Companies like Netflix and Blue Apron seem to grab the headlines, but while those brands are household names, streaming services and meal kits aren’t the biggest money-makers. So, which are?

This edition of the Subscription Commerce Conversion Index gauges subscribers’ experiences in accessing consumer retail products through subscription services and determines which categories are more successful in customer satisfaction.

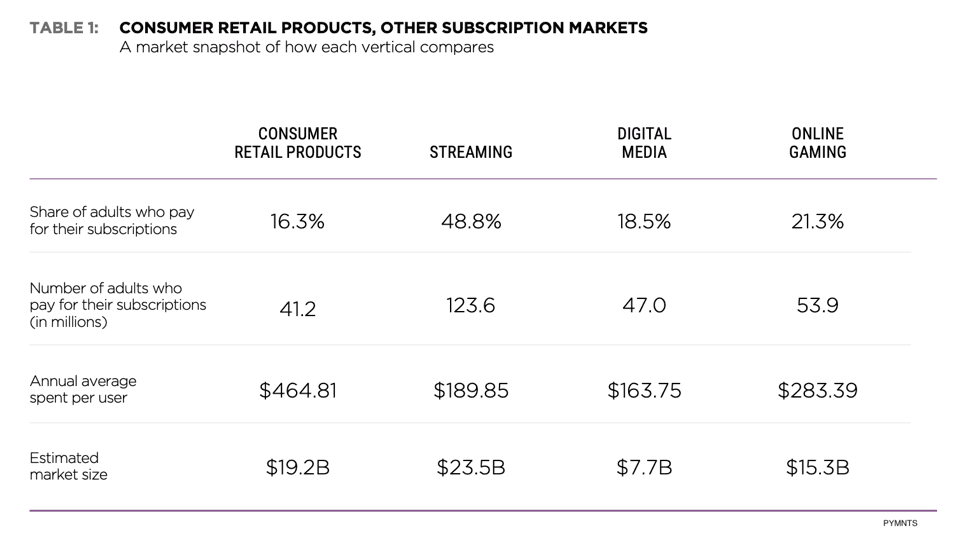

Retail Subscriptions Rank High in Spending

Even though the consumer retail product market has fewer subscribers than digital media, online gaming or streaming services, it is driven by a higher annual rate of spending. Some 41.2 million consumers subscribe to consumer retail products, whereas streaming has three times the number of subscribers at 123.6 million.

The average U.S. subscriber spends $464.81 annually on retail subscriptions to purchase beauty products, clothes and fragrances, among other items. This represents 64 percent more than the $283.39 spent on online gaming subscriptions, the second most popular category in annual spending.

Who Are the Subscribers?

Streaming and online gaming subscribers run younger than consumer retail products subscribers. The largest group (46.6 percent) of online gaming subscribers fall into the Gen Z demographic, followed by millennials (39.0 percent) and bridge millennials (37.6 percent). Streaming subscribers are concentrated among millennials (82.9 percent) and bridge millennials (82.4 percent), while Gen X (73.4 percent) and Gen Z (72.7 percent) have nearly equal levels of participation in streaming subscriptions.

