Financial institutions (FIs) have had many reasons to consider the benefits of investing in receipt data solutions. These range from fighting friendly fraud to helping their merchant partners personalize their loyalty programs, potentially increasing sales. Another driver is FIs’ hope to increase customer engagement through hyper-personalized offerings assisting consumers with spending behavior insights. Correctly implemented, receipt data can piece together separately purchased items that could fall under different categories, such as healthcare and food bought during a single grocery trip, and offer a granular look that helps FIs make more accurate spending recommendations.

Receipt data’s potential is a bit of a self-fulfilling prophecy, however, as found in proprietary research prepared for PYMNTS’ March collaboration with Banyan, “Meeting the Need for Item-Level Receipt Data.” The FIs most ready to implement receipt data tools into their consumer-facing offerings are also the most likely to fully recognize its potential. The report found that nearly 40% of surveyed FIs expect receipt data to improve customer experiences and engagement. And the perceived impact is meaningful: a nearly equal share believes not implementing receipt data tools could lead customers to other FIs that do.

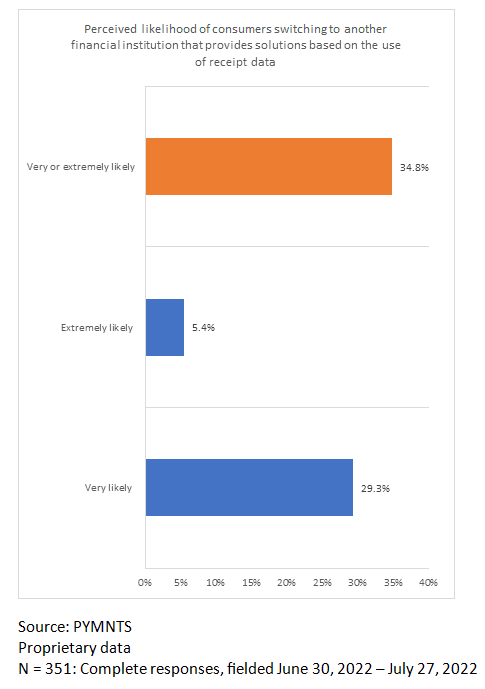

However, that number grows for FIs specifically seeking to track consumer spending to give their customers a better understanding of their spending behavior, with 59% of firms expecting the tool to provide an improved customer experience. Previous PYMNTS’ research finds that this expectation rises to nearly 80% among firms with high data readiness. Of those organizations, 77% believe consumers would be very or extremely likely to switch to institutions that provide solutions that use receipt data.

Self-fulfilling prophecies aside, firms believing customers may seek out providers offering receipt data spending tools may be on to something. A previous PYMNTS report found that just over 40% of customers want personalized advice and money management support from their mobile banking apps, with 29% of FI customers saying the same. Approximately the same share of consumers want suggestions on how much they could save every month. Receipt data can serve as the key to unlocking those critical insights — and winning the favor of long-term account holders.

For FIs, receipt data can empower a multitude of innovative solutions. Those considering implementing the tool for consumer-facing spending recommendations may well find that the customer satisfaction benefits they forecast will come to fruition.

See More In:

banking, Banyan, Connected Economy, consumer finance, Consumer Spending, Digital Banking, ecommerce, Featured News, News, PYMNTS Study, receipt data, Retail, Retail sales