A key for financial institutions (FIs) prioritizing loyalty and seeking to tailor their clients’ customer experience could be right in front of them: receipt data.

Today’s digitally savvy consumers expect seamless, personalized banking — including targeted help with their spending habits. However, customers may not want to pay extra for what could be perceived as an “extra” feature, perhaps due to inflation’s impact on their wallets. Some FIs seeking to strike that delicate balance have embraced item-level receipt data as one solution.

The study “Tapping Into the Benefits of Item-Level Receipt Data,” a PYMNTS and Bayan collaboration, found that 95% of FIs and FinTech firms surveyed already use receipt data to at least partially support their operations. Given this, the concept of receipt data is likely not new to FIs, removing a barrier from the process of those seeking to hyper-personalize the customer experience and foster loyalty.

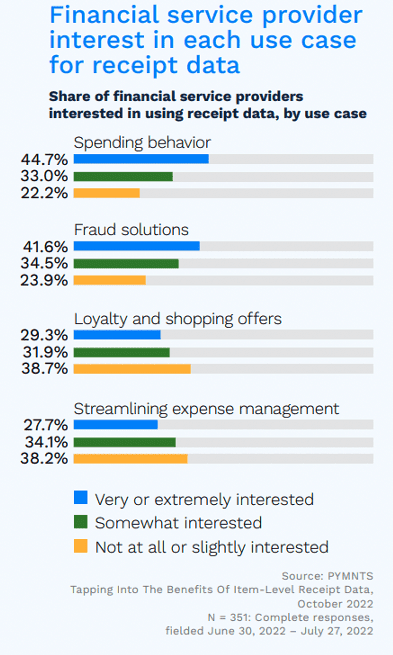

Financial service providers already express interest in using receipt data to personalize the customer experience by educating consumers about their financial habits.

This education could serve as an important approach toward customer loyalty, as only 4% of Americans demonstrate basic financial literacy. Presumably, a fair portion of the remaining 96% might want to learn more, especially relating to their personal finance.

Perhaps unsurprisingly, firms that are very ready to use data (“high data-readiness firms”) are most interested in using receipt data to boost consumers’ understanding of their spending behavior. The firms considered this to be high stakes, as 67% of these firms surveyed said they believe consumers would be very or extremely likely to switch institutions for ones providing solutions using receipt data. For firms that were very or extremely interested in using the data for loyalty or shopping offers, this belief that switching could be imminent surged to 78%.

Implementation issues were cited as the largest obstacle in using receipt data to power consumer education. More than 45% of firms named system readiness, a lack of standardization and cost as their primary challenges. However, implementation may not be as harrowing as it initially seemed. Third-party platforms can assist FIs in making this change as painless as possible.

Banyan is one of these third-party providers. In an interview with PYMNTS’ Karen Webster, Chief Marketing Officer Andrea Gilman explained why some FIs see the long-term value in making the change.

“These firms are not just investing for the pure ‘joy’ of innovation, but really to drive superior experiences and financial services and to get people to switch,” she said. “… As we build this network, we are creating the infrastructure for the banks and the FinTechs to build on top of — and to focus their time on creating their customers’ experiences.”

For FIs seeking to retain their customer base and build long-term loyalty through such educational programs and personalized features, item-level receipt data may be one of the strongest gadgets in their toolbox.