The velocity of technological advancement has sped the arrival of digital-centric lifestyles and business models — even new industries in some cases — all now coming under the umbrella of what PYMNTS now refers to as the ever-expanding ConnectedEconomy™.

Measuring the pace of change as consumers and businesses alike lean into digital in practically everything from shopping to paying to deciding what kind of financial institution (FI) to deal with, be it legacy bank or challenger, PYMNTS inaugural report, How Consumers Live In The ConnectedEconomy™, based on a survey of over 15,000 U.S. consumers, is first in a new series exploring the undiscovered country of connected experiences and tech streaming to market.

Per the June study, “The rise of a ConnectedEconomy™ ecosystem — enabled by 5G, IoT, machine learning, AI and innumerable connected devices — has the potential to make consumers’ digital experiences more seamless and deeply integrated into their daily lives,” adding that “segments of the economy that have historically operated … in silos, like brick-and-mortar retail, payment processing and delivery services, are now deeply integrated.”

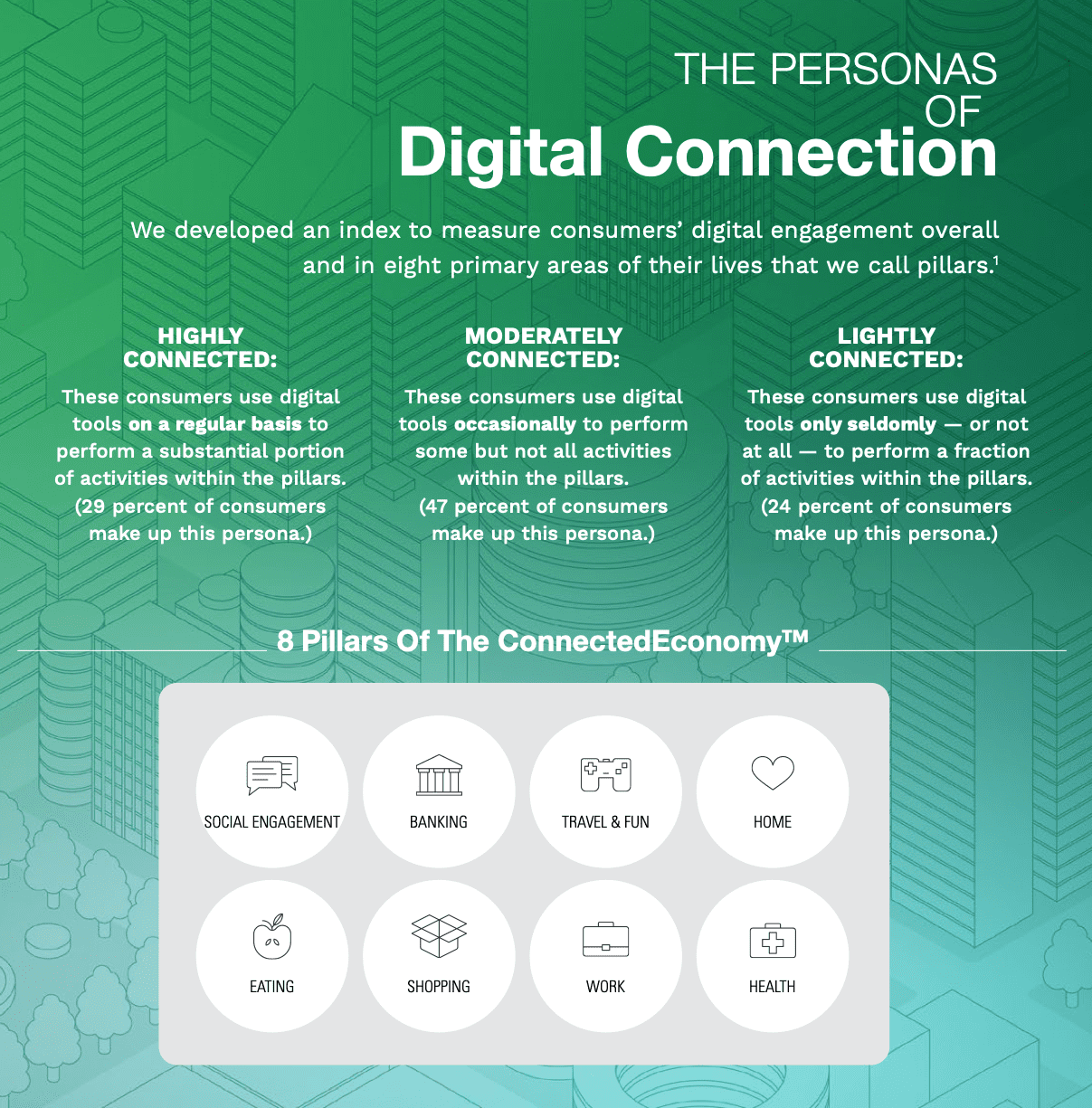

Demonstrating how the new connectedness is organizing itself by all manner of preference, PYMNTS researchers have identified eight “pillars” of the ConnectedEconomy™, as well as rapidly emerging consumer personas that map to the connected “Big 8” drivers.

Devices Bringing It All Together

The depth and breadth of findings from How Consumers Live In The ConnectedEconomy™ is daunting, and it’s no shocker that devices, data and trust all play decisive roles, coming together as they now are under the rubric of horizontal payments spanning commerce.

“Several data points from our research illustrate how strongly consumers have taken to digital tools over the past 15 months,” per the study, with 92 percent of all consumers placing online orders for products and/or services. “More than 85 percent have paid bills online and managed their banking online, and 72 percent have booked hotel tickets online,” per the study.

Additionally, over 70 percent of consumers have paid their bills online in recent months, as well as account-to-account transfers and payments apps including PayPal and Venmo.