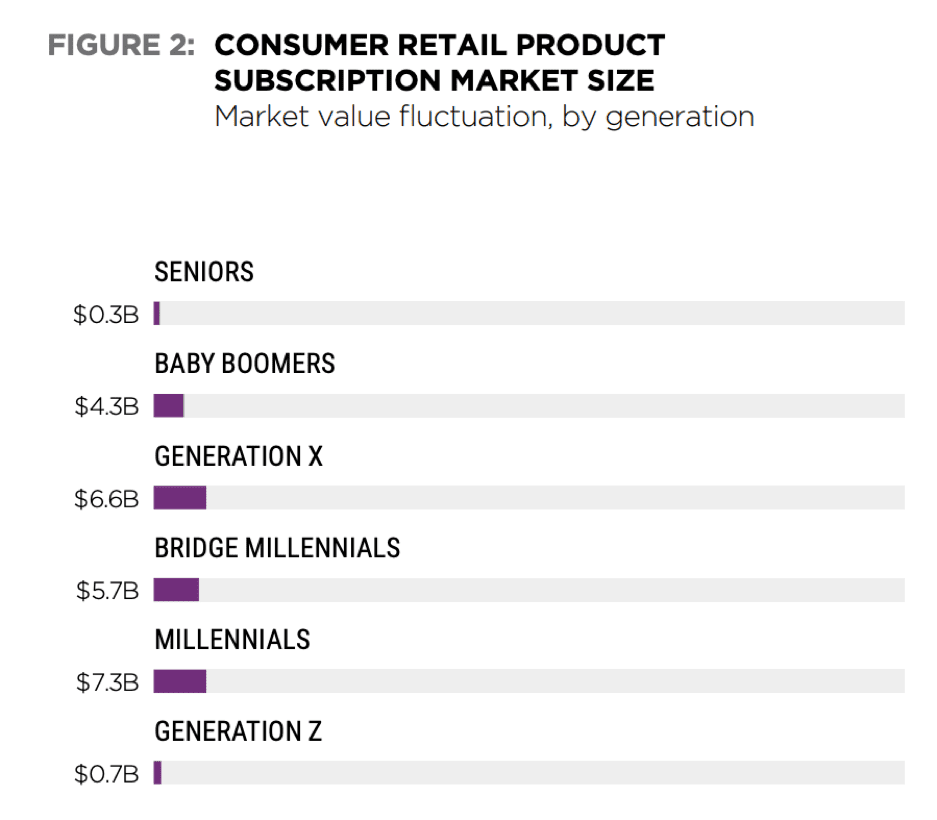

For consumer retail product subscriptions, millennials (25.9 percent) and bridge millennials (24.0 percent) also dominate the market, but aren’t the biggest spenders collectively. Millennials spend $7.3 billion annually on consumer retail product subscriptions, while Generation X consumers pay $6.6 billion each year. Bridge millennials come in third with an annual total of $5.7 billion, while baby boomers spend $4.3 billion over the same period.

Couples with children are the largest spenders ($9.3 billion), though single consumers without children also spend a significant amount ($4.3 billion). Respondents with higher incomes and education levels are also likelier to spend more on consumer retail product subscriptions. Retail product subscribers who earn more than $100,000 annually spend approximately $11.1 billion total, while those who earn between $50,000 and $100,000 spend $5.5 billion and those earning less than $50,000 contribute $2.5 billion.

Retail Subscription Categories: Replenishment vs. Box-of-the-Month

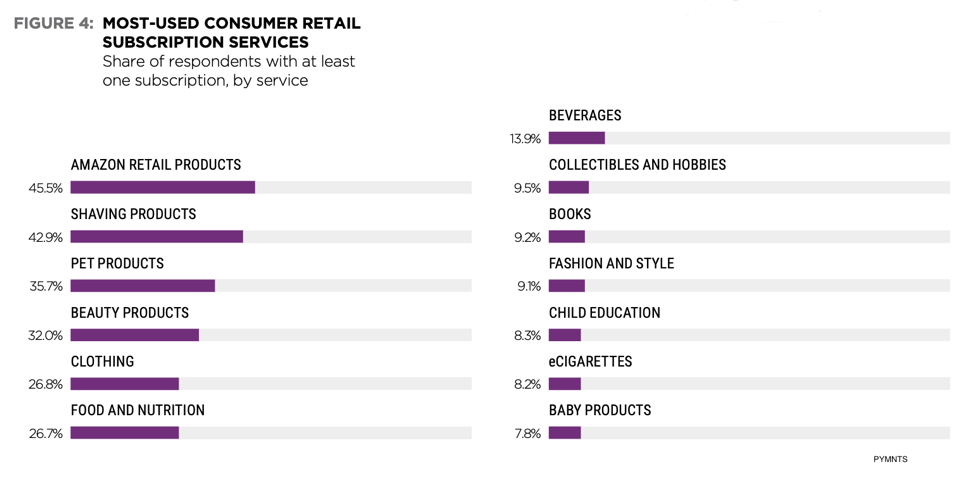

Amazon is the one to beat for online retailing — and this also holds true for subscription commerce. More consumers turn to Amazon for retail product subscriptions than any other type of subscription product service, with 45.5 percent of survey respondents indicating they do so. This share is larger than the combined portion of consumers who subscribe to any single other product category, including the 42.9 percent of shaving products subscribers, the 35.7 percent who subscribe to pet products and the 32 percent who do so for beauty products.

