The buy now, pay later (BNPL) race has spent the better part of the last two years expanding and speeding up, as an ever-increasing number of big-name entrants wade into the market, including PayPal, Visa and, most recently, Apple (according to the rumors).

The reason behind the rush is obvious when looking at the data from PYMNTS’ Buy Now, Pay Later Tracker and other sources. Corporate interest is following booming consumer demand and extreme loyalty to the product. Some 48 percent of BNPL users will not buy from a merchant if they don’t offer a BNPL option. And that strength is particularly notable among younger consumers: More than 26 percent of millennials and nearly 11 percent of Gen Z consumers had tapped BNPL to finance their most recent online purchases, compared to only 7.5 percent of older generations who had done the same.

Why that sudden upswing in interest among consumers, particularly those early in their financial services journeys? PYMNTS’ July 2021 Buy Now, Pay Later: The Financial Self-Care Revolution Report offers some insight: The study found that “BNPL provides a rapid pathway to retail shopping for larger purchases and helps rescue blemished credit histories.” Moreover, the report found that ease of use and the ability to spread out payments into more manageable installments were the most cited reasons for choosing the method, regardless of a customer’s financial history or access to mainstream credit products.

“Most of our consumers viewed Sezzle as a great tool for budgeting online purchases,” Sezzle President and Co-Founder Paul Paradis told PYMNTS in a recent discussion. “We’re seeing a significant shift to a more mainstream consumer audience recently. Most of our users own a credit card, but use it as an emergency tool … for big or unexpected purchases, not their preferred payment method. And they’re looking for a better alternative.”

From a customer’s perspective, BNPL is a better alternative, offering the expanded buying power of traditional credit offers, without the corresponding pitfalls that tend to come along with it. But are merchants really keeping up with the rapidly evolving BNPL segment? The latest PYMNTS BNPL Pulse Survey, conducted between May 25 and June 4 among 304 small businesses, indicates that they still have some catching up to do.

Where Firms Are Seeing The Action

Though this is starting to change — care of things like Afterpay’s expansion into Westfield Mall properties — BNPL offerings are still very much an online experience from a merchant’s perspective.

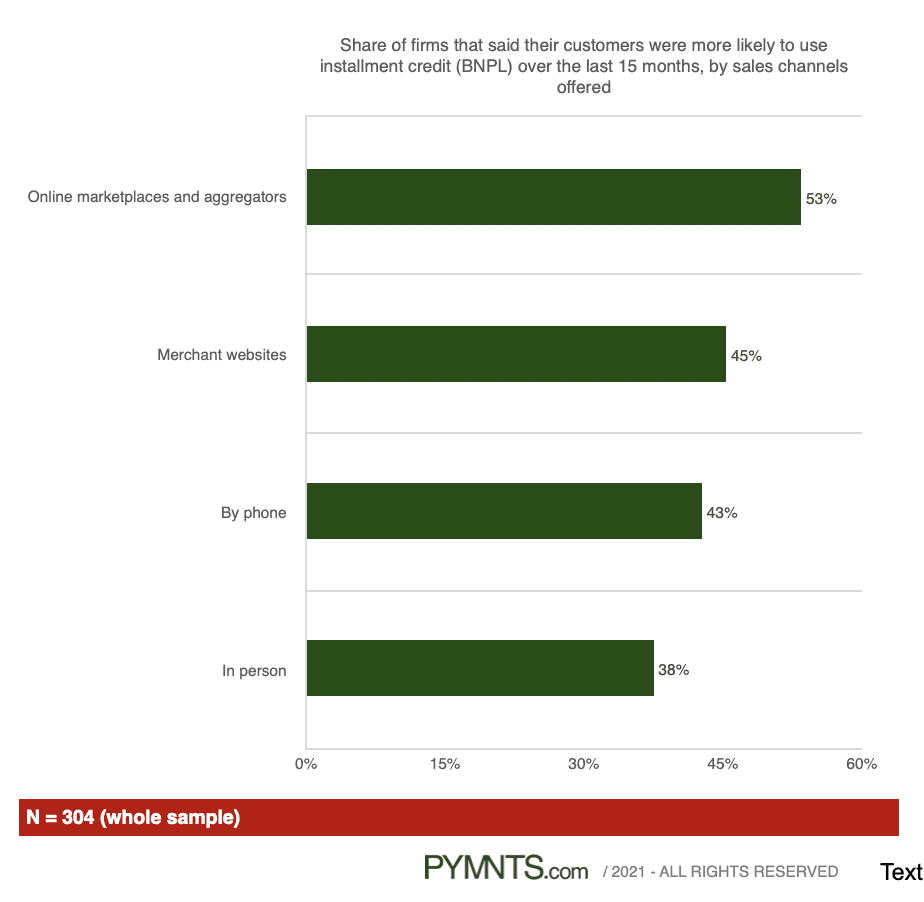

Demand for BNPL programs is higher among consumers who buy products and services from online marketplaces and aggregator sites, where some 53 percent of BNPL users leverage the service — or on merchants’ home sites, where 45 percent of BNPL consumers tend to flock.

