Why The Next Big Connected Commerce Play Is Television

No doubt you’ve heard the news: People aren’t watching television anymore.

That may leave many of you who left for the office this morning having watched a half hour or so of morning network or cable programming — who probably spent some part of your weekend parked in front of the television watching sports, “Saturday Night Live” or “The History Channel” — wondering if you’re an outlier, or just too old and set in your ways to change your habits.

But then again, maybe you think it’s not you; it’s those crazy, cord-cutting, mobile-centric, social network-tethered 18 to 24-year-olds who’ve given television the boot.

That might not be a crazy assumption: Reports from Nielsen reveal that television viewership by that demographic has declined more than 40 percent since 2010 and is off 11 percent year over year for the older half of millennials aged 25 to 34.

But why then, you might ask, are so many pure-play eTailers, whose target audience is the millennial — like The RealReal and Rent The Runway, new marketplaces like OfferUp, deal aggregators like Groupon, alt lenders like SoFi and alt lending platforms like LendingTree — buying pricey blocks of airtime on CNN and CNBC to promote their brands?

And why do card networks and banks continue to hire actors and spokespeople to blanket the airways with clever ads that tout the merits of using their products?

Because President Donald Trump isn’t the only one who spends four — and sometimes as many as eight — hours a day watching television.

The Great Television Viewing Fallacy

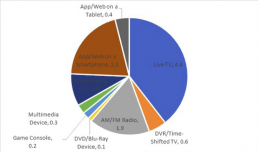

According to 2016 Nielsen data, consumers in the U.S. spend 4.4 hours a day watching television and 1.9 hours listening to AM/FM radio.

From “The Economics of Attention Markets” by David S. Evans

Yes, you’re reading this chart correctly. Of the 11.1 hours people spend each day consuming media, about twice the amount of time people spend with their thumbs on their mobile devices and inside apps is actually spent watching television.

But that’s not even the best part.

In a new study of ad-supported media and the attention economy written by economist and author (and PYMNTS chairman) Dr. David S. Evans, 4.4 hours is just how much time consumers actively engage with television programming.

In other words, sitting right in front of their TVs, watching them.

If one were to include the time a television is on “in the background” — while those same consumers are cooking, putting groceries away, cleaning, getting dressed, getting kids off to school, answering emails — the number of hours spent nearly doubles.

And, that, says Evans, adds up to a lot of time.

Based on his estimates, consumers spend 174 billion hours actively watching television — in other words, it’s the main thing they’re doing — and 311 billion hours when they also include time spent passively engaged with this medium — in other words, when people have the boob tube on while they are mainly doing other things, like feeding the kids.

That’s 174 billion out of the 437 billion and 311 billion out of the 779 billion total hours that people either spend engaged actively, or actively and passively engaged with all forms of ad-supported media.

At 311 billion hours, that means consumers spend more time actively and/or passively engaged with television than the 308 billion hours Evans reports they spend at work.

So, although it’s true that younger millennials watch less television than they used to, they’re still actively watching two hours and seven minutes of it a day, according to Nielsen. Their older millennial buddies are actively watching about three hours, and big brother and sister Gen Xers are up to about four and a quarter hours a day. Their baby boomer parents and grandparents watch just about as much, if not a little more, than they always have — six and seven-plus hours a day, respectively.

That’s why, according to eMarketer, television still accounts for more than a third of all ad spend ($72 billion of $206 billion for 2017) in the U.S. and why eTailers interested in building a brand continue to use television as an important part of their advertising mix.

And why, with every TV rapidly transforming into a smart TV that has a connection to the internet, television is positioned to become one of the most powerful connected commerce platforms in the U.S. — and in other developed economies where people spend more than half of their leisure time watching TV.

Television as a Contextual Commerce Platform — the 1960s Version

It all began with the Veg-O-Matic.

In the 1960s.

Popeil set up shop in New York in 1937 and then later in Chicago in 1941, where he invented a slew of household gadgets — like potato peelers and cheese slicers. Selling those gadgets was done by sending salesmen into stores to set up tables to demonstrate and then sell those products. His salesmen also sold door-to-door to housewives with an interest in saving time when preparing meals.

Two of Popeil’s more popular inventions, the Chop-O-Matic and the Veg-O-Matic, created a big problem for his team of traveling salesmen. They found it hard to carry an adequate supply of vegetables for the number of demonstrations they had scheduled each day, which meant the product was not able to be demonstrated properly and consistently.

That gave Popeil the idea to record a video of the product in action, so that in-home demonstrations featured Popeil’s persuasive sales and demonstration techniques by way of video instead of live, in-home demonstrations by his sales team.