It’s not exactly fair to compare Amazon with its Amazon Prime offering that encompasses free shipping, music streaming and other perks to companies like Harry’s, Birchbox or Rent the Runway that focus on narrower product categories.

The survey reflects these differences between utilitarian services vs. product discovery, as the majority of Amazon subscribers (54.1 percent) subscribe for replenishment. So do 84.3 percent of shaving service subscribers. Beauty products and clothing are the reverse, with 90.1 percent of beauty subscribers doing so for “box-of-the-month” items and 76.2 percent of clothing subscribers doing so for the same reason.

The research also shows another motivation for subscriptions beyond replenishment and product discovery. Consumers pay $959.68 annually on food and nutrition like a la carte meal kits FIX or Butcher Box, delivering grass-fed, humanely raised, sustainably sourced meat to customers’ doors on a monthly basis, compared to just $561.45 on their Amazon-based services, which implies specialty products are a third category that lends itself to subscription commerce.

Different subscription service types also tend to split along age brackets, with younger consumers likelier to subscribe to box-of-the-month offerings and older respondents more inclined to use replenishment services. Each subscriber group has its own reasons for seeking certain services. Box-of-the-month consumers are most likely to value trying new products, with 63.2 percent listing this as their main reason for enrolling in such services. The next most likely reason is ease and convenience, cited by 56 percent of these consumers.

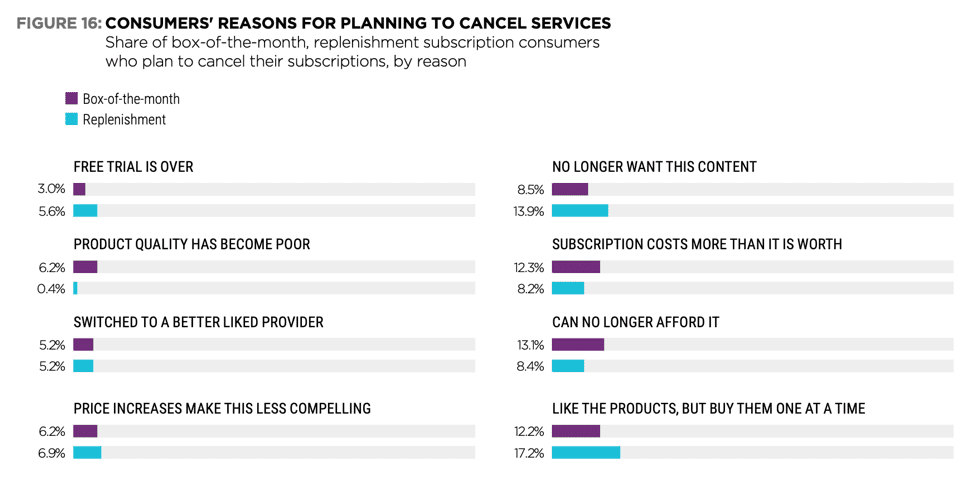

Different subscription service types are also subject to different reasons for dissatisfaction. Box-of-the-month subscribers appear much more likely to cancel their services, with 25.4 percent planning to terminate their services within the next year, compared to 14.2 percent of their replenishment counterparts.

Box-of-the-month consumers are more likely to indicate that they can no longer afford services, that their subscriptions’ costs do not align with their values and that product quality is substandard. Replenishment subscribers are instead likelier to prefer buying products one at a time, indicate they no longer want services or say they concluded free trial periods.

The good news for these merchants is that an overwhelming share of subscribers are highly satisfied with their current services. The subscription box has been a staple of the market for many years, but retailers must take the time to understand what consumers want and expect from services if they aim to keep satisfaction high.