Flexible payment options like BNPL do somewhat worse when costumes are shopping in-store or via mobile phone, with 38 percent reporting in-store use and 43 percent reporting seeking flexible payment options when shopping from their phone.

Flexible payment options like BNPL do somewhat worse when costumes are shopping in-store or via mobile phone, with 38 percent reporting in-store use and 43 percent reporting seeking flexible payment options when shopping from their phone.

The data also reflects a slight urban tilt to BNPL use, though perhaps not a very powerful one. Cities with over a million residents have been seeing the fastest growth in BNPL usage over the last 18 months, with 40 percent of merchants in large cities reporting a pick up in demand for BNPL services. That was followed by small cities, 38 percent of which reported a BNPL pick-up, while those in towns or rural areas saw a 32 percent increase in consumers singing on for BNPL. The gap is there, the data show, but it has been narrowing.

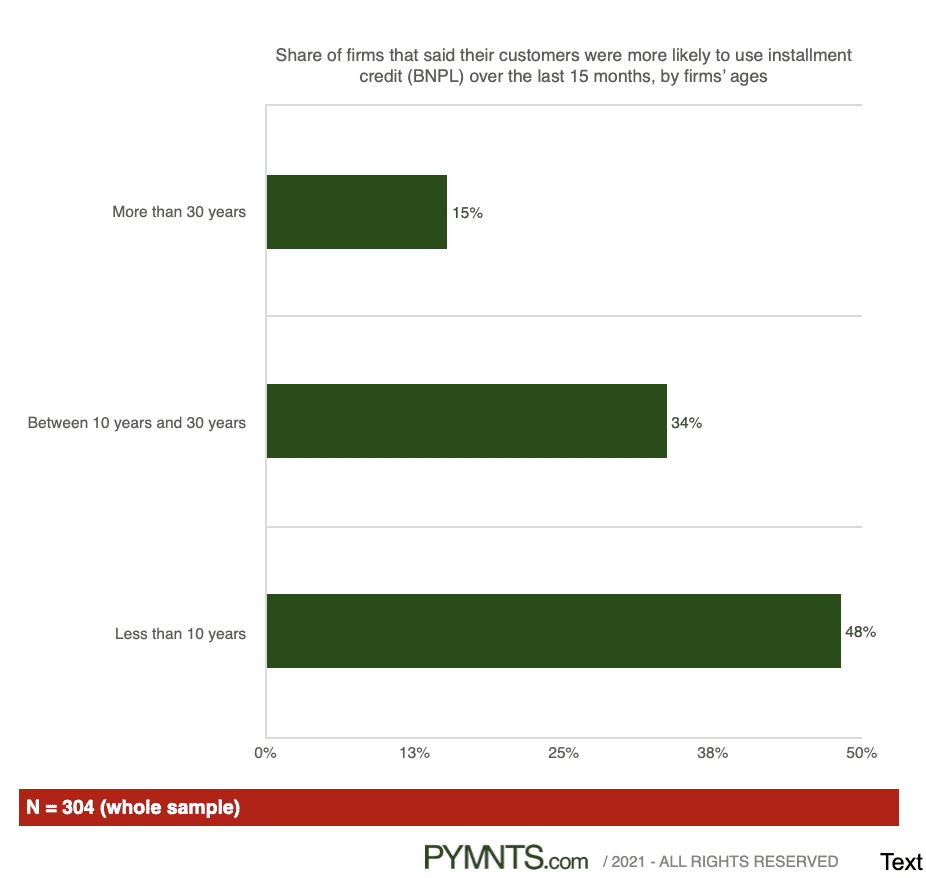

Perhaps the most eye-catching element of the latest PYMNTS data is the fact that the age of consumers is not the only heavily influential determinant of BNPL use: The age of the firm also seems to play a large part.

According to the forthcoming data, firms that are less than 10 years old are seeing three times more BNPL use than those that are more than 30 years old. Only one-sixth (about 70 percent) of firms that are more than 30 years old are seeing greater demand for installment credit options compared to the 48 percent of firms that are less than 10 years old. Businesses somewhere in between 10 and 30 years old are also seeing a surge in BNPL use, with 34 percent saying that their customers are more likely to use those options.

The data seems to indicate that BNPL is expanding its reach and range among consumer groups in a wider variety of contexts. Merchants — older ones in particular — must do some repositioning to ensure that they’re taking advantage of the BNPL opportunity in as many contexts as possible.

The data seems to indicate that BNPL is expanding its reach and range among consumer groups in a wider variety of contexts. Merchants — older ones in particular — must do some repositioning to ensure that they’re taking advantage of the BNPL opportunity in as many contexts as possible.

Because, as Afterpay General Manager of North America Zahir Khoja told PYMNTS in a recent conversation, participating in the rapidly redefining future of retail will increasingly depend on it.

“[Consumers] are going to want to spend and buy and purchase in person — data tells us that millennials are among the most eager to get back into the mall,” he noted. “So adding technologies like buy now, pay later into traditional shopping centers is another step to bring them into this world of the future of retail.”