The daily juggling act of managing household expenses forcing consumers to think about credit.

Specifically, how and when they might take on more credit card debt to help ease the pain points of inflation, which remains stubbornly high, and which continues to eat into purchasing power.

In the report “New Reality Check: The Debt and Credit Deep Dive Edition,” a PYMNTS and LendingClub collaboration, we surveyed more than 4,160 consumers to get a sense of the tradeoffs between how they use credit and savings.

Roughly 60% of consumers live paycheck to paycheck, and most of us think that inflation’s pressures will remain in place well into next year. Drilling down a bit, there has been a bit more prudent management of debt. We found that seven in 10 consumers report taking a range of approaches to manage their credit card debt. Individuals and households are pulling back on spending and are using their cards less.

That means that there’s a bit more firepower, so to speak, at the ready to help bridge the gaps between what consumers want to buy and the available cash on hand (through their jobs or through savings) to be able to satisfy those desires.

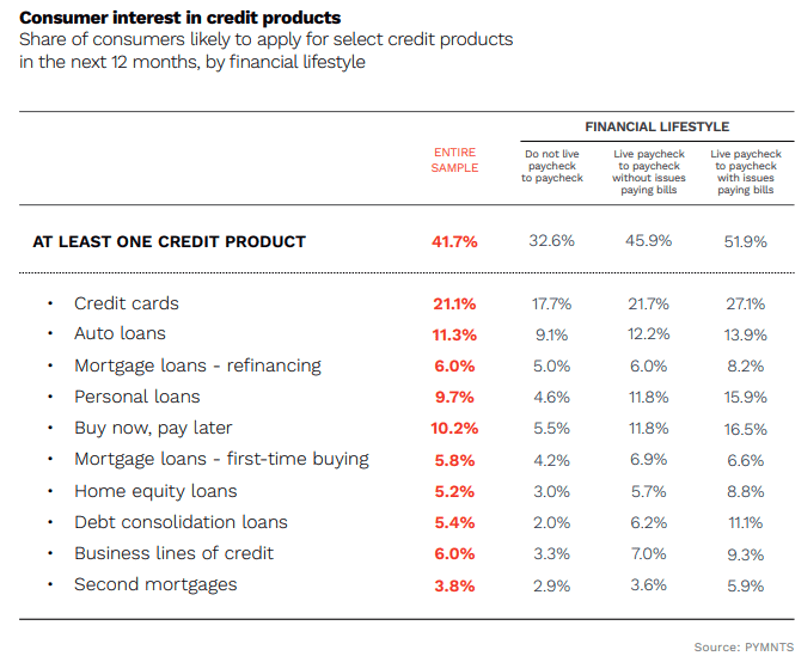

To that end, a full 42% of consumers said they would be likely to take on more credit products in the next year.

Credit card debt tops the list, at 21% of the entire sample. The population of people living paycheck to paycheck with issues paying bills top that tally, as 27% of this segment said they are likely to apply for a card in the next 12 months.

But there are some warning signs in the mix. Although the average consumer holds outstanding credit card balances equivalent to 35% of their available savings, those living paycheck to paycheck tend to have higher credit card debt relative to their savings level, PYMNTS and LendingClub found. Our data showed those with issues paying monthly bills carry balances of 157% of their available savings, meaning they would still have a balance even if they emptied their savings accounts.

There would be no easy fix, in other words, should these same consumers encounter a significant unforeseen expense.