Data from the Federal Reserve and the Census Bureau hint at a looming crunch on Main Street.

Specifically: The businesses that power the economy are finding it harder to get the credit they need to grow, or even stay in business. And there are fewer newer firms starting up, which could conceivably keep the economy growing, or replace the businesses that might shutter operations.

The Census Bureau’s latest reading on business formation for April shows that on a seasonally adjusted basis, applications totaled a bit less than 434,000, down 4.2% from March’s levels. The bureau’s projected formations, looking out over the next four quarters, forecasts a 4.7% decline. We’re a far cry from the depths of the pandemic where, for example, in July, the stats showed 552,000 applications.

And within the latest report, we can see that retail trade applications were down 6.9% month over month, professional services firms applications were down 2.6%, construction firms sank 2.4% in month over month, and accommodation and food services applications were down a muted 0.3%.

No Easy Access to Funding

As for the capital crunch: the Federal Reserve reported the value of commercial and industrial loans from all commercial banks was $2.77 trillion in April, down slightly from $2.78 trillion in March, and down from more than $2.8 trillion in January — and where the recent monthly peak in the midst of the pandemic was $3 trillion in May 2020.

Advertisement: Scroll to Continue

The trends have been in place for a while. Separately, the Kansas City Fed released data at the end of March that shows that coming into the end of 2022, and specifically for smaller businesses in the fourth quarter, total new small business balances plummeted by 19.3%, driven by a 19.8% decrease in new term loans and an 18.5% decrease in new lines of credit.

The crunch is real: In the April PYMNTS Main Street Survey on business sentiment, we found that overall only a small percentage of companies — 26% — have access to the equivalent of two months of revenue in the bank. Another 17% have access to no emergency funding. And like everybody else, these companies are grappling with inflation, which is eating steadily away at margins and on cash that they do have on hand.

The firms that are most in trouble are the ones that operate precisely in the verticals where, as detailed by the business formation stats, there have been declining applications. The read-across here is that if some of these Main Street mainstays go dark, there may not be a replacement in the wings — and specialized, skilled labor may find it a bit harder to find work if that does happen.

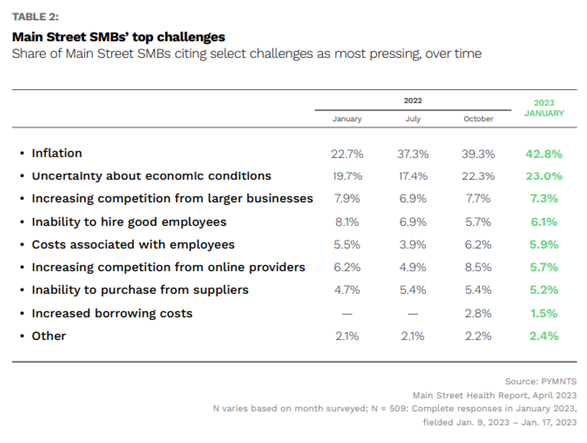

As many as 64% of personal services SMBs and 55% of construction and utility small businesses have no financing options readily available, we found, and 44% of Main Street retail SMBs say they have no financing available. The chart below details the key concerns SMBs have had coming into the year as 59% expect a recession — with inflation, and economic uncertainty topping the list.

And those concerns, we note, might be enough to give would-be Main Street entrepreneurs pause, too.

#image_title