Cryptocurrencies and other crypto-related technologies have been gaining steam among consumers in recent years.

What was once an obscure digital technology is now fairly mainstream, with data from PYMNTS indicating that 23% of Americans have owned crypto in the past year. This number is likely to increase. One survey found that more than 46 million Americans report they will likely buy cryptocurrency in the next year.

There has also been remarkable growth in bitcoin ATMs, or BTMs. Globally, the crypto ATM market was valued at over $75 million in 2021 and is expected to grow at a compound annual growth rate (CAGR) of 59% from 2022 to 2028.

The stunning rise of crypto is occurring against a backdrop of a broader digital transformation sweeping through the financial services industry, fueled by financial institutions (FIs) responding to consumers’ interest in digital products and services. Overall, FIs have retooled their offerings to meet consumers’ digital financial needs, yet when it comes to cryptocurrency adoption, the banking industry has been much slower and more cautious.

This month, PYMNTS examines how banks have been slow to embrace crypto-related product offerings despite significant consumer interest in them doing so.

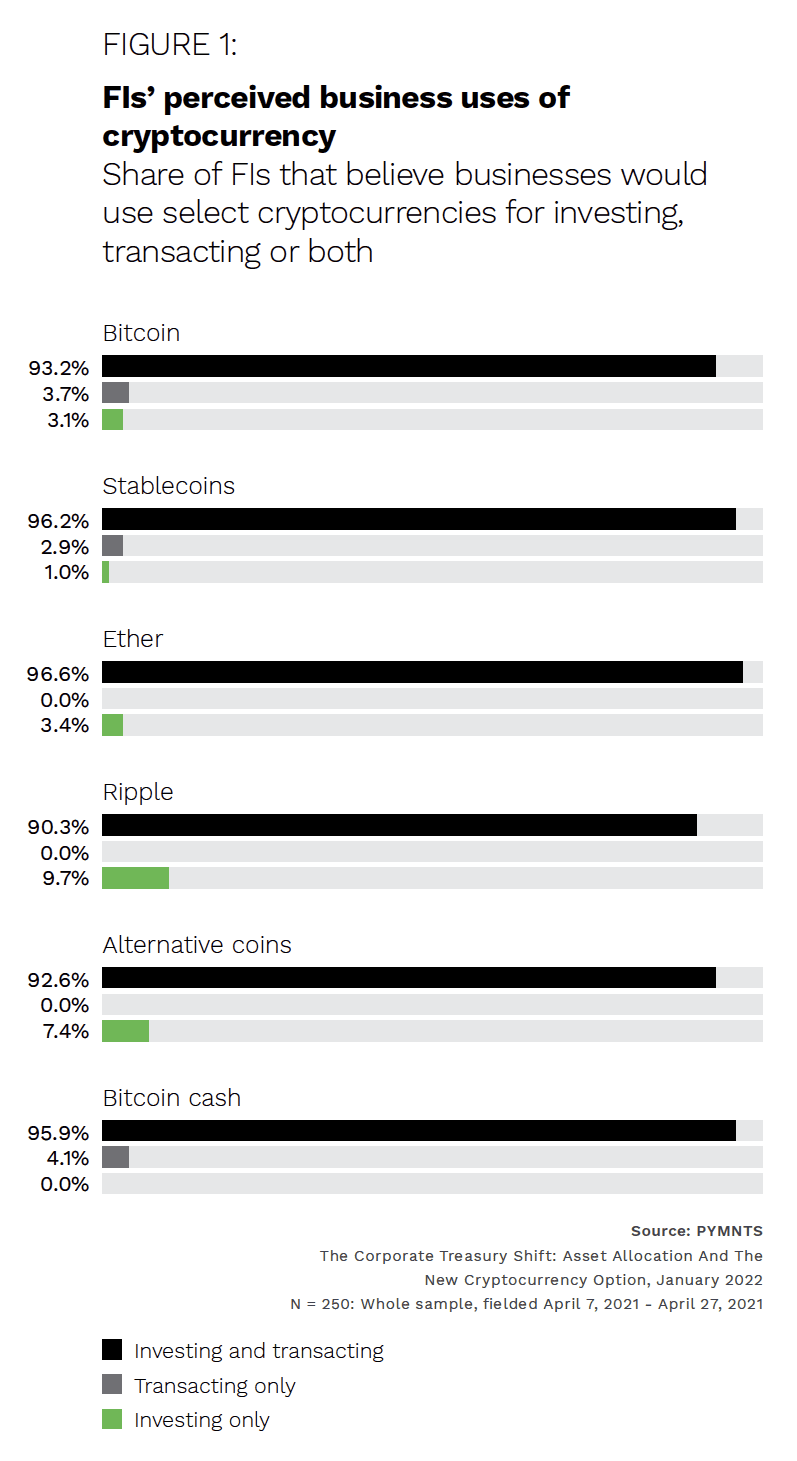

Banks Have Little Crypto Involvement

Although many consumers use cryptocurrencies as a form of payment, crypto is also commonly used as an investment instrument. Banks, however, have been hesitant to espouse crypto in this way. A survey of private global banks conducted by the Basel Committee on Banking Supervision (BCBS) found that only seven of 178 banks had direct cryptocurrency exposure. While more than 100 of the banks did perform some crypto-related activity — such as trading on clients’ accounts — none of the banks reported direct cryptocurrency holdings as long-term investments.

The BCBS report noted that due to traditional FIs’ lack of involvement, crypto trading and storage has been left largely to unregulated crypto exchanges, essentially forming a “shadow crypto financial system.” These exchanges have been proliferating as crypto becomes more popular.

Despite an incremental expansion of crypto exposure, banks still do not view crypto as an immediate priority. According to the Federal Reserve, two-thirds of banks do not view distributed ledger technology (DLT) and crypto-related products and services as a strategic imperative for growth in the next two years. More than 60% of banks also viewed DLT and crypto-related products and services as unimportant to liquidity management over the next two to five years.

Another survey found that eight in 10 FIs have no interest in providing cryptocurrency investing services to their customers, with only 1% of FIs reporting to be very interested in doing so. On the whole, although some banks have begun to dip their toes into crypto, most have not and are not particularly interested in doing so at this time.

Consumers Are Open to Banks’ Facilitation of Crypto Access

While banks have been less interested in offering crypto-related products and services, consumers’ interest in crypto continues to grow, and they are open to using their FIs’ offerings in this area. A survey found that 60% of crypto owners would definitely use their banks to invest in crypto if given the option, and 32% reported they might be interested in such a service. Only 4% of respondents said they would not use their banks’ crypto-related investment services. The same survey found that 68% of crypto-owning consumers are very interested in debit or credit card rewards based on bitcoin.

It is understandable why banks have thus far been reluctant to jump into the world of crypto. Despite their increased popularity, cryptocurrencies remain volatile. While much uncertainty still exists on the regulation front, banks also have their hands full with developing other digital offerings.

However, FIs have an opportunity to satisfy their customers’ interest in cryptocurrencies. Some major banks, such as Chase, are already providing consumers with the ability to link their Coinbase accounts to their traditional banking accounts. Other FIs and FinTechs are also starting to release products that enable customers to access cryptocurrencies more easily. Crypto is not going away, so banks should learn how to evolve their products and services accordingly.