This warning was delivered last week by Rohit Chopra, director of the Consumer Financial Protection Bureau (CFPB), who reiterated his support of open banking during an industry presentation and assured attendees that its guidelines will be deployed evenly across the industry.

“We know dangers exist when more powerful players weaponize industry standards,” Chopra said. “We have to be vigilant that standard-setting does not skew to benefit dominant firms and their prevailing market power.”

Open banking is the legal framework permitting secure data sharing amongst financial institutions (FIs) and FinTechs to enhance the products and services they offer consumers. The CFPB is currently finalizing its guidelines around the framework.

Despite his concerns, Chopra believes open banking, once finalized, will streamline the processes consumers now encounter when trying to switch FIs or financial products — processes that he called “clunky.”

“Open banking involves less red tape and more seamless switching,” he said.

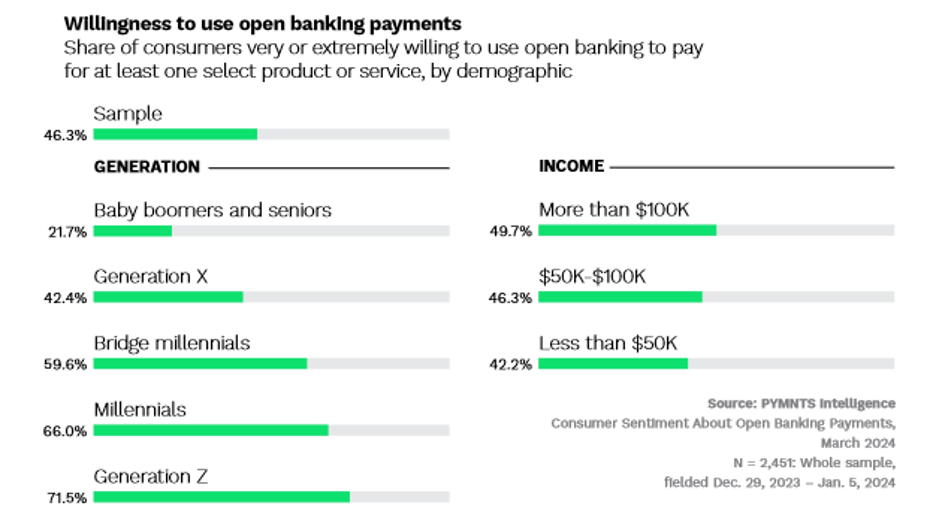

As PYMNTS Intelligence recently found, if open banking means faster payments, then a significant portion of Americans — especially younger ones — support the switch.

“Consumer Sentiment About Open Banking Payments,” a new PYMNTS Intelligence report created in collaboration with Trustly, found nearly half of the 2,541 U.S. consumers surveyed are willing to use open-banking supported payments.

This willingness surges for younger respondents. The majority of Generation Z and millennial consumers surveyed said they would be highly willing to try open banking payments for at least one type of common transaction, such as recurring bills, subscriptions and groceries.

But the support escalates even more for those already familiar with open banking. Sixty-eight percent of respondents who already used an open-banking application to pay for at least one item in the last year told us they were generally satisfied. The satisfaction level increased to 82% among high-frequency users.

However, the report reveals a clear divide between younger respondents who expressed enthusiasm for open banking initiatives and older ones who were less avid.

Seventy-two percent of Gen Z and 66% of millennials showed a strong willingness to use open banking payments, while only 42% Generation X respondents and 22% of baby boomers and seniors are onboard.

Meanwhile, 50% of respondents earning at least $100,000 per year — high-income earners — are highly willing to use open banking payments. Only 42% of those earning $50,000 or less annually said the same.

The reluctance older consumers harbor about open banking hinges on security concerns. Sixty-four percent of baby boomers and seniors who are not open-banking users said worries about security and trust was the leading reason for their hesitancy. Only 44% of their Gen Z and millennial counterparts share those concerns.

To mitigate trust and security anxiety, especially among older consumers, “Consumer Sentiment About Open Banking Payments” suggests FIs and FinTechs both make transparent communication about security measures and user benefits a priority. Doing so will bolster credibility and acceptance across all age groups.

The report also noted that FIs and FinTechs can leverage the eagerness younger consumers already show for open banking payments. The best way to do this? Highlight both the ease of use and the security and innovation open banking payments can offer. Doing so can help FIs and FinTechs improve adoption rates among Gen Z and millennial users.