In the latest edition of New Reality Check: The Paycheck-to-Paycheck Report entitled “The Savings Deep Dive Edition,” PYMNTS Intelligence draws insights from a survey of more than 3,600 consumers to assess their capacity to maintain their savings in the current economic environment, particularly when confronted with significant expenses.

The study reveals that those who indulge in at least three out of the proposed 30 product and service categories tend to maintain savings balances that are, on average, 26% higher compared to those who abstain from such purchases. Specifically, indulgent consumers typically hold an average savings of $14,058, whereas non-indulgent consumers have an average of $11,178 in savings.

This pattern is notably prominent among baby boomers and seniors, where the 18% engaged in indulgent spending exhibit average savings 47% higher than their non-indulgent counterparts.

These splurging baby boomers and seniors, on average, hold savings of $21,014, while their non-splurging counterparts maintain an average savings balance of $14,320. However, among Gen Z consumers, nearly 40% describe their spending as indulgent for at least three product or service categories, even though their average savings mirror those of Gen Z consumers who abstain from such expenses.

Additionally, within the paycheck-to-paycheck demographic, only a quarter invest in “nice-to-have” items, with the indulgent spenders reporting slightly higher savings than those who refrain from such indulgence.

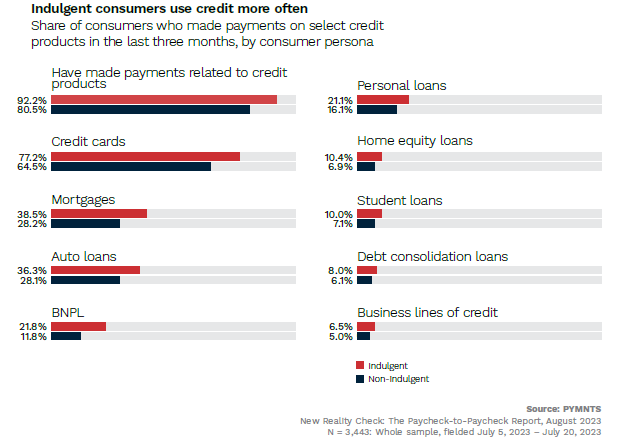

Shoppers who engage in indulgent spending also tend to be more active in making payments linked to credit cards, personal loans, and buy now, pay later (BNPL) schemes within the 30 days preceding the survey. “Overall credit product usage is 11 percentage points higher for consumers who cite indulgent spending in three or more categories than those who do not cite such spending,” the study shows.

Specifically, among these indulgent shoppers, credit card usage surges by 20% compared to those who do not engage in nonessential spending. Moreover, BNPL usage skyrockets to 85% higher, with 22% of indulgent consumers using BNPL services versus only 12% among non-indulgent consumers.

The disparity continues with personal loan usage, as 21% of indulgent shoppers resort to personal loans compared to just 16% among their non-indulgent counterparts. This higher utilization of credit among indulgent spenders strongly suggests that credit is more commonly employed for nonessential categories like clothing or travel rather than for essentials such as groceries or household supplies, per the study.