“The currency isn’t going to work,” the executive said. “You can’t have a business where people can invent a currency out of thin air and think that people who are buying it are really smart.”

He went on to call it “a fraud,” and noted he would fire any trader caught messing with it for being “stupid.” Dimon, within a few weeks, had moderated his comments — some. He said he regretted calling bitcoin a fraud, and that the blockchain was a genuinely interesting technology with potential.

When it comes to bitcoin itself, though, as recently as last November, Dimon pretty staunchly remains “not a huge fan.”

“I didn’t want to be the spokesman against bitcoin. I don’t really give [an expletive] — that’s the point, OK?” Dimon clarified.

However Dimon feels about bitcoin these days, JPMC apparently isn’t feeling quite as dimly about the future of blockchain and crypto as its CEO once did. Yesterday (Feb. 14), it became the first major U.S. bank to introduce its own digital token for real-world use. Named the JPM Coin, the blockchain-based cryptocurrency is designed to enable “the instantaneous transfer of payments between institutional accounts,” according to the company’s blog post.

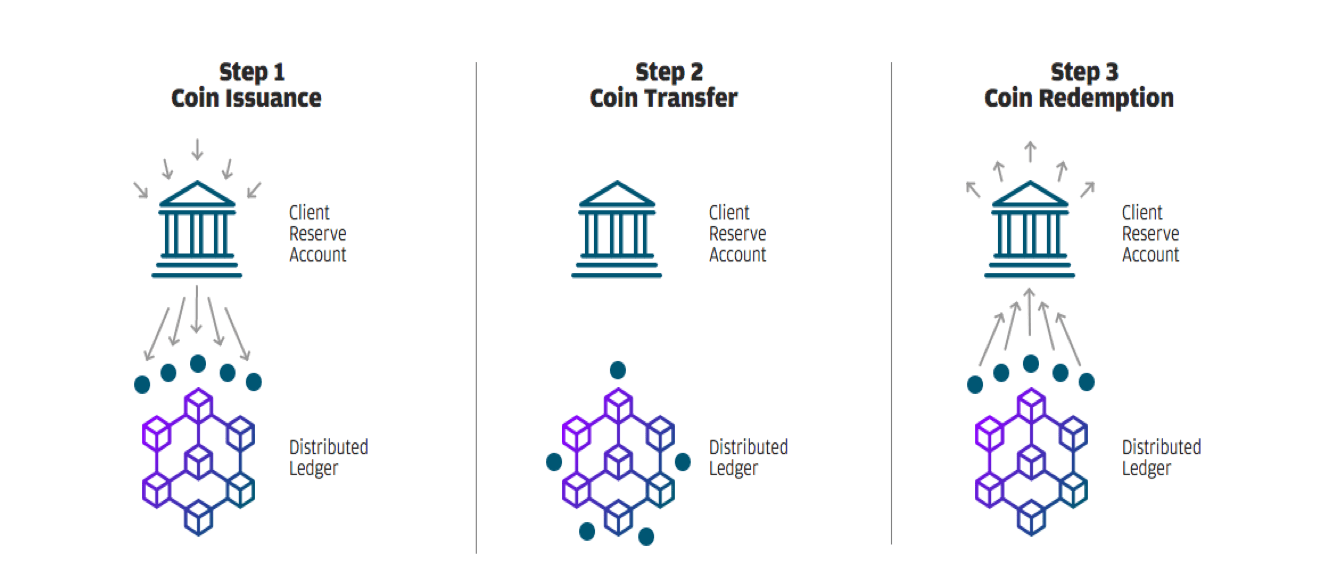

“The JPM Coin isn’t money per se. It is a digital coin, representing United States dollars, held in designated accounts at JPMorgan Chase N.A. In short, a JPM Coin always has a value equivalent to one U.S. dollar. When one client sends money to another over the blockchain, JPM Coins are transferred and instantaneously redeemed for the equivalent amount of U.S. dollars, reducing the typical settlement time,” the blog explained.

The release of the JPM Coin follows the bank’s release of Quorum — a blockchain platform designed to allow institutions to keep track of financial data. According to Umar Farooq, head of treasury services and blockchain for JPMC, the release of the coin represents JPMC’s next natural step in widening its blockchain experiment for its institutional partners.

“Clients engaged us, saying they need a way to move money onto the blockchain,” Farooq told The New York Times in an interview.

The JPM Coin ledger will be controlled by JPMC itself — and each coin will be backed by a dollar, making it a stablecoin at base, not subject to the sort of wild valuation swings that make bitcoin attractive to speculators. To use the coins, a JPMC client commits deposits to a designated account, and receives an equivalent number of JPM Coins. Once the client has said coins, they are used for transactions over a blockchain network with other JPMC clients (e.g., money movement, payments in securities transactions). Once the trades have happened over the network, the new holders of the JPM Coins redeem them for U.S. dollars from JPMC.

The JPM Coin is not for retail customers, but will be used internally by JPMC. Several cryptocurrency exchanges already have their own so-called stablecoins. What’s more, it is still just being tested, and is not available to clients yet.

The main advantage of the new token, according to Farooq, is speed, since tokens will be able to move nearly instantly on the coin’s ledger, which will initially be based on JPMC’s Quorum blockchain. The alternative for institutional clients looking to send large sums, he noted, in the past, would have been a wire transfer that might have taken hours or even days. Moreover, that lag time, apart from being annoying, added to the opacity of the pricing, since currency exchange rates fluctuate.

“This is designed specifically for institutional use cases on blockchain,” he said. “It’s not created to be for public investment.”

The JPM Coin, as mentioned, is not the only stablecoin on the market. Since several cryptocurrency exchanges already have their own, some skeptics noted that JPMC’s choice to move funds via a closed blockchain product is a new tech twist on an old concept.

“It is very similar to corporations’ desires to launch intranets as competition to the open internet system in the 1990s,” said Lawson Baker, founder of Relay Zero, an investment fund in blockchain projects.

It also bears some resemblance to the Utility Settlement Coin that banks like Barclays and Credit Suisse have been developing to make it easier to transfer money between financial institutions.

The big question of the day — in terms of the competitive landscape — is about Ripple, and what the JPM Coin will do to that firm’s relevance. Ripple has carved a niche for itself as an attempted heir apparent to the SWIFT network, used by banks, individuals and businesses to send and receive money.

“This is a huge slap in the face for Ripple,’’ said Tom Shaughnessy, principal at Delphi Digital, a crypto research boutique in New York. “Ripple’s target market is cross-border payments and remittances, and, now, JPMorgan’s effort is a direct threat.’’

JPMC, he noted, moves more than $5 trillion in wholesale payments each day, meaning that even a tiny toe into the blockchain waters from a bank of its size could create some major waves for all the other players. However, Ripple, for its part, is unworried thus far.

“As predicted, banks are changing their tune on crypto,” wrote Ripple CEO Brad Garlinghouse in a tweet. “But this JPM project misses the point — introducing a closed network today is like launching AOL after Netscape’s IPO. Two years later, and bank coins still aren’t the answer.”

San Francisco-based Ripple said it has more than 200 banks and payment providers on its RippleNet network. Yet, not being worried today could change into worry tomorrow, since reports indicated that JPMC plans to work with regulators to gain permission for broader uses of the JPM Coin. That process could take at least several months, according to Farooq.

“We have always believed in the potential of blockchain technology, and we are supportive of cryptocurrencies as long as they are properly controlled and regulated. As a globally regulated bank, we believe we have a unique opportunity to develop the capability in a responsible way with the oversight of our regulators,” the JPMC blog said.