In terms of any business strategy, scale matters and Affirm now gets to have two of the largest retail heavyweights tied to its payment network.

Read Now: Amazon Moves Into BNPL Space With Affirm Partnership

But for retail, in general, Amazon’s partnership to bring BNPL more broadly to its hundreds of millions of customers across the U.S. is yet further evidence of nod to the fact that consumers want some control and visibility into how they can conserve cash flow, and improve credit along the way.

The rise of the partnerships, perhaps, fires ominous shots across the bow for banks — namely, that they’ll have to innovate to compete, to offset the impact to card payments and to bring their own fine-tuned BNPL efforts to greater prominence — or get left in the dust.

For Walmart and Amazon, the Affirm partnership represents some strategic thinking, too as they eye each other warily across in-store and online sales channels. Walmart and Affirm announced their own omnichannel pact back in 2019. As had been announced back then, the pact initially gave shoppers the option of using Affirm to pay for their purchases over time, in person, at 4,000 Supercenters nationwide. That functionality has also been rolled out to Walmart.com.

Advertisement: Scroll to Continue

Amazon’s announcement with Affirm is only the latest in a string of seismic events in the BNPL space. Square is buying Afterpay, of course, and that, though it’s only speculative thinking, perhaps that might have been a flashpoint that has set off the Amazon/Affirm linkup.

Read More: What The Square Afterpay Deal Means For BNPL, FinTech, BigTech And Banks

We’ll note that there’s at least some prologue to the Amazon and Affirm announcement in the fact that within Affirm’s own “ecosystem” of affiliates and merchants, Amazon indeed has had a presence. Shopping through this conduit gives a consumer an idea of how much they can spend at Amazon, for example, and no doubt has given both firms a sense of how (and where) BNPL has its appeal as part of the Amazon eCommerce experience.

Affirm, of course, makes money by earning commissions from the businesses (which, per its SEC filing, varies according to the merchant, though reports are that the percentages can be in the low- to mid- single-digit percentages), or by charging interest on some items.

For Amazon and Walmart, sharing the same BNPL platform comes as the companies joust for consumers’ wallet share.

By the Numbers

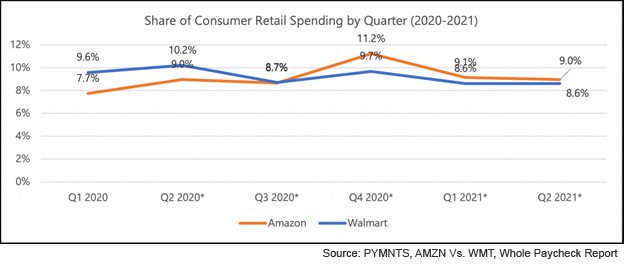

PYMNTS data show that the two retail behemoths are essentially neck and neck in overall retail market share, where in the second quarter of 2021, Amazon had an estimated 9% share of overall retail sales, Walmart had an 8.6% share.

By bringing BNPL to its U.S. consumers (installment payments are available in other countries), Amazon is latching onto a payment option that is gaining traction among all income levels and particularly those for whom traditional credit options are out of reach. PYMNTS research shows that of those consumers that suffered a several financial shock — a bankruptcy, loss of a job or death of a partner or spouse — more than two-thirds of them have or are interested in using BNPL to make purchases. And, importantly, to build back their credit. For merchants, those consumers represent incremental customers, and for those consumers, BNPL represents an opportunity to buy using credit with a predictable and manageable financial guard rail.

BNPL Gains Traction

As reported in a recent BNPL PYMNTS Tracker, 29 million adults in the U.S. have used BNPL at least once in the last 12 months. That equates to about 14% of online shoppers here in the U.S. and with Amazon/Affirm in the mix, and its natural “top of mind share” for online purchases, the net gets cast a bit wider.

See also: Buy Now, Pay Later: The Financial Self-Care Revolution Report

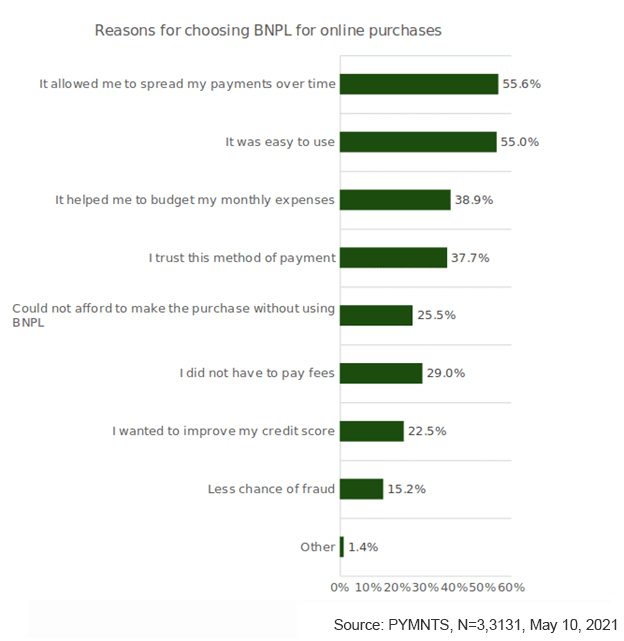

By and large, the perception on the part of the consumers is positive — particularly in terms of managing expenses, and for ease of use.

But it’s underneath the surface that we find that the competitive landscape may be marked by quite a bit of jockeying.

Consider the fact that, as detailed in past PYMNTS coverage, more than 26% of BNPL users ranked PayPal as their most preferred provider. Next on the list, in terms of market share (as measured by volume) credit card-offered BNPL services were ranked as the most preferred option by 18.3% of users. In the third and fourth spots, were Afterpay (at 13.9% share of BNPL users), Affirm (at 11% of BNPL users).

See Also: Buy Now, Pay Later: 5 Fast Facts

By bringing Amazon into its fold, though, Affirm may, in one shot, gain some ground against PayPal. Although PayPal may boast online wallet dominance, Amazon has more than 50% of online sales’ market share (which, incidentally, has far outpaced Walmart’s levels).

PYMNTS research also finds that 64% of consumers who use BNPL believe that BNPL providers are “more trustworthy service providers than banks or credit card companies.” And nearly half of the more than 7,000 individuals PYMNTS surveyed said that “BNPL providers are more trusted service providers than banks or credit card companies.”

See Also: Buy Now, Pay Later: The Financial Self-Care Revolution Report

Those responses seem to signal at least some friction ahead for traditional financial institutions (FIs) as well as a marked difference in the user experience and how the offer is presented. Affirm’s user experience, as with other pure-play BNPL providers, signal the availability of BNPL on product pages and as purchases are being considered. At a high level, the Amazon/Affirm’s efforts seem to be competing with its Amazon Prime Chase card, which also offers installment payments but not until checkout, similar to other examples, including Citi’s Flex Pay and JPMorgan’s My Chase Plan. Amex’s Plan It was expanded last year, to include platinum cardholders, after that option had been made available to Green and Gold members, again post-checkout. In recent PYMNTS surveys, more than 60% of respondents said that the Amex offering helps them improve their credit scores and manage their spending.

Read Also: American Express Expands BNPL Options For Cardholders