In payments, complexity reigns, and making payments simple, transparent and speedy is anything but easy.

That’s especially true with cross-border payments, where commerce done globally demands that firms be aware of regulations and payments preferences that are endemic to a specific country or even specific region. Infrastructure can be varied, too, in terms of technology.

Fragmentation reigns, then, and as detailed in the Simplifying Cross-Border Payments Playbook, as firms strive to connect cross-border fund flows, any number of considerations are paramount. These include security and grappling with legacy systems in the embrace of real-time payments.

Data:

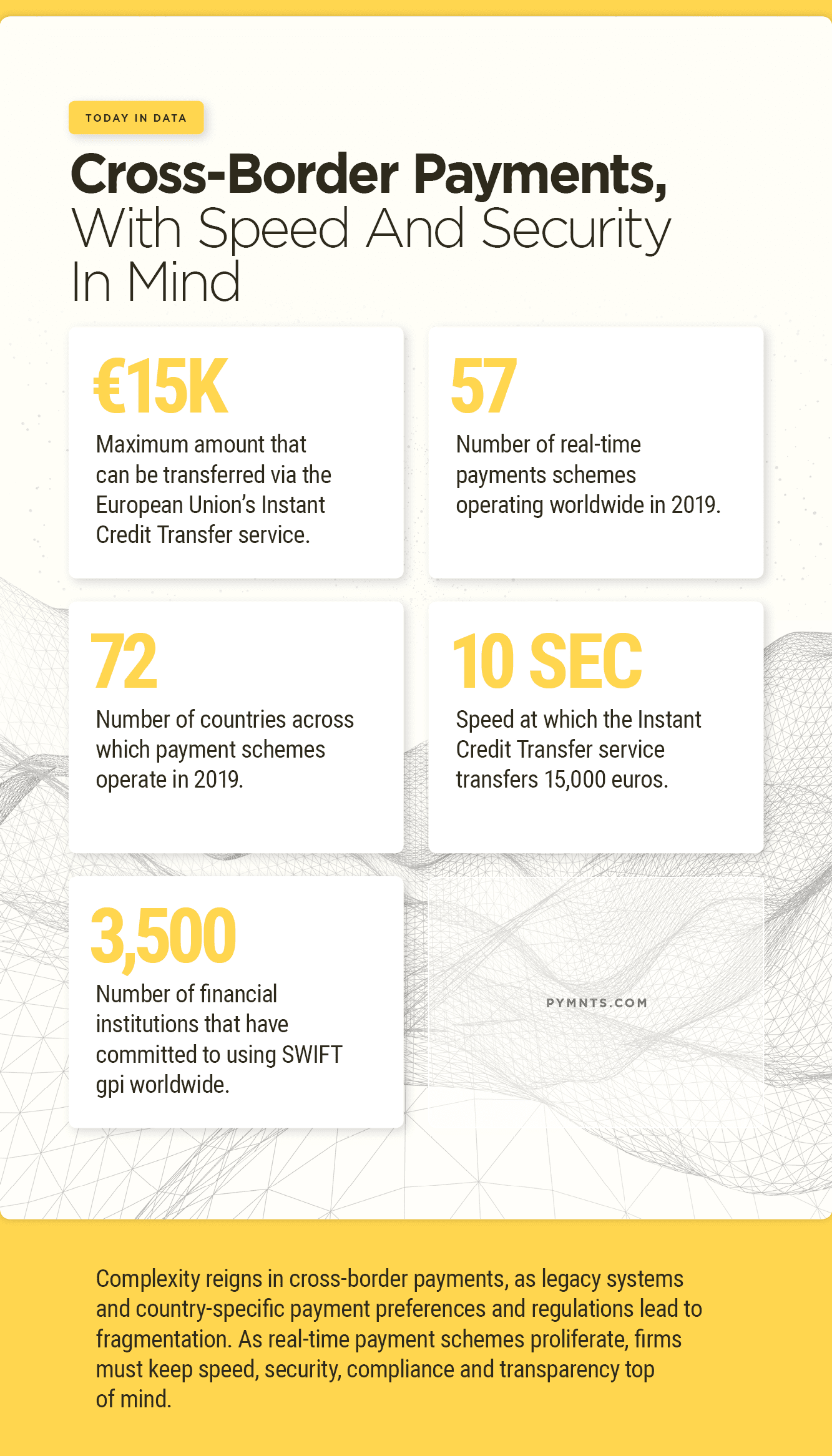

15,000 euros: Maximum amount that can be transferred via the European Union’s Instant Credit Transfer service.

57: Number of real-time payments schemes operating worldwide in 2019.

Advertisement: Scroll to Continue

72: Number of countries across which payment schemes operate in 2019.

10 seconds: Speed at which the Instant Credit Transfer service transfers 15,000 euros.

3,500: Number of financial institutions that have committed to using SWIFT gpi worldwide.