Access to business financing is crucial for small and medium-sized businesses (SMBs) on Main Street — firms generating less than $10 million in annual revenue and having physical locations from which they conduct their business within core commercial districts of cities or towns.

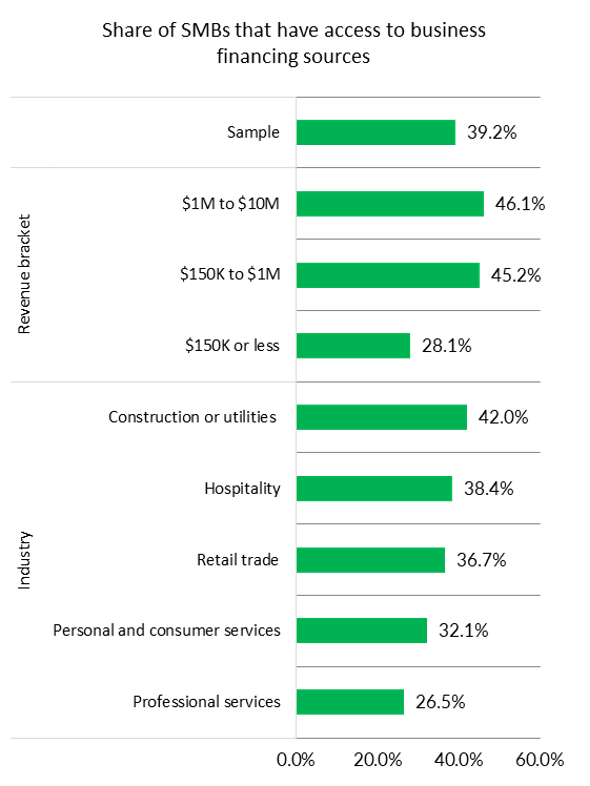

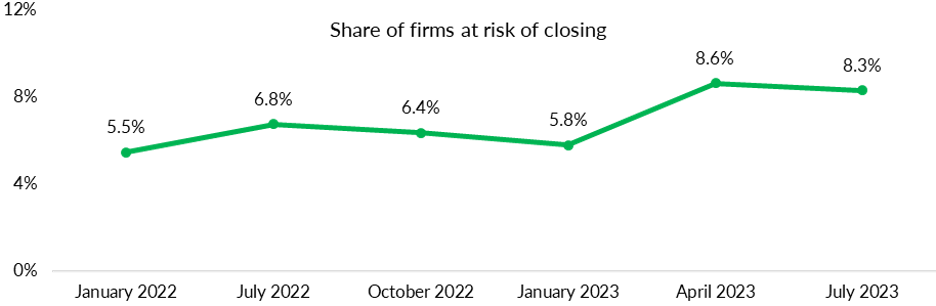

But according to PYMNTS Intelligence research, only 39% of these SMBs have access to financing sources such as business credit cards and working capital loans, with 8% of these Main Street SMBs are at risk of closing shop.

Drilling down into the data shows that firms in the hospitality industry (11%) and retail trade (10%) sectors have a slightly higher likelihood of ceasing business operations.

This aligns with recent news on small business bankruptcies surging, as PYMNTS reported by PYMNTS on Sunday (Oct. 1) per The Wall Street Journal (WSJ).

According to the WSJ report, nearly 1,500 small businesses filed for bankruptcy under Subchapter V of the bankruptcy code — a provision making it easier for small businesses to restructure — in the first nine months of 2023, almost matching the total number for the whole of last year.

Additionally, defaults and delinquencies on small business loans have surpassed pre-pandemic averages, the WSJ noted, per Equifax data. The report attributed this surge to small businesses’ lack of ability to issue stock or seek funding from sources like private equity investors, unlike larger companies.

This limited access to capital makes them more vulnerable to economic fluctuations, particularly when interest rates rise. Moreover, the inability to secure affordable financing can lead to financial strain, making it difficult for small businesses to sustain their operations and meet their financial obligations.