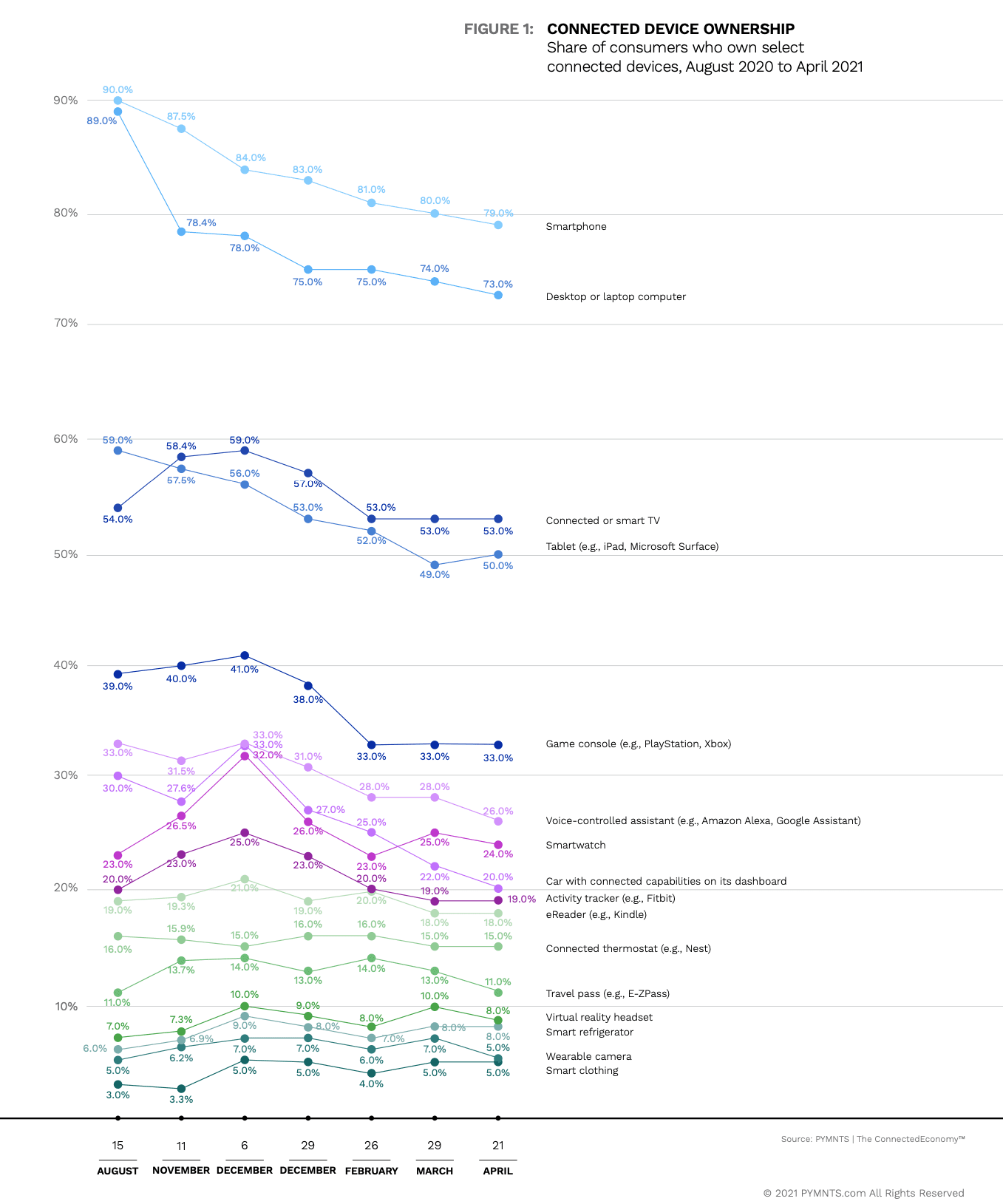

There’s no ConnectedEconomy™ without digital devices, and findings around device ownership contain some surprises. “Despite the abundance of gadgets on the market, the average number of devices owned appears to be leveling off, dropping slightly below five after rising for several years. Even among the most avid device aficionados — a group we have previously termed the super-connected in our research — the average number has plateaued at around seven.”

Additionally, 92 percent of consumers have placed an online order for a product and/or service “at least once recently, with over three-quarters conducting “at least some banking online.”

Payments Lead The Way

The more connected one is the more they wish to be, based on study findings. “Consumers who are highly connected at home, for example, are also likely to be highly connected in the banking (91 percent), travel and fun (92 percent) and health (84 percent) pillars,” researchers found.

