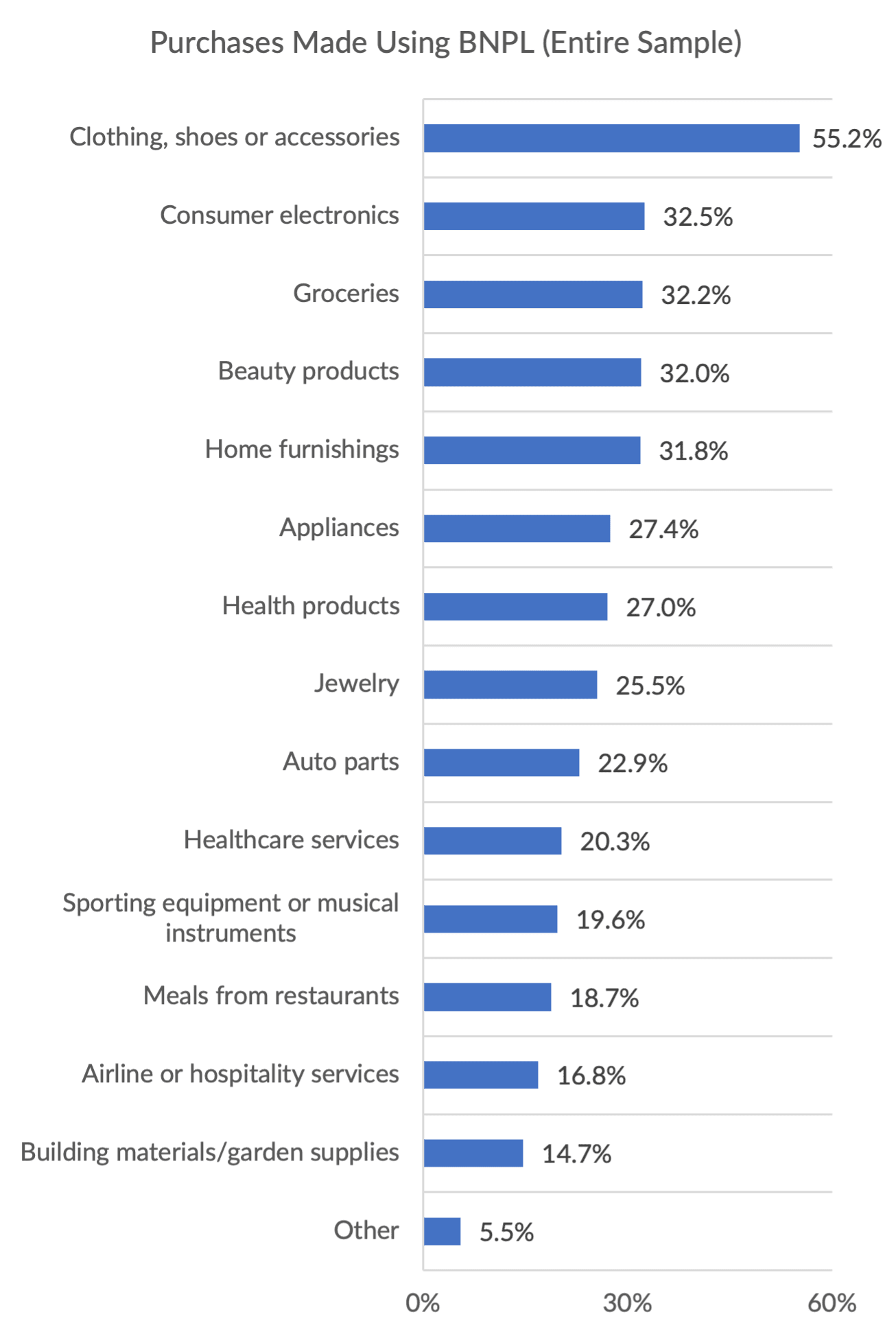

As to what they’re buying: millennials and bridge millennials closely hew to the categories seen below, which are representative of the entire 2,500-consumer sample that we surveyed. Roughly 56% of younger consumers use BNPL for everyday items such as clothes, shoes and accessories, while about 35% opt to purchase consumer electronics with that payment method.

Source: PYMNTS (n=2,500)