Consumers are fed up and they’re not going to take it anymore. At least when it comes to their credit scores. A new survey says that U.S. consumers are tired of seeing their creditworthiness, or lack thereof, determined by outdated methods. Is the industry prepared to respond?

VantageScore’s latest Consumer Survey has one big takeaway: Consumers are ready to see a significant shift in the credit score marketplace.

In fact, the majority of those surveyed – 50 percent – voiced their support for newer methods of calculating credit scores and fostering competition among credit score model developers.

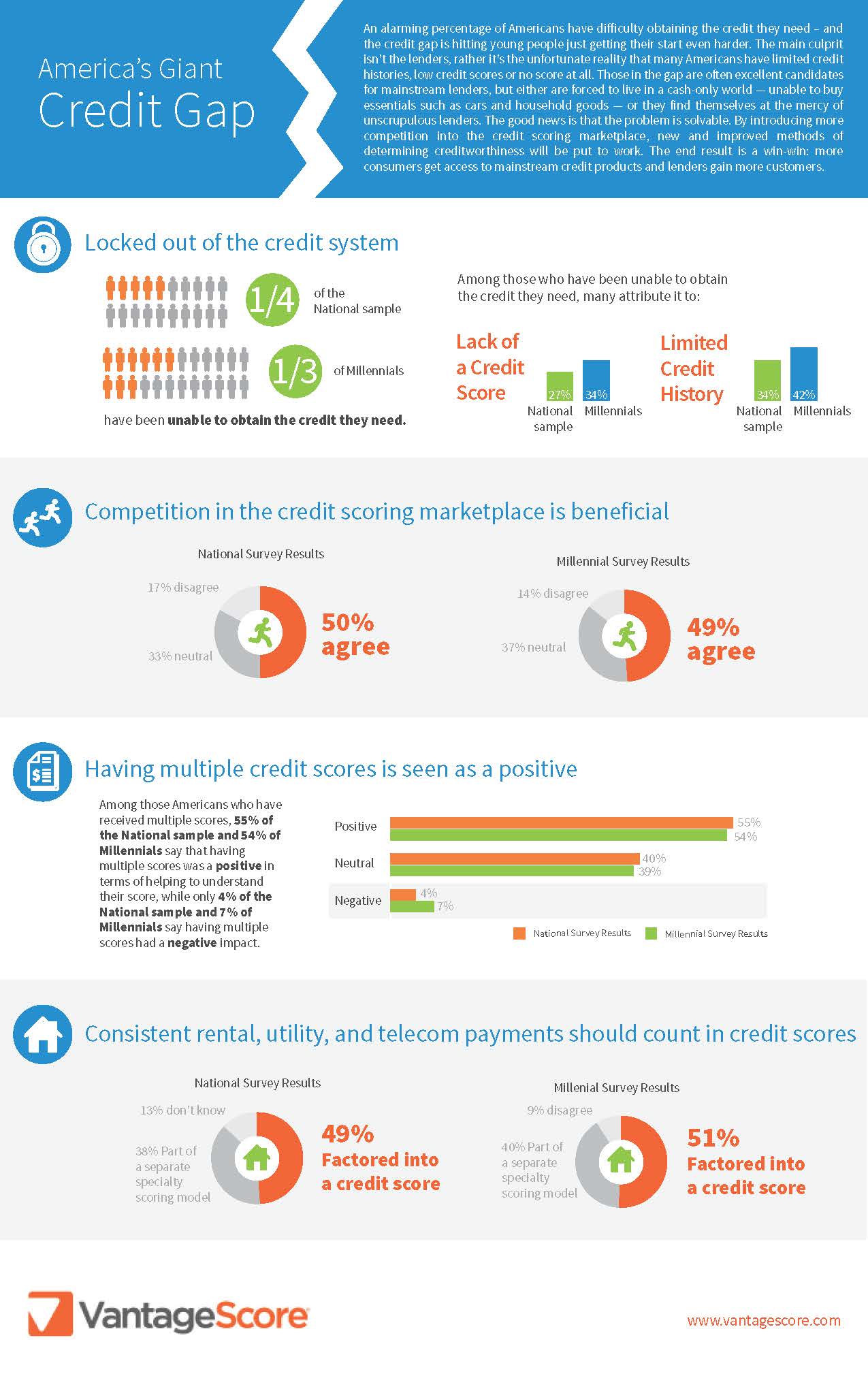

While consumers expressed approval of various features within more modernized credit scoring models, such as recognition of positive payment histories for rent, utility and telecomm bills, the survey found an underlying dissatisfaction with the number of people who remain locked out of the credit system. The survey polled two groups: a millennial sample, made up of 200 individuals between the ages of 18-34, and a national sample, consisting of 1,000 American adults over the age of 18.

According to the survey results, nearly 48 percent of millennial respondents were unable to receive the credit they needed due to the lack of a credit score, and 42 percent of them attributed it to a limited credit history.

When looking at the national sample, about 27 percent felt not having a credit score stood in the way of obtaining credit, whereas 34 percent said it was due to limited credit history.

The alarming percentages point to a glaring credit gap that is hitting young people hard as they begin to step into the financial world, VantageScore explained, noting that the lack of substantial credit history or having low or nonexistent credit scores are the main drivers of this growing gap.

Many of those consumers whose creditworthiness is not up to par with what the industry currently deems acceptable are subsequently forced to navigate a digital world with a cash-only approach, making it difficult to purchase essentials like vehicles and homes, or even to shop online. Subsequently, these consumers also can find themselves at the mercy of unscrupulous lenders.

“These consumers are reachable, scoreable and can be made eligible for automated underwriting systems in a safe and sound manner. They are seeking credit products and credit cards in particular,” Barrett Burns, president and CEO of VantageScore Solutions, said in a press release announcing the survey Consumer Survey results.

“Many are very attractive potential borrowers, and lenders using outdated credit scoring models are missing opportunities to win their business and their loyalty.”

But there is a viable solution to the problem and it’s one that many of the survey respondents are already in agreement with.

The introduction of increased competition within the credit scoring marketplace has the potential to give more viable consumers access to mainstream credit products while helping lenders increase the numbers of customers they are able to reach.

Increased competition can also open the door to new and value-added methods of credit scoring, which may help to bring more accuracy and fairness to the determination of creditworthiness.

Fifty percent of the national survey respondents agree that increasing competition in the credit scoring marketplace is beneficial, with the millennial respondents following close behind with 49 percent in agreement.

One of the new approaches to credit scoring includes ensuring that rental payments are factored into credit scores, which many of the national population respondents (49 percent) and a slight majority of millennials (51 percent) support.

The consumers surveyed by VantageScore also maintained a positive view toward having multiple credit scores from different models as it helped them to better understand their credit score, while only 4 percent of the national sample and 7 percent of millennials expressed multiple scores as having a negative impact.

“The results of this survey clearly demonstrate that consumers prefer competition in the credit scoring marketplace, and that they welcome important innovations VantageScore has delivered to a market that previously lacked the motivation to better serve lenders and consumers,” Burns said.

Survey results can be found here or in the infographic below.