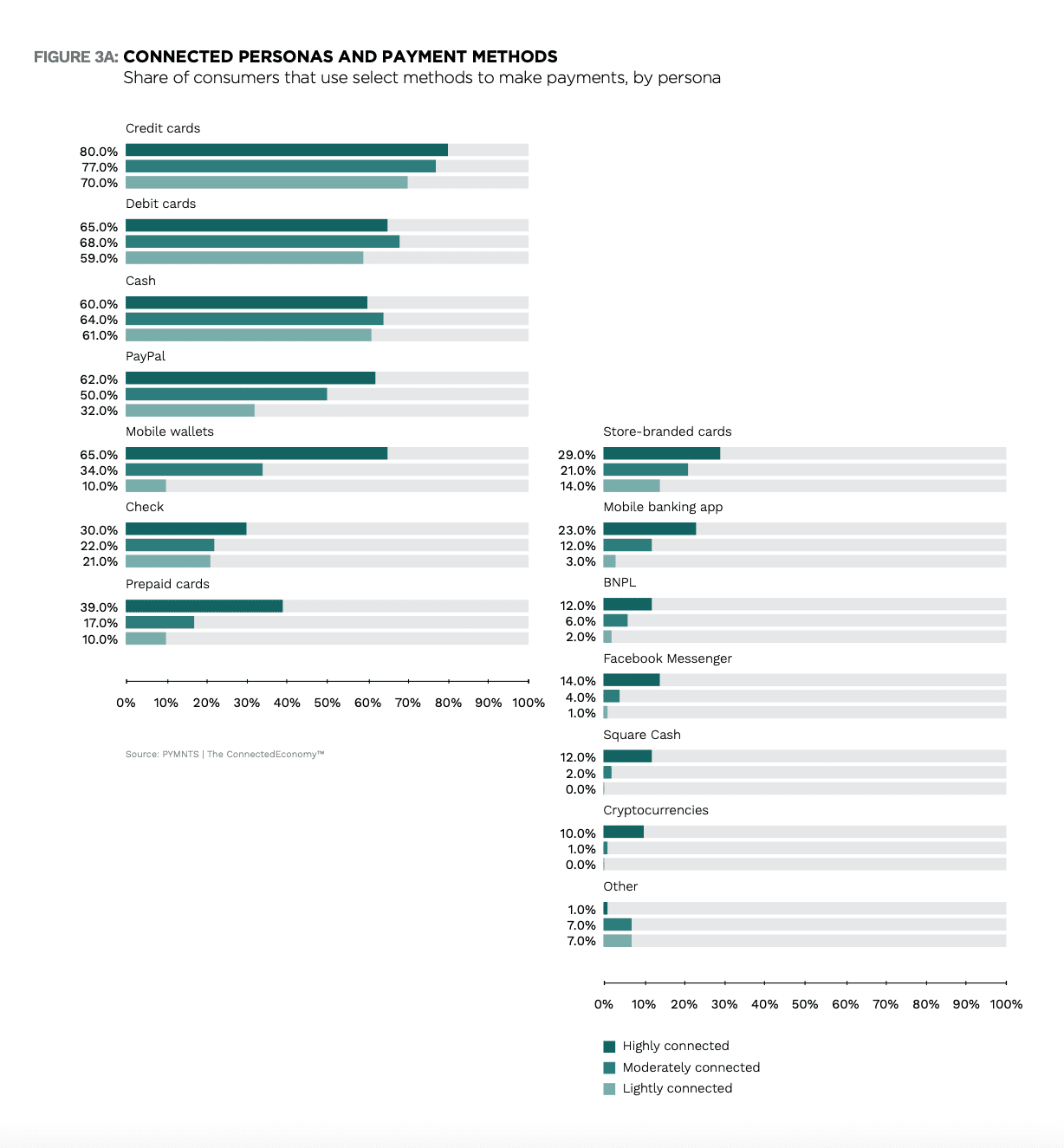

That trend has legs, with 62 percent of the highly connected having received payments into mobile wallets at least once in the past year — twice that paid by check or direct deposit.

“Highly connected consumers also tend to use a robust array of methods to make payments. Majorities of them use four distinct methods: Credit cards are most common – 80 percent of them have used the payment method over the past 12 months – but mobile wallets and debit cards tie for second at 65 percent, while PayPal rounds out the list at 62 percent.”

Larger shares use ecommerce for both retail products (66 percent) and groceries (56 percent) than those shopping physical locations (50 percent and 54 percent, respectively).

