It was once assumed that bank customers would bring their children on board to become lifelong customers themselves, but a new study indicates that this assumption is no longer valid. Less than half of Gen Z and millennials surveyed used the same financial institutions (FIs) as their parents in 2021, down from 61% and 54%, respectively, in 2020. In addition, more than 60% of these two age groups would consider switching FIs for better mobile banking apps or digital capabilities.

Digital banking preferences depend largely on generational differences and comfort with technology. While older generations may still prefer face-to-face interactions with tellers and occasional visits to the ATM, younger and tech-savvier banking consumers are looking to avoid trips to the bank altogether in favor of mobile apps that allow safe, seamless service in the palm of their hands.

Credit unions (CUs) are under pressure to compete with banks and FinTechs, making it crucial for them to invest in technology infrastructure to give members of all generations the experiences they demand. This month, PYMNTS Intelligence takes a close look at CU members’ digital banking expectations across all generations and the steps credit unions must take to attract those members and stay in step with profit-driven banks.

The Demands of Different Generations

No matter how they choose to do their banking, consumers still expect a guiding partner in their financial lives. The success of any FI platform will depend on the organization’s willingness to cater to the changing needs of younger consumers while not alienating loyal, longtime patrons.

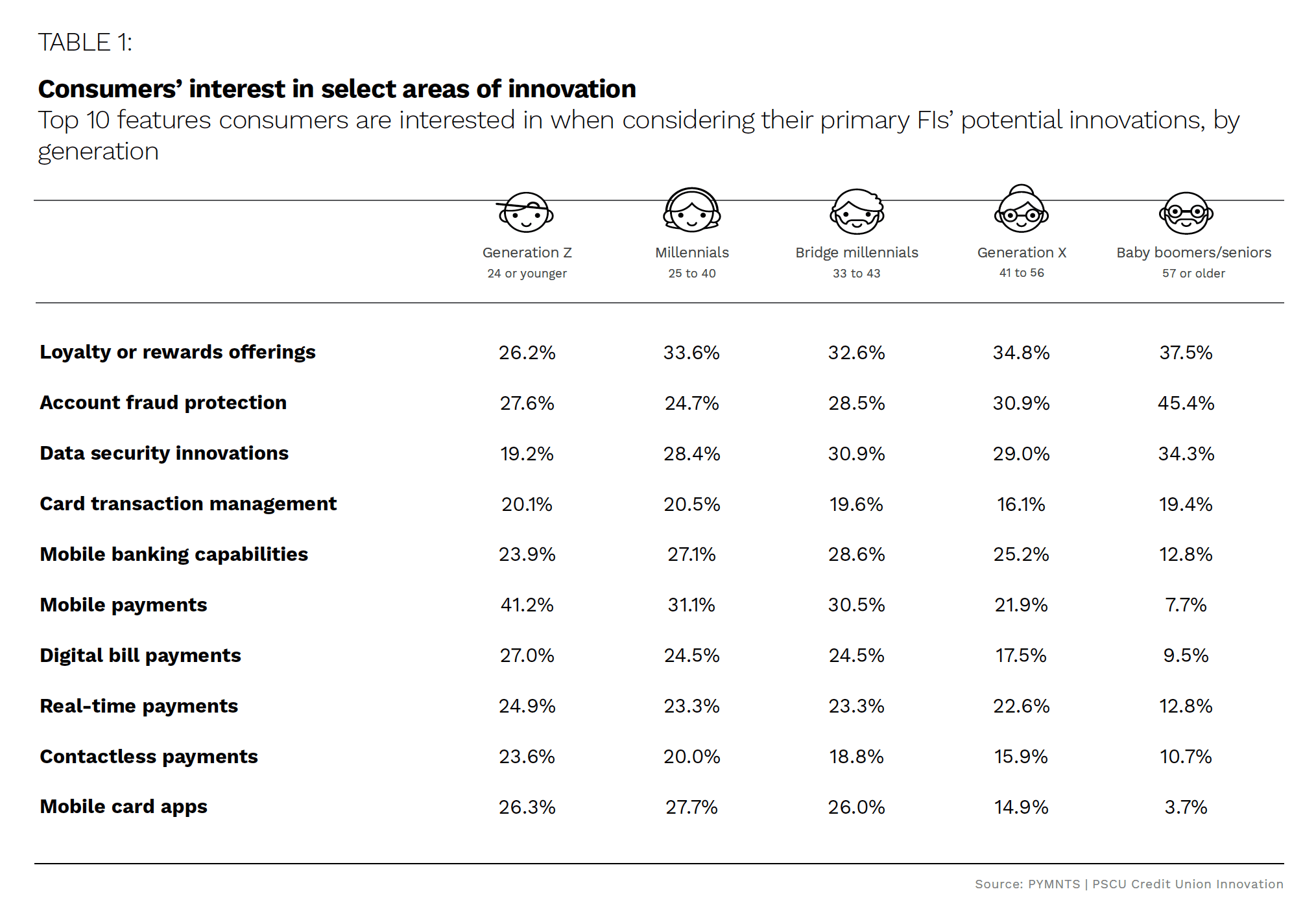

PYMNTS’ research found that 15% of Gen Z consumers are dissatisfied with their current FIs, representing an opportunity for CUs that want a piece of the younger-demographics pie. Some 40% of this generation said high costs are a source of frustration, while nearly one-quarter said poor-quality mobile services and difficult-to-navigate bill pay options left more to be desired. Although just 5.3% of millennials and 6% of bridge millennials said they were unsatisfied, these latter demographics also prefer the digital convenience of mobile banking, real-time bill payment options and online chats with their FIs.

