The most useful signal in consumer spending may not be how Americans feel about the economy. It may be how much room they have to keep moving.

That is the practical takeaway from “The Three-Speed Consumer Economy: How Financial Capacity Is Rewriting Spending Behavior,” a June 2026 PYMNTS Consumer Expectations Index (PCEI) report. The report helps explain why weak confidence has not stopped spending. Consumers are not moving as one bloc. Some have enough savings and job security to keep buying. Others still spend, but hunt harder for value. A third group is losing cushion fast. For merchants, banks and payments providers, the lesson is clear: a single sentiment number can blur the signals that shape real purchase behavior.

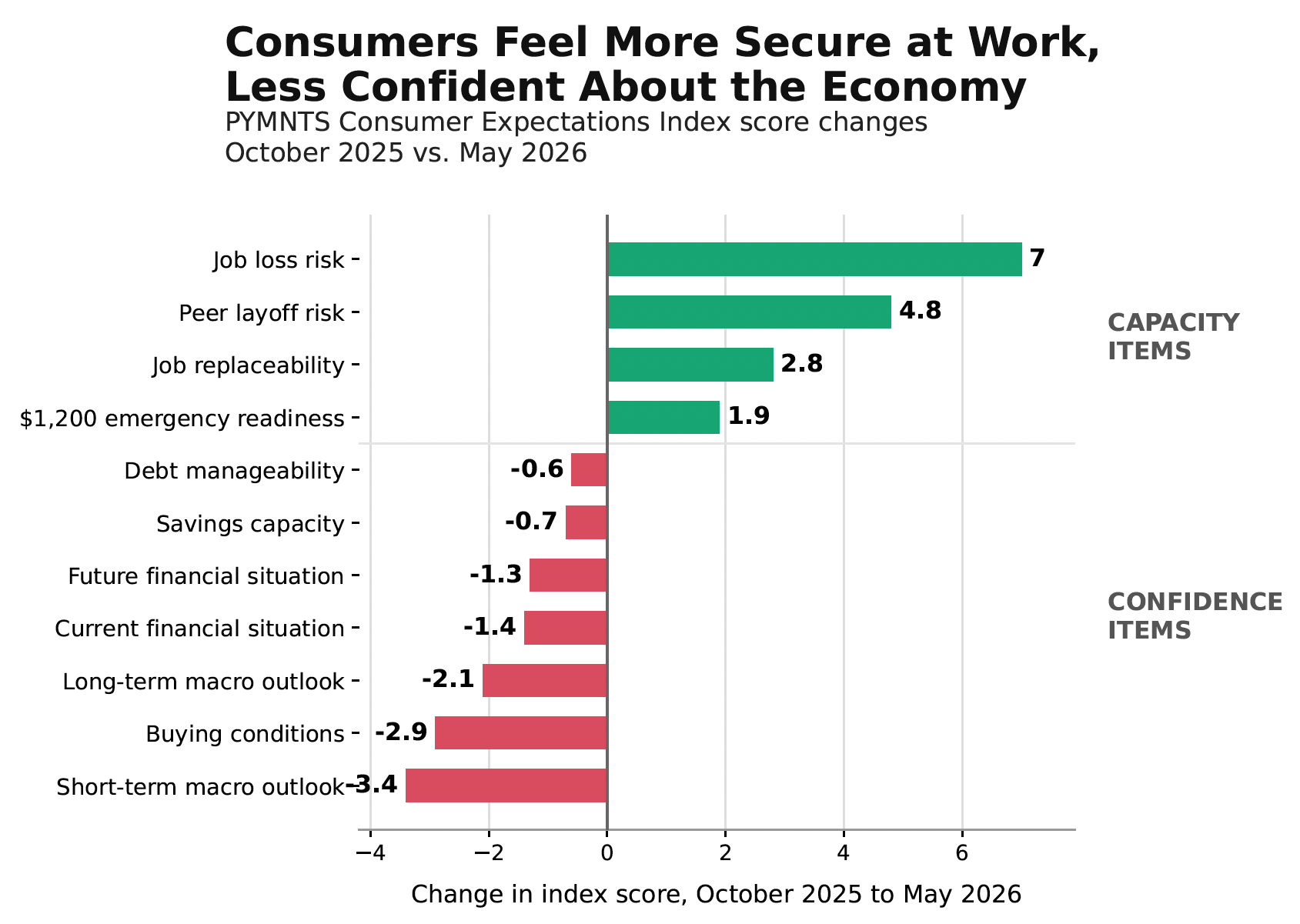

Key Points

- Job security improved while confidence fell. From October 2025 to May 2026, consumers’ perceived job-loss risk improved 7.0 points, peer-layoff risk improved 4.8 points and job replaceability improved 2.8 points. At the same time, short-term macro outlook fell 3.4 points and buying conditions fell 2.9 points. Consumers may dislike the economic weather, but many still trust the roof over their own heads.

- The consumer gap widened to about 21 points. Consumers who do not live paycheck to paycheck posted a PCEI score of 61.9 in May, while consumers living paycheck to paycheck and struggling to pay bills fell to 40.6. The divide expanded from roughly 18 points to about 21. The split came mostly from the bottom group weakening, not the top group surging.

- The middle is still active, but more selective. Consumers living paycheck to paycheck without trouble paying bills held nearly flat at 56.2. They are the value-conscious middle of the market, still spending but more focused on predictability, loyalty offers, bundles that can be budgeted and total cost. They resemble a driver keeping both hands on the wheel while scanning for lower gas prices.

That creates a more constructive view of consumer spending than the usual confidence story. The economy is not being carried by blind optimism. It is being supported by households that still feel secure at work and by a middle group that remains reachable when offers feel practical and transparent. The risk sits with consumers whose financial resilience is shrinking. For them, rigid payment terms, late fees and one-shot bills can turn a short-term squeeze into customer loss. Flexible due dates, split payments, low-cost liquidity and earned-wage access can help keep demand in the system.

The report’s broader message is that the average consumer is no longer a reliable guide. Businesses that see the three speeds clearly can protect margins at the top, retain the value-focused middle and support the most strained customers before pressure becomes permanent.