Dwindling Cash Reserves

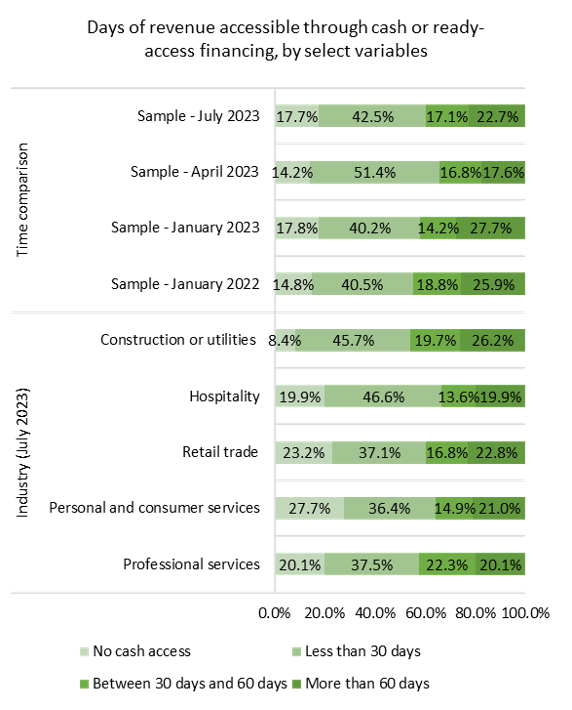

This challenging economic environment has also impacted firms’ access to cash, PYMNTS Intelligence research shows, with 18% Main Street SMBs having no access to cash as of July this year, up from 15% in January 2022.

Among those affected, personal and consumer services firms face the greatest challenge in cash access at 28%, followed by SMBs in the retail trade (23%).

Overall, most Main Street SMBs have a $28,000 cash cushion, with the amount of ready-access cash across sectors representing less than half of average monthly sales.

That and challenges related to the economy will continue to be a challenge for most SMBs as 45% of SMBs point to inflation and almost 20% cite the uncertainty of economic conditions, respectively, as their biggest challenge.

However, more than half of the Main Street SMBs remain bullish about the future. In July, 57% of these businesses expected their revenues to increase compared to July of last year — a trend that has remained relatively stable since January 2023.

Middle Market Firms Tap Working Capital to Improve Performance

The high cost of accessing working capital is particularly challenging middle market firms, companies typically generating annual revenues ranging from $50 million to $1 billion.

These firms often find themselves in a dilemma, as existing financial solutions are not tailored to their specific needs, which fall between small businesses and large enterprises.

Findings detailed in a study done by PYMNTS Intelligence and Visa titled “The 2023 Growth Corporates Working Capital Index” shows that working capital has been instrumental to middle market firms’ business growth, with 70% of corporates that used working capital solutions seeing improved business metrics as a result.

In fact, top-performing growth corporates made an average $3.3 million annually in accounts payables (AP) savings, reduced days payable outstanding (DPO) by five days and improved cash conversion cycles.

The study further reveals that using working capital for strategic purposes including to cover predictable cash flow gaps and growth initiatives, enabling firms to pay suppliers earlier than expected and integrating more suppliers in payment systems, which in turn leads to discounts and better vendor relationships as well as reduced errors, delays and human resource’s time.

Additionally, instead of overdrafts and loans which are an expensive substitute for other forms of strategic growth capital, virtual credit cards have proved critical for middle market companies, the PYMNTS study further reveals.

In fact, utilization of virtual cards has skyrocketed in recent years, with middle market firms expected to triple its use in 2024.

Utilization of this solution — considered the “Swiss Army Knife” of working capital solutions by CFOs — has been associated with increased operational efficiencies, driven by higher supplier integration and versatility in types of utilization.

Looking ahead, nearly all middle market firms plan to increase their use of financing in 2024, with most of them seeing it as a tool to fund strategic growth in today’s uncertain macroeconomic environment.