Demand for contactless payment options has been at an all-time high since March of last year, spurred by the World Health Organization, which warned then that cash use could further fuel the virus’s spread.

Twenty-nine European countries responded by discouraging physical modes of payment and encouraging contactless point-of-sale (POS) transactions, which ramped up. Members easily latched on to the convenient, secure and speedy appeal of touchless methods, and contactless credit and debit cards and mobile wallets gained popularity.

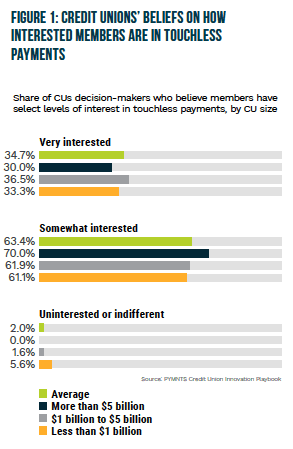

There is room for improvement in credit unions’ (CUs’) efforts to support such payment methods, however. A PYMNTS report found that only about 34 percent of CUs invest in contactless cards, even though 86 percent of CUs invest in mobile wallets. CUs routinely underestimate the latent appeal of these contactless technologies, and nearly 35 percent of CU decision-makers said they believe their members are “very” interested in touchless payments.

The following Deep Dive examines how CUs are currently missing the mark in meeting their members’ contactless payment wish lists and details how they can help meet this demand to keep members engaged.

The Global Surge Of Contactless Payments

The drive for contactless payment options started slow but soon intensified into a stampede, and financial institutions (FIs) have had to quickly react. Major card issuers rolled out new technologies, and consumers began to adopt them en masse, making contactless options the new de facto payment of choice.

Visa noted in April that it had processed 1 billion contactless payments in Europe in less than a year, for example, while Mastercard estimated that at least 75 percent of payments processed in Europe are touchless, illustrating the immense growth. CUs must keep up with major players and take note of these changes in member behavior to stay at the forefront.

These behaviors are predicted to stick around for some time, too. A report revealed that 70 percent of consumers from 18 countries expect to use a contactless card by the end of 2021. Millennial and Generation Z consumer groups are becoming the most enthusiastic adopters, with reports finding that more than half of the 46 percent of global consumers who made contactless cards “top-of-wallet” were younger than 35 years old. Seventy-four percent of respondents said they plan to continue using contactless payments even after the pandemic has eased, entrenching contactless as an essential payment option in a post-pandemic world.

CUs’ Responses To Members’ Desires For Contactless Cards

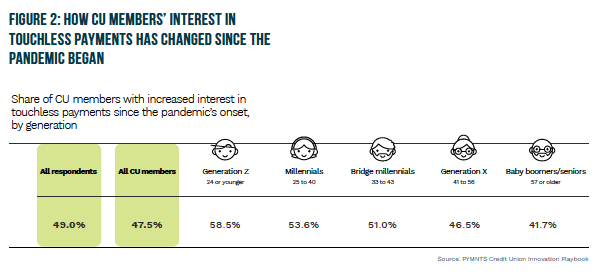

A majority of CUs prioritize investing in mobile wallets, yet relatively few CUs focus on issuing the contactless cards that a majority of CU members told PYMNTS they plan to use. Several hurdles prevent CUs from delivering the contactless capabilities members want. CU decision-makers often underestimate members’ levels of interest in such payments, as only 35 percent of decision-makers gauge that members are “strongly” interested in touchless payments. Forty-nine percent of all consumers and almost 48 percent of all CU members are more interested in using contactless credit and debit cards, mobile wallets, cards on file and QR codes now than they were before the pandemic began, however.

CUs have the potential to benefit significantly from reevaluating their agendas and prioritizing touchless credit and debit cards. Those that issue these cards could capitalize on the advantages of speed, convenience and security that drive users to increase their spending across their accounts. PYMNTS’ Credit Union Innovation Playbook found that 36 percent of CU members would be “somewhat” likely to switch their primary FIs for access to touchless payment options, meaning that investing in contactless innovation could help attract new members or secure the attention of existing members.

An annual study by credit union service organization (CUSO) PSCU showed that many CU members and consumers are either uncertain how to use contactless cards (17 percent) or concerned about their security (31 percent). This creates an engagement opportunity to help educate them on how to use their touch-free cards as well as reassure them of their security features.

CUs can also diversify their payment offerings, keep a pulse on what their members prefer and, if they provide merchant payment solutions to small businesses, persuade those members to offer a variety of payment options. Eighty-four percent of global consumers said they expect to find their preferred payment method of choice wherever they want to make a purchase.

An optimistic future is ahead for CUs that invest in and support contactless payments at a time when demand for them is not slowing down. Providing members with the payment experiences they seek could help CUs maintain a competitive edge and prevent them from losing members to larger banks or FinTechs that support this demand more effectively.