Consumers’ awareness of — and comfort with — buy now, pay later (BNPL) payment methods has been growing recently, with these options expected to facilitate $680 billion worth of transactions globally in 2025. BNPL allows customers to receive their purchases right away while deferring the items’ full costs by paying them off with several installment payments — an approach that can help consumers who otherwise could not afford these purchases or comfortably pay for them upfront. Users can also typically avoid fees as long as they meet each installment payment deadline.

Such financing methods appear to hold particular sway with younger shoppers, who are often in more precarious financial positions than their older counterparts and thus more in need of options that allow them to postpone full payment for purchases. These younger generations also make up a vast shopper base, with Generation Z comprising 2.6 billion young adults globally as of 2020. Brands looking to grow by attracting and winning over this large base of young consumers may therefore find that offering BNPL solutions is a crucial step for success.

This Deep Dive digs into PYMNTS’ findings from a recent survey of 2,977 U.S. shoppers about their BNPL habits and preferences. The survey investigated how use of BNPL services varies across generations and how these age groups’ different financial outlooks could be influencing the results.

BNPL’s Youth Uptake

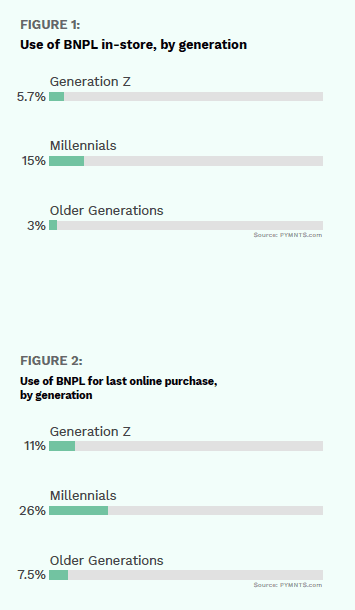

Consumers of all generations use BNPL tools, but millennial and Gen Z shoppers are doing so at markedly higher rates than older generations. PYMNTS’ survey found that 15 percent of millennials and 5.7 percent of Gen Z consumers used BNPL in-store compared to only 3 percent of older generations, for example.

The same kind of disparity was reflected in shoppers’ preferences for their eCommerce purchases as well. More than 26 percent of millennials and nearly 11 percent of Gen Z consumers had tapped BNPL to finance their most recent online purchases, compared to only 7.5 percent of older generations who had done the same.

BNPL’s Resiliency In Millennials

Consumers’ shopping behaviors naturally change as their financial situations — and even the seasons — shift. Survey respondents as a whole spent less online and made fewer eCommerce purchases in February 2021 than they had in November 2020, for example, perhaps reflecting a drop-off in shopping following the holiday season. Respondents made 2.2 online retail purchases in February, down from 2.6 in November, and spent an average of $201 online in February compared to $262 in November.

Use of BNPL online declined during this time, too — an understandable trend, given that shoppers were buying less. The effect was less striking for millennials, however, whose BNPL usage dipped from November 2020 to January 2021 but then nearly rebounded to earlier levels by February 2021. Survey respondents did not explain the reasons for these changes, but the rebound in BNPL use among millennials suggests that this purchasing method remains an important tool even as some shoppers may be tightening their belts and reducing overall eCommerce spending.

The Paycheck-To-Paycheck Factor

Younger shoppers are distinct in many ways that may explain their heavier BNPL usage. Many members of Gen Z and the millennial generation are on shakier financial footing, which can have a strong influence on the payment tools that shoppers have available to them or prefer to use. PYMNTS’ research finds that only 35 percent of Gen Z and 31 percent of millennials said they did not live paycheck to paycheck, compared to 47 percent of older shoppers. Sizable portions of these younger demographics also said they struggled to make ends meet.

Younger consumers with less money in the bank and perhaps less secure employment are apt to have a greater need for solutions that can assist them in buying large-ticket items that they cannot easily purchase in one go, and individuals who have been through financial struggles may not have the credit scores to obtain credit cards for this help. BNPL offerings are thus positioned particularly well to suit Gen Z and millennial shoppers’ current needs. Time will tell whether these shoppers stick with such methods as they get older or whether the generations below them will take over as primary users. BNPL methods nonetheless appear poised to serve the needs of young consumers who are still establishing themselves financially — and to generate income streams for the merchants that offer them.