All the while, salesmen continued to make sales, which gave Popeil another idea.

If people still bought his products after seeing a video of the product, why not take that demonstration video and broadcast it to a much larger, in-home audience — using the most popular digital medium of its day: the television.

Popeil started buying remnant ads that would run at odd hours at $7.50 a minute in the early 1960s. Each demonstration ended with a call to action — with the infamous “operators standing by” to take orders for what consumers just saw over the course of 30 seconds and had to buy.

And buy they did.

At $3.98, the Chop-O-Matic sold more than 2 million units in its first year. The Pocket Fisherman, a collapsible fishing rod priced at $19.99 when introduced in 1973 by Popeil, sold 2 million units in its first year too.

The debut of the Pocket Fisherman also ushered in another new concept — installment payments. The $19.99 purchase price was offered to consumers to be paid in three easy installments.

Popeil and the company set up by his son Ron, Ronco, were the pioneers of direct response television and gave the remnant television ad space a new lease on life. Their “O-Matic” product line was soon followed by many other gadgets — the Egg Scrambler, Food Dehydrator, Smart Rotisserie, women’s stockings that never got a run, smokeless ashtrays and even spray hair in a can — an invention created by Ron to cover his bald spot.

Popeil and Ronco paved the way for many others, who saw an opportunity to pitch products directly to the consumer using the power of television.

Chia Pets, those famous sets of Ginsu Knives, Suzanne Somer’s ThighMaster, the Clapper, the Total Gym, George Foreman’s Grill and the must-have Snuggie are all some of the more infamous examples of products sold in this manner.

Before you laugh, the direct response infomercial market is a $250 billion commerce market — and growing.

Five hundred million Chia Pets are sold each holiday season (at $19.95 each, the Trump version is the latest in its Presidential series), the ThighMaster raked in $100 million for Suzanne Somers, the Total Gym a cool billion for Christie Brinkley and Chuck Norris and, in 2015, Snuggies were a $500 million business.

Some 44 years later, the Pocket Fisherman is alive and selling well. A vintage Pocket Fisherman can be purchased on eBay for $0.99, and a new and improved version is listed on Amazon.com for $24.99. Currently, it’s out of stock at Walmart, where it can be bought for $18.88 when they get some more.

This year, my personal favorite is the Sock Slider — a plastic contraption that makes it a cinch to put on socks and then collapses into a shoehorn to make it a cinch to put on shoes. There’s still time to order if you’re looking for that all-important stocking stuffer. Who doesn’t know someone who needs a Sock Slider for Christmas?

Even if you don’t, the commercial is worth watching:

Payments today are complemented by credit cards, mobile wallets and even Amazon Pay.

Television as Contextual Commerce — the 1980s Edition

My late grandmother lived in Florida and developed an obsession for buying what my mother called “knick-knacks” in the late 1980s and 1990s. It was then that Grandma began to amass the largest collection of Capodimonte we’d ever seen. The little porcelain swans and vases, flower bouquets and figurines were everywhere in her home. Capodimonte soon became her favorite presents to give and, quite frankly, our least favorite presents to receive.

Grandma, we’d ask, where are you buying such, um, interesting stuff?

Home Shopping, she would say, at which point she’d direct us to the television to see what the hosts were pitching at that moment.

For my grandmother, and others like her, shopping via television was both a novelty, something to occupy her time, and a way to feel a sense of community with the hosts and the other shoppers who’d call in and talk about their shopping experiences.

I also happen to believe my grandmother liked the visits from the UPS man who delivered her treasures as much as she liked watching the show and buying things.

Taking the 30-second infomercial of the 1960s and turning it into a live, interactive sales pitch, where on-air hosts sold products, was the brainchild of radio station owner Bud Paxson in 1982.

It was all inspired by a can opener.

In 1977, one of Paxson’s advertisers ran into financial problems. Instead of paying his balance in cash, that advertiser paid Paxson in can openers. Turning those can openers into cash was left to one of Paxson’s on-air personalities, who took to the radio airwaves and sold the entire inventory of can openers for $9.95 each.

If can openers could sell on the radio for almost $10, sight unseen, why couldn’t lots of other stuff that people could see and interact with in real time sell on television?

That silver-tongued, on-air personality who moved countless can openers became the first Home Shopping host in 1982, selling 75,000 products in over 20,000 hours of live programming. The Home Shopping Network (HSN) went national in 1985, and its competitor, QVC, went live a year later.

