And while this news is worth celebrating, it’s worth remembering that there is still a significant portion of U.S. consumers who struggle to make ends meet — especially when faced with unexpected expenses.

As PYMNTS Intelligence discovered in researching “Unexpected Expenses and the Demand for External Financing Solutions,” 56% of U.S. consumers had to deal with at least one unexpected expense in the last 12 months, costing them on average $5,500 — a sum representing more than half of the average savings U.S. consumer have on hand.

The study, which is based on surveys with more than 2,500 consumers, found unforeseen medical bills are the most common unplanned expense, costing on average about $6,200. Unexpected home repairs, averaging $6,000, are the second-most common unanticipated bill.

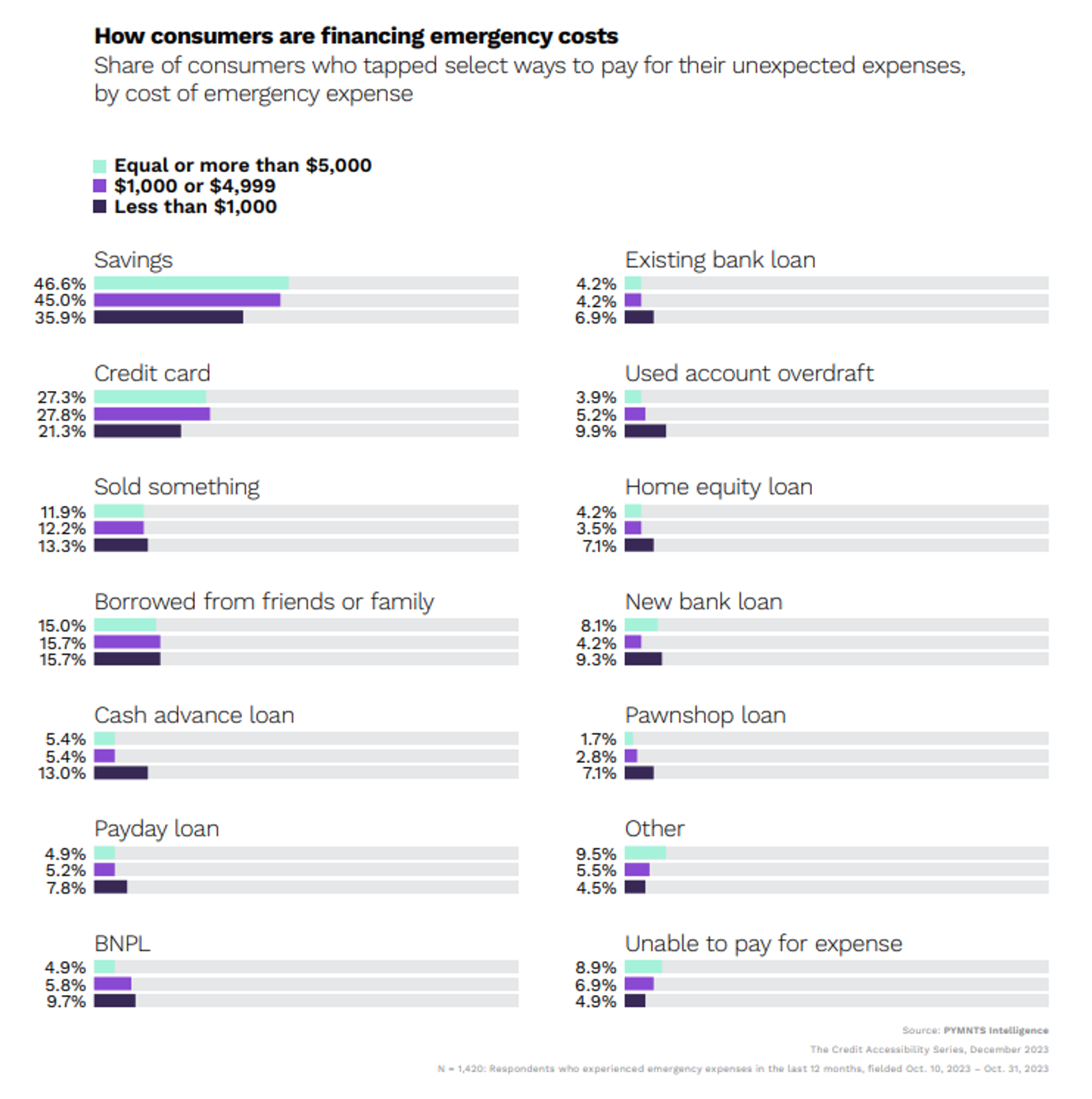

Faced with sudden costs like these, most consumers opt to dip into their savings accounts.

Nearly 47% of consumers use savings to cover bills costing $5,000 or more, while 27% turn to credit cards and 15% borrow from friends or family. When emergency expenses are south of $1,000, 36% rely on savings, while 21% reach for credit cards and 13% use cash advance loans.

Our study found that credit-marginalized consumers — those who have been rejected for at least one credit product in the past year — are 47% more likely than the average consumer to face unexpected expenses. And, because of their credit-challenged status, they are more than twice as likely to turn to high-interest credit products to cover emergency costs.

For instance, 18% of credit-marginalized consumers used cash advance loans, which is 2.2 times the rate of the average consumer. Fourteen percent of credit-marginalized consumers used payday loans, again 2.2 times the rate of the average consumer.

As the report concludes, although most consumers want to “save for a rainy day,” savings accounts are the first line of defense when unexpected expenses arise, which makes savings a challenge. For those who are credit-marginalized, the challenges remain far greater.