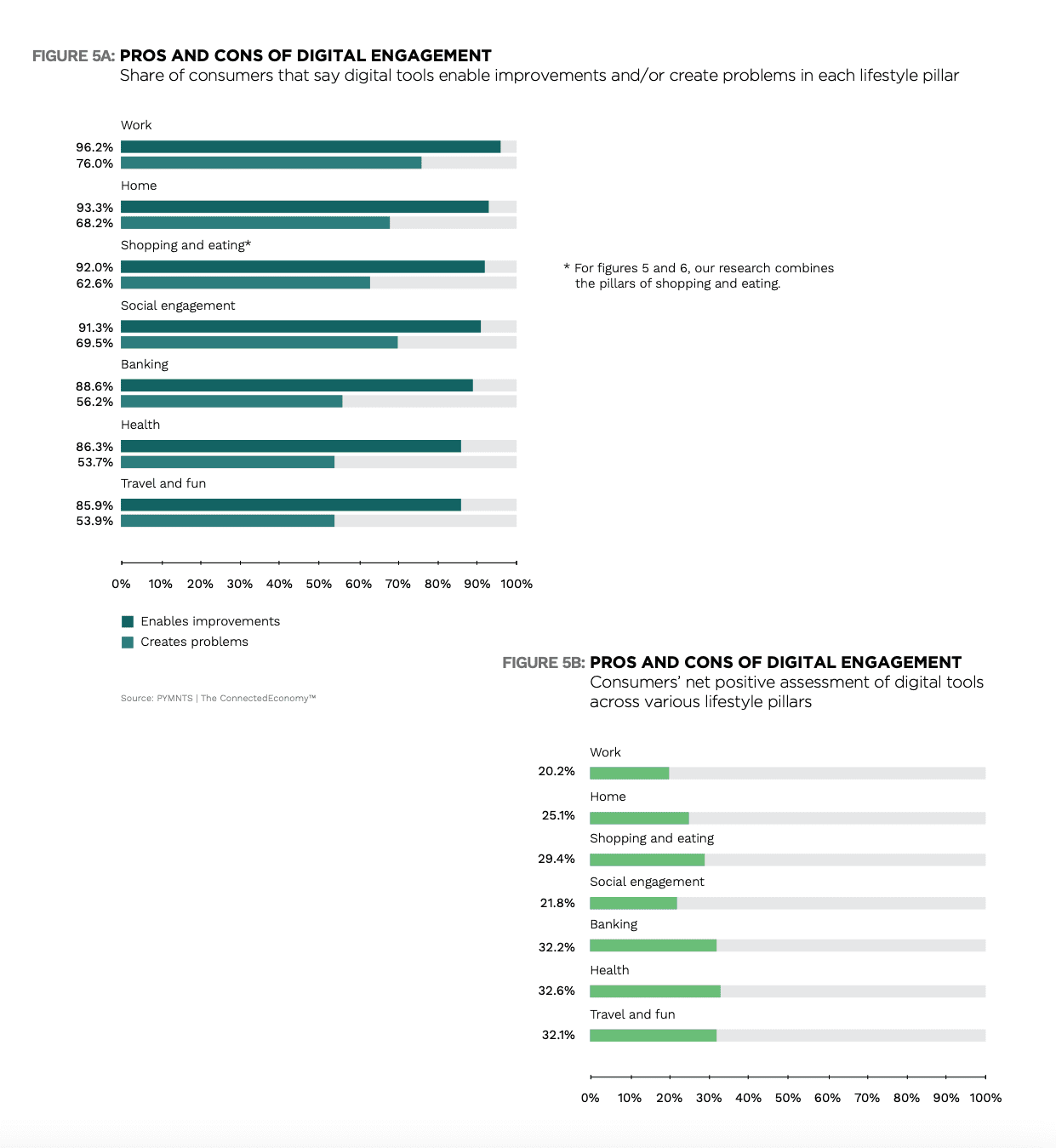

Weighing ConnectedEconomy™ Pros And Cons

Other data analyzed for How Consumers Live In The ConnectedEconomy™ paints a picture of perceived risks and rewards of embracing a completely connected lifestyle.

“The pros and cons of digital engagement vary by pillar. In the working realm, for example, 54 percent cite productivity and ease and convenience as benefits, while approximately one-quarter point to wasted time and communication breakdowns as downsides.”

Another 60 percent like the ease and convenience of digital particularly in the shopping pillar, while roughly 21 percent “have concerns about wasting time and money. Security is a standout concern in the home environment, cited by 30 percent. This is understandable, as appliance hacking and data breaches could quite literally strike close to home.”

