Shakespeare once wrote that the “readiness is all.” That pithy statement can apply to any number of endeavors – including the shift to electronic payments on a global scale.

The advantages of electronic payments are hard to dispute. It’s safe and less costly than cash – for both merchants and consumers. Millions of low income families can get access to the banking system – there are 2 billion individuals around the globe without access to a bank account. Mobile devices offer access to those funds anywhere a consumer and her mobile phone can go.

Yet a staggering $21 Trillion of spend still happens in cash – even where there are options for making payments using digital methods.

Why?

The issues stymieing global adoption are formidable ones, indicating that Shakespeare’s “readiness” entails satisfying a number of demands (some of them competing ones) that must be addressed in order to bring streamlined payments to the masses.

Visa’s new white paper entitled “Perspectives on Accelerating Global Payments Acceptance,” delves into the challenges surrounding the eventual diminishment of cash as a method of payment in favor of more technologically advanced methods. And lays out a framework, without being perspective, for how the industry at large must begin to think about addressing this societal challenge.

Visa identified three barriers to the global acceptance of electronic payments:

- Infrastructure:

The sheer lack of physical infrastructure that makes terminalization and the delivery of services like risk management and underwriting impossible or too costly or both. Mobile devices, however, provide an opportunity for players to “leapfrog” the old ways of doing business into new mobile-driven ways.

- Incentives:

Inadequate ROI as a result of low volumes, and/or a perceived cost of acceptance. In developing economies, where cash is predominant, merchants may also resist because they don’t want to create a (taxable) electronic record of transactions, and the nature of the transaction – low dollar amounts – make profits challenging.

- Policy and Regulation

Restrictive, outdated or inconsistent regulation makes the cost of doing business in certain markets a challenge and the value proposition for the merchant less attractive. The inconsistent nature of regulation on a worldwide basis introduces friction that is costly to the ecosystem overall as players are forced to adjust their business models on a country by country basis.

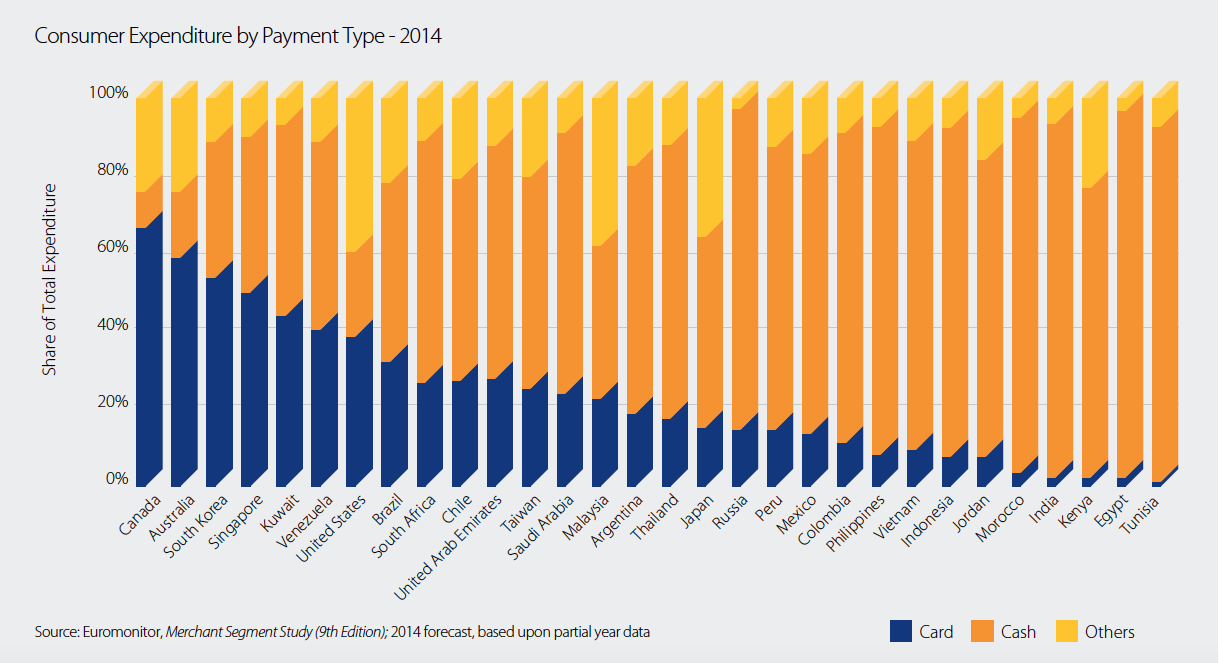

While some countries are on their way toward becoming “cashless” – chiefly among the most industrialized of nations – other nations are sorely lacking. Visa found that the countries that have made the most headway in transitioning to a model that has relatively less reliance on cash sports a roster that includes Canada, Australia and South Korea, where cash is less than half the percentage of overall consumer expenditure.

