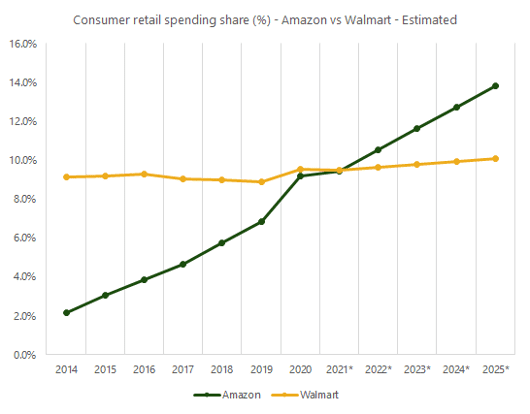

This after PYMNTS’ data for the fourth quarter and full year showed that, after Amazon has been chipping away at Walmart’s lead for more than a decade, the two titans of retail are now in a neck-and-neck dead heat, with each controlling approximately a 9 percent share of total U.S. retail sales.

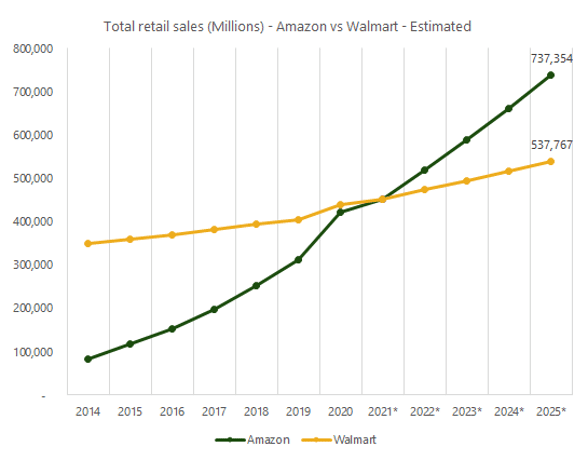

However, as the below graph shows, new research by PYMNTS has now gone one step further, projecting that by the middle of next year, Amazon will have begun to pull away from Walmart in terms of both share of U.S. retail sales and the dollar value of those sales.

The leadership change is significant because, looking back six years, Walmart’s $350 billion in annual sales were more than triple Amazon’s revenue. However, looking forward five years, PYMNTS is projecting that Amazon will be doing roughly $737 billion in sales, for a $200 billion or 37 percent revenue margin over Walmart’s projected $537 billion revenue target for 2025.

Similarly, when measured by domestic market share, PYMNTS data shows Amazon breaching the current tie by 2022, and then opening up a four-percentage-point share advantage in the next four years of roughly 14 percent to 10 percent.

Editor’s Note: It is important to acknowledge that PYMNTS data and projections look at the broadest measure of retail activity by tabulating gross merchandise value (GMV) — or the value of everything actually sold, except gasoline — rather than officially reported top-line revenues, which only reflect the commission earned on certain items sold for other vendors through Amazon’s and Walmart’s respective marketplaces.

For example, if Amazon sold a $50 set of knives but only booked $5 in revenue, assuming it charged the merchant a typical 10 percent referral fee, PYMNTS’ use of the former metric provides a more holistic view of where consumers are actually spending their money.

Top Line vs. Bottom Line

Officially, for the three months ending March 31, the average forecast of 37 analysts who cover Amazon is $9.50 per share, within a range that goes from as low as $6.50 and as high as $12.00. At the same time, analysts are expecting $105 billion in Q1 revenue, up about 30 percent from the $75 billion in sales it posted a year ago — just six weeks into the COVID lockdowns.

However, it is important to keep in mind that roughly 13 percent — or $10 billion — of that $75 billion reported in 2020 came from the lucrative Amazon Web Services division, which also accounted for almost 80 percent of the Seattle-based retailer’s total quarterly profits.

Amazon is also generating more income from its media division, but those gains have been tempered by a spate of enormous expenditures on content, including a deal with the NFL as well as a string of original shows and films.

Checkout Line

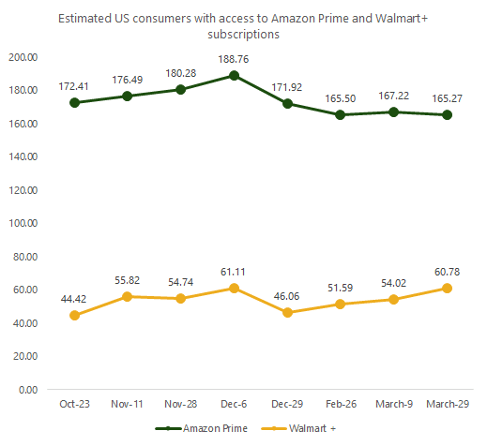

As much as investors will be keen to evaluate any top- and bottom-line changes, Amazon itself is currently focused on stemming the gains that the new Walmart+ subscription service has recently strung together. In fact, in just seven months, the Walmart+ membership program has built a base of more than 60 million U.S. consumers who subscribe to the $98-per-year service, which provides online delivery, in-store savings and convenience offerings.

Although the total gap between Walmart+ and rival Amazon Prime is still a formidable 100 million members wide, the upstart entry from Arkansas has been trending higher in the first quarter of 2021, at a time when the dominant digital leader has experienced a few months of slippage in its overall share of the category.

To cut into Walmart’s dominance of the food and beverage category, Amazon has been quietly adding to its portfolio of Amazon Fresh stores alongside its 500 existing Whole Foods locations, in the face of its rival’s 5,000 domestic outlets that offer modern conveniences such as in-store and curbside pickup.

The Post-Pandemic Trend

A year ago, with COVID raging and the country on lockdown, Jeff Bezos, Amazon co-founder and soon-to-be executive chairman, characterized the climate as “the hardest time we’ve ever faced.”

Fast-forward to the present, and the retailing giant has not only delivered its strongest, most profitable year ever, but is preparing to welcome AWS Chief Andy Jassy to the CEO role after solidifying its 50 percent grip of the online retail sales market.

While platforms such as Shopify have tried to prepare investors that the pace of eCommerce growth will slow this year as consumers revert back to so-called offline or in-store shopping, investors will be eager to hear Amazon’s insights as to how much of the recent gains made during the digital shift will remain.

Amazon will report its first-quarter earnings after the close of trading on Thursday (April 29). The company’s stock is worth more than $1.7 trillion after rising 47 percent in the past year.