Facebook and Twitter made the news towards the end of last week when they both announced plans to enable commerce from their respective social networks. Facebook is testing a “Buy” button that can enable purchasing directly from a promotion inside a user’s news feed. And, Twitter acquired CardSpring, a platform that could enable merchants to extend card-linked offers via tweets. Sorry to be the ant at the picnic here, but I have some pretty serious doubts about whether either of these players can set the commerce world on fire. Why? Because it’s not obvious what burning commerce and payment issues they solve for consumers.

The player that could is Yelp. And depending upon how it decides to integrate payments within its platform, it could pretty seriously tip the balance of power in the mobile commerce ecosystem.

Hear me out.

I was one of the early advocates of what a couple of years ago was called “Facebook Commerce.” I even spent some time trying to ignite a venture in the “social commerce” space. Having hundreds of millions of people assembled in one place and having the great majority of them checking their news feeds at least once a day seemed to make it a totally logical environment for commerce. What could be better than a walled garden that people visited all of the time and retailers with fans and fan pages that could enable commerce?

Well, as it turns out, shopping the way people always shopped.

There were (and are, I believe) two problems with Facebook Commerce.

The first is that Facebook’s algorithm is designed so that only a very small fraction of fans see anything from brands on their newsfeeds. This sort of came as a big surprise to brands who spent gazillions of dollars getting fans to “Like” them. The dirty little secret of how the Facebook news feed works only became transparent when it was about to go public – long after those investments in acquiring fans were made. So, without massive advertising budgets to go along with those commerce efforts, not enough people were exposed to offers in their news feed, making conversions a challenge. For small merchants in particular who really saw Facebook Commerce as an attractive opportunity, this was lethal. As our resident economist puts it if you multiply a small percent (percent of views) by another small percent (conversions) and you get bubkis. The ROI of any sort of commerce initiative was more than upside down, it was impossible.

But reason number two is probably more important.

The reason that people joined Facebook and visited the site once a day in the first place had nothing to do with buying stuff. People were invited by their friends to join Facebook to keep up with their goings on, check out their photos, share their own and yes, stalk other people’s pages. People weren’t motivated by shopping or even the idea of shopping. Increasingly, people also began to worry about privacy issues and whether what they bought would be broadcast on their newsfeed. Facebook users were used to seeing just about everything that their friends did – what they liked, what photos they posted, what they were listening to on Spotify, even how their farms were doing on Farmville. But since they weren’t entirely sure that commerce applications would work differently, the last thing that people wanted to broadcast was that they just bought a pair of Jimmy Choos for $535 from Neiman’s, especially if one of their friends was their husband. Looking at it that way, Facebook Commerce actually could not solve problems from the consumer’s point of view.

Turning to Twitter, it has one billion registered Twitter users and 255 million active monthly ones. Like Facebook, users visit Twitter to get interesting scoop from the people they follow – celebrities, athletes, industry experts, friends and yes, brands. And, there’s a lot to see, too, something like 500 million new tweets are posted every day. Most people don’t compose tweets (and many of those who do, have others composing them on their behalf) or even engage with them. They just scan their news stream to absorb information.

Like Facebook, there have been a number of attempts to monetize those eyeballs via commerce. Chirpify, which was started in 2011, was positioned as the “hashtag commerce” company now the “action tag” company that would enable action of any kind from a tweet on a page – a donation to a campaign, a purchase from a brand. American Express, Tesco and Amazon, more recently, have all launched “hashtag” commerce on Twitter. But since no one is really boasting about how well they’ve done, it seems safe to assume that Twitter commerce hasn’t exactly delivered compelling results yet. Could users who only passively engage with Twitter find offers to engage in commerce compelling enough to get them to change their behavior? Time, I suppose will tell.

But at the moment, it’s hard to see what commerce and payment problems Facebook and Twitter uniquely solve for consumers. In fact, a McKinsey survey published earlier in the year that said that, yes folks, the lowly Outlook email was 40 times more effective in acquiring customers than Facebook and Twitter combined.

Why is Yelp different?

How about this for starters? Yelp is a commerce company.

Payments is is always easier when commerce is the starting point of a business. Yelp’s stated mission is to connect people with local businesses. And wouldn’t you know – commerce is exactly why consumers use it.

Yelp’s reported stats prove it, too. Eighty – as in 80 – percent of the people who visit Yelp – and that’s 132 million uniques a month – went to Yelp with the intention of making a purchase. Nearly 100 percent of them (98 percent to be exact) made a purchase from a business they found on Yelp – 85 percent within a week and 27 percent the same day.

Yelp’s users also have money to spend. According to Yelp’s own data, 36 percent of its users make $100k or more a year, 60 present of them are college educated, and 36 percent of them are between the ages of 35 and 54 – the GenX’s and Boomers who drive most of the consumer spend today. Yelp says it’s visitors initiate 200k daily calls to businesses for information of some kind, and now they can message them directly from their page on Yelp and skip the telephone entirely. Yelp says it drives 10k food orders every week. And, according to a BCG study done in 2013, on average, businesses say that they can point to about $8,000 a year in revenue from leads from Yelp; some categories report even bigger revenue gains.