While some countries are on their way toward becoming “cashless” – chiefly among the most industrialized of nations – other nations are sorely lacking. Visa found that the countries that have made the most headway in transitioning to a model that has relatively less reliance on cash sports a roster that includes Canada, Australia and South Korea, where cash is less than half the percentage of overall consumer expenditure.

Visa’s report finds that infrastructure is one of the most critical parts of delivering electronic payments and also remains woefully lacking. At present about 43 percent of all consumer payments are made with cash and only a fraction of retailers around the globe are outfitted with the POS terminals and the telecom services needed to support such devices or electronic payments in the first place.

At the government level, the barriers to efficient adoption can come in the form of regulation of acquirer pricing that limits the attraction of bringing electronic payments to the fore, and are at times conflicting policies that do not balance tackling the shadow economy that marks some emerging nations with “consumer friendly” policies that indeed promote spending (and by extension, electronic payments).

What to do? Visa’s report posits that at the government level, there could be subsidies for POS terminals, a tactic that might be thought of as merchant incentive programs that operate well in cash-centric societies. Or alternatively, governments can lead by example and adopt electronic payments themselves, with the acceptance of such payments for a range of services.

In an interview with MPD’s Karen Webster, Sameer Govil, Visa’s SVP for Policy and the report’s author, cautioned that Visa’s findings and suggestions are not in fact meant to be prescriptive (beyond possibilities) to any countries or companies, and are in fact meant to be “brand agnostic,” with respect to even his own company or competitors. It’s important to avoid too much prescriptive dialogue, said Govil, because each challenge and solution needs to be “discussed in a local market context… [electronic payments] is a complicated topic” and Visa’s aim is to simplify the discussion (moving it away from technology) to focus on governmental and regulatory initiatives.

“The underlying opportunity is there,” said Govil, with the key a part of looking at “each stage of adoption in electronic payments” in each market, with an eye on “different sets of regulatory and policy choices…the objective is to be different for Sri Lanka, or Colombia … the ideas of how to fast track electronic payments in each market is not the same.”

“The underlying opportunity is there,” said Govil, with the key a part of looking at “each stage of adoption in electronic payments” in each market, with an eye on “different sets of regulatory and policy choices…the objective is to be different for Sri Lanka, or Colombia … the ideas of how to fast track electronic payments in each market is not the same.”

When asked about how central banks and other large regulators can help, Govil replied that such entities “can serve as role models to grow financial inclusion, and they can start seeing themselves that way, and the influence that they have on [payment] ecosystems.”

As for a consumer push, digital commerce, according to Govil, allows for an elimination of the lag time between purchase and payment, which behooves merchants and which both guarantees payments to the merchants while safeguarding consumer interests. Other avenues, the report noted, could include “disincentives” for cash usage, which could include a tax on cash payments.

Govil also cautions that the movement to adopt an electronic payments strategy is a long term one and one with global reach. But strategy must also be local in nature, tailored to economies on a case-by-case basis.

Though one might look most readily at country by country trends toward cashless adoption, it is in fact a local market mindset that can help foster change most significantly. Govil told Webster that regulators also need to understand payments “in a local context” that includes not just consumer behavior but concerns about data security, too. Regulators, he added, “need to work with partners like us, and other interested parties, in that local market context.”

In the end, the slow pace of electronic payments adoption can be traced to a series of challenges – ranging from merchant acceptance to consumer incentive, and new infrastructure to support those behavioral changes — which require enormous effort. But then again, the rewards can and will be enormous, too. Beyond the program and policy changes that need to be considered and ultimately implemented, collaboration among stakeholders can bring a virtuous cycle to financial inclusion and electronic payments.

To download the Visa white paper, click below.