Like Ronco and Popeil, over the years HSN and QVC went multi-channel and used the internet to complement their televised pitches. In 2017, QVC bought HSN for $2.1 billion dollars so they could consolidate their largely independent cadre of loyal patrons. According to company filings, in Q1 2017, HSN reported that its 5 million shoppers purchased 13 times each year and that 90 percent of their sales came from repeat customers. QVC’s 8 million customers shop 25 times each year and account for 92 percent of their sales. Those repeat shopper rates are more than double what Internet Retailer (IR) reports as the shopper repeat rate for the IR Top 500 (39.2 percent).

Today, QVC and HSN, combined with their 69.4 million visits, represent the seventh most-trafficked online retailer, ahead of Macy’s.

Television’s Smart, Connected Future

There have been a few attempts over the years to take the notion of direct response television to the next level.

Seventeen years ago, when the commercial internet was just a toddler, innovators thought that the intersection of the internet and television viewership would happen, quite literally, on the TV screen itself. A feed running on the side of a television show required the use of remote controls to “shop” the products promoted in those feeds — a clunky experience that never got much, if any, commercial traction.

In 2010, Bluefly launched QR codes, as did HSN in 2011, so that viewers could use their phones to link to product pages for purchases. Both efforts were shuttered not long after they started, owing to the clunky technology that created a bad user experience, along with tedious integrations required of the brands.

Since then, the direct-to-consumer concept has evolved very little beyond its early days of campy infomercials and continuous live programming with operators standing by.

The infomercials have become more sophisticated — and longer — with some now using a full 30-minute segment, complete with celebrity endorsements and hosts. The Home Shopping product selection has expanded and diversified to include celebrity products like Mariah Carey’s jewelry, Sheryl Crow’s clothing and Beyonce’s hair stylist’s hair care line, to name but a few.

Consumers today who want to buy the things they see on television — the products the stars in their shows are wearing or using or the products they see in the ads they are watching — do so via the mobile devices that are with them as they watch TV; they can google and search for them on Amazon while the show continues.

That has the potential to change, and rather dramatically: As more televisions connect to the internet, the mobile apps users like to access are now available to them on the big screen.

Nielsen reports that going into the 2017 television season, of the 125 million households in the U.S., 118.4 million of them had at least one television in their household. That’s up 1.6 percent from the prior year. At the end of 2016, roughly 36 percent — or more than 42 million of those households — owned a television that was connected to the internet. Analysts report that 59 percent of all televisions sold in the first half of Q1 2017 were smart televisions, up from 50 percent the year prior.

At the same time, Netflix reported in June of this year that it had more than 50 million subscribers — more than cable television. Amazon’s streaming service is available to all 80-plus million of its Prime Members here in the U.S. And Hulu is a distant third, with 12 million subscribers.

It’s possible to watch Netflix and Amazon Prime and Hulu on these smart TVs, and some 42 million households have the ability to do so today.

And, of course, that’s what many people do. Those who don’t are watching programming on lots of other devices, like game consoles, PCs and tablets, that are now being substituted for big screen TVs.

But — and here’s the key thing — these new streaming players are doing this over the internet, which connects them and those viewers directly. Unlike operators standing by and 1-800 numbers, they have the internet and their apps.

And they are doing this globally.

That’s a lot different than the cable companies, satellite providers and (this still happens) over-the-air broadcasters who don’t have a direct internet connection with the consumer for the programming they are pushing out. And who tend to operate in national, and often regional, footprints.

Right now, the streaming players — particularly Netflix and Amazon — are all about paid subscriptions with no ads.

I don’t think that’s a long-term situation, however.

Like any digital pure-play that enters an analogue world, Netflix and Amazon both understand the importance of commerce in their digital worlds. Both have the payments credentials for their users on file, available for them to make purchases for the products they see and may want to buy in the context of the programming their customers are watching.

On their big, smart television screens.

Or any other device that happens to be streaming entertainment from these providers.

Either of these companies, or a new one in this fast-growing area, could introduce an ad-supported — or commerce-supported — model that either subsidizes the cost of providing programming or provides an additional revenue stream if they do.

In fact, given its growing commerce empire, this seems like a more interesting thing for Amazon to be doing than just competing with Netflix for streaming eyeballs.

Today, roughly 18 percent of all television viewership happens online. But like most other shifts, there’s momentum, and it’s growing. The long run could be a world in which television is provided via streaming over the internet, but with a much richer commerce layer than the uninspired one cable and satellite providers have been able to serve up.

It’s a massive revenue and commerce opportunity for a medium that sucks up more time than people spend at work.