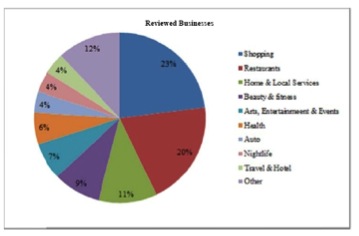

Yelp’s users also like to eat out. Restaurants are the quintessential local business. They also happen to account for 20 percent of the reviewed businesses on Yelp according to the graph that was taken from their 2013 annual report. (Reviews are how Yelp measures what drives traffic to their site, user engagement and therefore the concentration of businesses there.) A Nielsen survey in 2013 found that when consumers search for restaurants specifically, they are much more likely to start with Yelp, in fact 3 times more likely than OpenTable and 4 times more likely than Zagat.

Yelp’s users also like to eat out. Restaurants are the quintessential local business. They also happen to account for 20 percent of the reviewed businesses on Yelp according to the graph that was taken from their 2013 annual report. (Reviews are how Yelp measures what drives traffic to their site, user engagement and therefore the concentration of businesses there.) A Nielsen survey in 2013 found that when consumers search for restaurants specifically, they are much more likely to start with Yelp, in fact 3 times more likely than OpenTable and 4 times more likely than Zagat.

Restaurants also happen to be a category that every payments and mobile commerce player is courting. There are now a slew of mobile apps that enable consumers to pay using a smartphone and a mobile app and to order ahead and pay via the app. But these apps aren’t only being deployed at fast food and fast casual restaurants. Online reservations powerhouse OpenTable, which serves only those restaurants that take reservations, is piloting its own mobile payments app at restaurants in San Francisco. OpenTable users that book a table can pay their check from the app when they are ready to leave the restaurant.

So, this is where I think Yelp could make things very interesting.

I was working on the OpenTable case for Summer School on Reinventing Retail (BTW, have you registered?) and looking at its competitors. The more I started to dig into Yelp, the brighter the light bulb became for me about their potential to enable payment for the businesses they host, and in the restaurant space in particular, and therefore, their potential to tip the balance of power in the mobile commerce ecosystem.

Yelp acquired a reservations service, SeatMe in 2013. As the name implies, SeatMe enables visitors to Yelp’s restaurant pages now to make a reservation at that restaurant. It would be pretty easy for Yelp to also integrate with one of the many mobile payments apps so that anyone searching for a restaurant on their mobile device could not only book a seat but also pay their check (or order ahead and pay online at the restaurants that don’t take reservations). Since most people start searching for a restaurant on their mobile an hour before they want to eat and about 59 percent of Yelp’s searches now originate from the mobile device, it seems like a logical next step for them.

Then I discovered something else.

Yelp is one of the handful of companies that was “selected” to work with Amazon to develop a version of its app for the Fire phone. It’s said to leverage the unique capabilities of the Fire phone OS like its “one handed gesturing” and optimized carousel browsing. Yelp is also tightly integrated with Amazon’s mapping service, which I’m sure is one of the things that Amazon is hoping will get users to use it.

Are you thinking what I’m thinking?

Restaurants are one of the only merchant categories that Amazon doesn’t compete with. Ditto some of the other local businesses that people use Yelp to check out such as hair salons, manicurists, dentists, dog walkers, museums, fitness clubs, cleaning services. That matters because enabling those players to “Pay with Amazon” is of no real threat like it is with other retailers who view Amazon as a competitor. ..

And “Paying with Amazon” is what 209 million can and probably do a lot on Amazon.com. Amazon’s advantage with consumers is that they’re in the habit of using Amazon and their Amazon accounts to buy a lot of stuff. It’s sort of second nature. Amazon is a marketplace of physical goods.

Could Yelp become Amazon’s marketplace of local businesses?

Amazon has 500 million people who come to its website every month so it surely doesn’t need Yelp’s monthly uniques to help it sell more stuff on the Amazon online marketplace. But, if it’s ambition is to build an offline marketplace that is enabled with payment, what better partner to have than a company whose mission it is to connect people to local businesses – and who actually deliver sales to those local businesses? And, don’t forget that at the end of 2013, Amazon bought the GoPago’s payment tech and engineering team. GoPago is a POS platform that allows customers to order and pay for purchases at local businesses, and was heavily penetrated in the restaurant sector. It would seem logical for Amazon to want to integrate Amazon payment capabilities within that platform, and potentially enable an Amazon Payments closed loop network for local businesses

Hmm.

Now none of what I just said requires consumers to buy a Fire phone (I still don’t get how on earth that phone could ever get traction) since an app would suffice just fine. But doing the OpenTable case sure got me to thinking in a whole new way about Amazon’s potential in offline retail and how it could change the balance of power in the mobile commerce space by entering in a category and with consumer and merchant assets that gives them a very attractive value proposition.

Speaking of the OpenTable case, I can’t wait for Professor Edelman to take us through it, but not only to debate OpenTable’s strategic considerations, now 16 years into their business. Like every sector, mobile has introduced a diverse set of players and new business considerations. What would happen if Amazon bought Yelp? That wouldn’t only change the game for OpenTable, but shake up the landscape for mobile commerce more broadly.

I’d love to know what you think.

P.S. If you’d like to participate in the PYMNTS “Deep Dive” on the reinvention of retail at Summer School on August 12 – 14 drop me a note at Karen.Webster@marketplatforms.com and I’ll send you a VIP link to register. Thirty people I respect tremendously will give you in 2.5 days what they have learned about mobile, retail, and payments over decades. In addition to the OpenTable case, we’re doing ShopRunner and Macys and 6 modules that touch every aspect of retail reinvention. Would love to see you there.