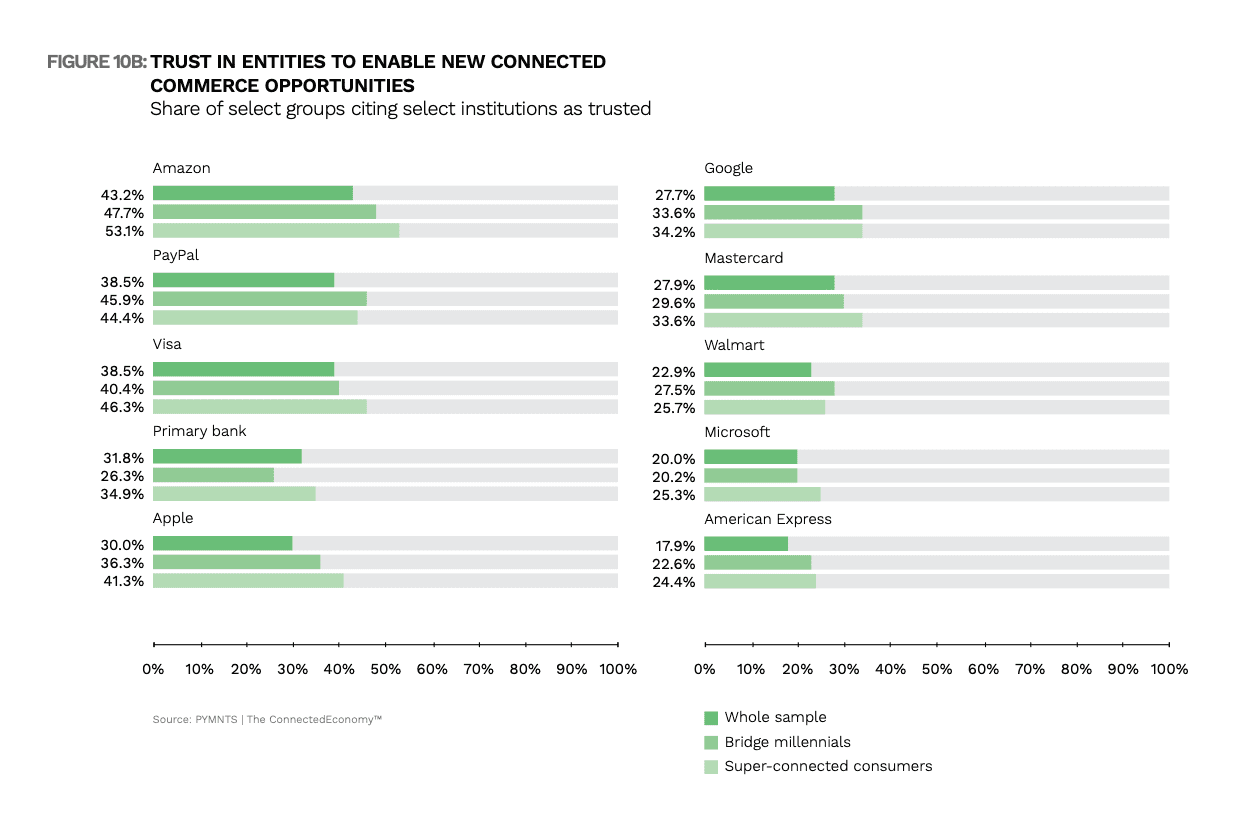

On Trust And ‘Super-Connectedness’

Data and trust go everywhere today hand-in-hand, nowhere more so than in connected experience. There can’t be one without the other, and somewhat alarmingly for legacy financial institutions (FIs), Big Tech is assuming a mantle of reliability people once reserved for banks.

“These trends are even stronger among ‘super-connected’ consumers — those that own at least six connected devices — and bridge millennials,” per the study, adding that “most trusted connected commerce enablers among super-connected consumers are Amazon (53 percent), Visa (46 percent), PayPal (44 percent), Apple (41 percent) and primary banks (35 percent).”