The rise of online and contactless transactions in the European Union, for example, has meant that many merchants are making the bulk of their sales away from brick-and-mortar stores.

Small- to medium-sized businesses (SMBs) have been especially hard hit, as many have pivoted quickly to enable online transactions and adhere to the regulations that often accompany them. SMBs and merchants operating in the EU must comply with strong customer authentication (SCA), which mandates stricter authentication requirements for online and contactless purchases above a certain value. The health crisis has brought about changes to this rule, however, and these may have long-term implications for payment standards and regulations.

In the latest Merchants Guide To Navigating Global Payments Regulations®, PYMNTS analyzes how the pandemic has affected SMBs in the EU, the United Kingdom and the United States. It also examines how  the pandemic’s effects are shifting the ways merchants and customers view payments and their financial relationships.

the pandemic’s effects are shifting the ways merchants and customers view payments and their financial relationships.

Around the Data Protection World

Financial players around the world are upgrading or launching solutions to help them offer swift payments. Canadian payments service RevoluPAY, for one, recently received a Pan-European revised Payment Services Directive (PSD2) banking license that allows it to provide solutions for businesses in the European market. The service aims to support B2B payments with application programming interfaces (APIs) that promote quick transactions. Banco de España, Spain’s central bank, granted the license, which enables RevoluPAY to operate within all 27 EU member countries. Regulators originally looked to use such licenses to shore up open banking and offer more support to digital-only banks and financial services.

Other entities are launching solutions designed to respond to SMBs’ and merchants’ shifting payment concerns amid the pandemic. Some regulations have recently been modified to offer customers and merchants added flexibility, with the contactless payment limit past which SCA requirements apply being increased in the EU and U.K. from 30 euros to 50 euros ($33.67-$56.12), for example. This change has prompted more compliance-related questions from SMBs, however, and ePayments provider Ingenico has crafted an SCA suite that leverages online security protocols to assist firms with following the requirements.

Other entities are launching solutions designed to respond to SMBs’ and merchants’ shifting payment concerns amid the pandemic. Some regulations have recently been modified to offer customers and merchants added flexibility, with the contactless payment limit past which SCA requirements apply being increased in the EU and U.K. from 30 euros to 50 euros ($33.67-$56.12), for example. This change has prompted more compliance-related questions from SMBs, however, and ePayments provider Ingenico has crafted an SCA suite that leverages online security protocols to assist firms with following the requirements.

Data privacy and security continue to be top priorities for many regulators, too. The Irish Data Protection Commission (DPC) recently submitted a draft decision on whether social media site Twitter violated the EU’s General Data Protection Regulation (GDPR) standards with its data collection methods. The DPC has been investigating how the social media service handles its users’ data since 2018, when it received its first complaint alleging that Twitter was not adhering to GDPR requirements. The draft decision is currently not available to the public, but Twitter could be fined for noncompliance if it is found to have violated the rule.

For more on these stories and other headlines, read the Tracker’s News & Trends.

How the Pandemic Is Driving Contactless Payments Forward

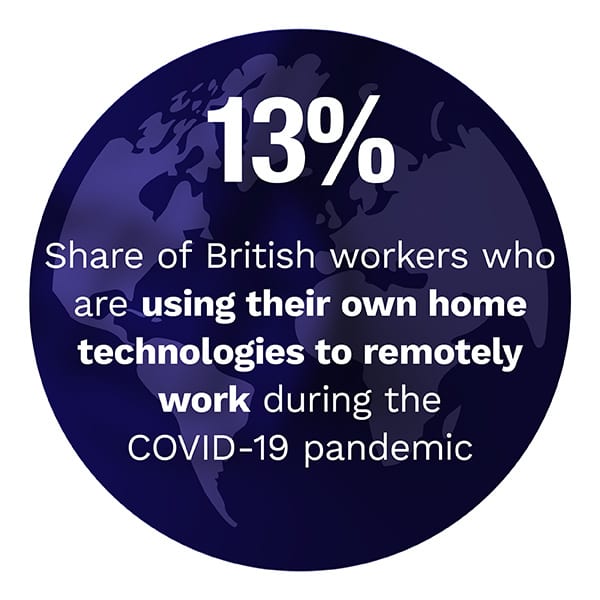

SMBs are responding quickly as the pandemic changes the payment landscape, with closures of brick-and-mortar locations leading more customers to purchase their goods through online platforms. Even consumers who do venture to stores are turning to touchless payment methods to avoid virus-related potential health risks, thus accelerating an ongoing shift toward contactless payments in certain regions.

Such transactions have been popular in the U.K. for some time, for example, but the rules attached to them have c hanged as their adoption grows, and the pandemic may have long-term effects on how those rules are structured in the future, Maha El Dimachki, head of payments for the U.K.’s Financial Conduct Authority (FCA), explained in a recent interview with PYMNTS.

hanged as their adoption grows, and the pandemic may have long-term effects on how those rules are structured in the future, Maha El Dimachki, head of payments for the U.K.’s Financial Conduct Authority (FCA), explained in a recent interview with PYMNTS.

To learn more about how contactless payments usage and other behaviors are changing due to the crisis as well as how banks, merchants and regulators are responding, visit the Tracker’s Feature Story.

How SMBs Can Respond to Shifting Payment Regulations After the Pandemic

SMBs are finalizing and accepting large volumes of online and contactless transactions as a growing number of consumers turn to these methods. These purchases must be authenticated under existing security and open banking rules in the EU and the U.K., however, notably SCA. Shifting standards and questions regarding SCA have thus begun to proliferate among the regions’ merchants as they struggle to comply with the rule while ensuring they can satisfy their customers’ payment needs.

To learn more about how the pandemic may be affecting consumers’ payment preferences and what that means for open banking, visit the Tracker’s Deep Dive.

About the Tracker

The Merchants Guide To Navigating Global Payments Regulations®, a PYMNTS and Ekata collaboration, is the go-to monthly resource for updates on the trends and changes regarding PSD2 as well as other privacy and data protection regulations.

The pandemic has drastically affected how consumers are shopping and paying for even routine purchases, and this in turn has altered how businesses are accepting their payments.

The pandemic has drastically affected how consumers are shopping and paying for even routine purchases, and this in turn has altered how businesses are accepting their payments.