Younger banking consumers tend to be more vigilant with their finances, and research shows that more than 60% of millennials and Gen Z consumers aim to increase their savings. This is one reason digital planning and budgeting tools are finding a niche with these age groups. Not surprisingly, baby boomers and seniors are more interested in security and fraud protection than in such innovations.

Credit unions must work to reposition themselves with younger consumers, as research shows that just 26% of those 18 to 24 years old belong to CUs, with 36% preferring national banks with better name recognition. Individuals between the ages of 25 and 34 are even less likely to use credit unions at 14%, with 28% preferring national banks and 31% preferring online banks. Interestingly, the very youngest demographics are not the only ones at stake, as those ages 35 to 44 are even greater fans of online banks at 36%, and just 19% bank with credit unions. CUs remain in strong favor with older generations, as 60% of those ages 65 and older are members. With smaller budgets, CUs tend to have fewer marketing dollars to attract younger cohorts, who may not be familiar with CUs as an option.

CUs Move to Satisfy Each Generation

CUs have been slower to adopt new technology, with PYMNTS research showing that roughly 19% are early adopters or innovators. Nevertheless, CUs realize that consumers want more digital offerings and are ramping up investments to stay competitive. Some 74% of CUs made investments in mobile banking in 2021, for example, up from 70% in 2020. Furthermore, 64% adopted mobile wallet technology, and half of CUs now offer peer-to-peer (P2P) payments capability, nearly double the number from a year earlier. By the end of 2022, just 4% of credit unions will not have begun a digital transformation strategy.

A growing number of younger consumers show interest in using cryptocurrency to make transactions, and some CUs have entered partnerships with FinTechs that allow them to invest and trade using bitcoin. One-quarter of CUs plan to implement real-time payments capability in 2022, and many already plan to make it easier to open accounts digitally, provide communication tools such as chatbots, make it easier to apply for loans and provide buy now, pay later (BNPL) options.

Credit unions have an important place in the financial marketplace, as 94% of their members report being satisfied with their CUs as financial providers. To spread the word and continue attracting new members, CUs must keep current with consumer demand and take risks by investing in technologies that can help members of all ages along their financial journeys.