About 62% of consumers in the United States live paycheck to paycheck, often face difficulties paying their monthly bills, and rely on credit cards to manage their cash flows.

Consumers living paycheck to paycheck own almost 60% of credit cards in the U.S., with these individuals owning two credit cards on average.

These are some of the key findings detailed in PYMNTS Intelligence’s “The Credit Card Use Deep Dive Edition” of the New Reality Check: The Paycheck-to-Paycheck Report series. The study drew on insights from a survey of over 3,250 U.S. consumers to examine their financial lifestyles and explore how they use credit cards to manage their finances.

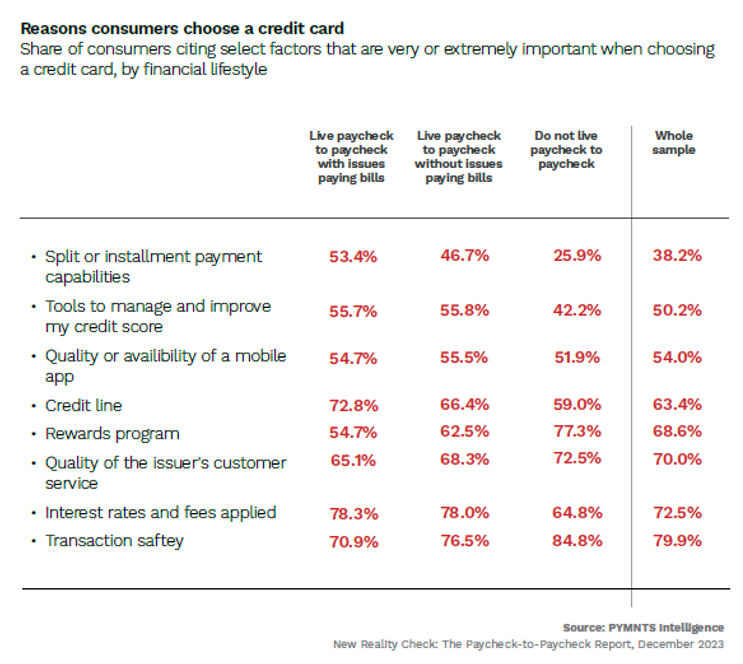

When it comes to reasons why consumers choose a credit card, the study found that nearly 80% of consumers overall prioritize transaction safety.

Specifically, 85% of consumers without paycheck pressures, 77% of those living paycheck to paycheck without issues paying bills and 71% of those living paycheck to paycheck struggling to pay bills said transaction security is highly important when choosing a credit card.

Following transaction security, consumers regard interest rates and fees, along with the quality of customer service provided by the issuer, as highly significant factors when selecting a credit card, cited by 72% and 70%, respectively. Subsequently, rewards programs are considered important by 68% of consumers.

The report also revealed that non-paycheck-to-paycheck consumers prioritize rewards programs the most, with 77% citing this as an important consideration when choosing a credit card. These individuals have more financial stability and can focus on maximizing the benefits and protection offered by their credit cards.

On the other hand, 55% of paycheck-to-paycheck consumers struggling with bill payments view rewards as significant. Instead, they prioritize interest rates (78%) and credit limits (73%) as extremely important factors to consider when selecting a primary credit card.

This discrepancy suggests that financially strained consumers rely on credit cards for financing, while those financially stable perceive them merely as another payment method, the study noted.

Drilling further down into the data showed that financial distress correlates with increased use of installment or split payment plans. While 25% of cardholders overall have pending repayments through installment plans, only 15% of cardholders not living paycheck to paycheck do.

However, the likelihood of pending repayments rises among paycheck-to-paycheck individuals, with 43% of those struggling to pay bills using split payment plans to manage cash flows compared to 26% of those without bill payment issues.

Overall, understanding the reasons behind consumer credit card use patterns can help credit card providers tailor their offerings to meet the specific needs of different consumer segments, and by doing so better serve their customers and foster financial stability.