In the classic story, The Wizard of Oz, Dorothy, Toto and the Tin Man are happily skipping along the Yellow Brick Road on their way to find said Wizard when they come upon a forest. Dorothy asks the forest whether there are scary animals living there and since this is a make believe story, the trees tell her that there are probably lots of lions and tigers and bears. In order to quell her fear about following the Yellow Brick Road thru a scary forest, she and the Tin Man start chanting, “lions, and tigers and bears, oh my” over and over. Soon they encounter a lion, who turns out to be totally not scary at all, so their mantra becomes sort of a lucky phrase.

As retailers travel the Yellow Brick road to mobile commerce, there are lots of scary creatures that they might encounter along the way. comScore’s recent report on the state of digital in the US produced a number of facts that retailers might find sort of scary as they travel to the land digital shopping and payments Oz. You’ve probably seen snippets of these stats by now but here are four that I think are most relevant payments and retail:

- Just about all of the growth in Internet usage over the past three years has come from consumers using smartphones and tablets.

- Mobile now accounts for 57 percent of internet usage, eclipsing desktop usage

- More than half (56 percent) of all consumers “multi-home” across digital devices – moving between mobile devices (phones and tablets) and PCs (desktops and laptops) routinely and seamlessly.

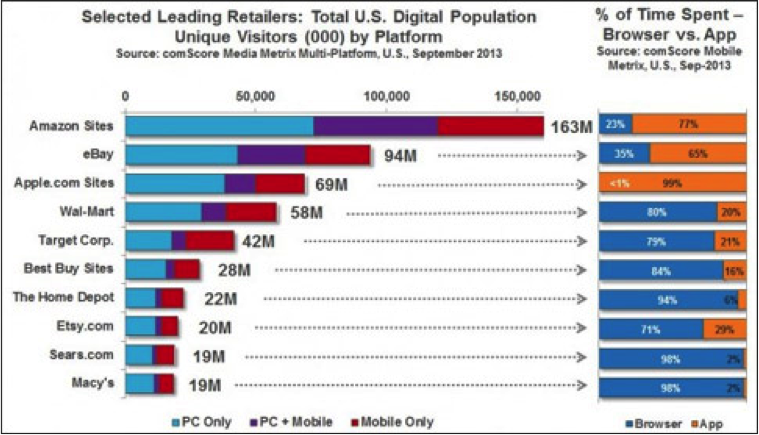

- Consumers love their apps, with 85 percent of Internet time spent on smart mobile devices spent on apps.

To the latter point, not surprisingly, the number one app, by a pretty sizable margin, is Facebook. Now you know why every time you check your news feed, you are bombarded with those annoying retargeted ads that, speaking for me personally, are just a huge turn-off. I don’t particularly like seeing, in what I regard as my private space, an ad for something that I just looked at on a retailer web site. It is a bit too big brother-ish and leaves me liking neither the merchant or Facebook any better.

But, looking at apps and retail, there are two important observations. The first is more than 50 percent (52 percent) of those who have apps from one of the top 50 mobile commerce apps use them to shop once a week (it’s 48 percent for Android users). For physical retailers, the average is 43 percent and for web only retailers its 47 percent. So, if consumers have apps, they’ll use them – and a lot. iPhone users drive more sales volume, incidentally and not surprisingly, e-tailers like Amazon.com Inc., eBay Inc. and Etsy Inc. drive the most mobile app traffic overall.

The second is that those multi-channel retailers that report having the greatest volume of traffic online as measured by monthly unique visitors, report that only a third of their total traffic comes from mobile apps.

So, what should retailers chant on their way down the Yellow Brick Road to mobile commerce?

Apps represent the most direct, potentially most secure and surely the most controlled channel to the customer that ever existed. It is a virtual version of their physical showroom. Within the app, the merchant can control the complete experience – from merchandising, to branding to advertising to offers and, yes, to payments. Within the virtual walls of their virtual storefront merchants can shut out just about everything and everyone that they don’t think adds any value to the consumer and merchant experience – no retargeted ads to distract the shopper, and no payments methods that they don’t chose to support. Consumers with apps, as the data supports, consult them often, and buy using them. Those with Apple devices even spend more when they use them.

(An important note, though, is that the average purchase via the app isn’t greater than the average purchase made in store …so retailers still want consumers in their storefronts!).

Given that merchants now have more tools available to them to more accurately authenticate an app user – the device itself and all of the passwords and now biometric authentications available – why aren’t more consumers using more retailer apps more of the time?

At least up to now, consumers have exhibited the same behavior with respect to apps that they have with store-branded cards and even loyalty cards – they want fewer and make decisions based on the stores they frequent the most. Even though, in theory, a phone can accommodate as many apps as a person wants to download, people use relatively few of the ones they download. Just look at your own screen – how many apps have you downloaded overall and which of those do you routinely use? Moreover, at some point, you aren’t even going to download apps because you know you won’t be able to find things on your phone if it becomes too crowded.

When it comes to retailer apps, consumers download the ones they use the most and then simply use the web when they see an email from a retailer or hear about an offer from one that is not in their top three or four.

This chart from comScore makes that point and sets up a potentially interesting dynamic in the omnichannel and multiplatform digital world in which consumers are living today. Consumers want to move seamlessly between PCs, phones and tablets and increasingly expect the same experience across all of them, regardless of whether they are transacting purely in a virtual world or starting in one world and completing the transaction in another – including payment. Merchants want to control the experience online in much the same way that they do in their physical stores. And just like the offline world, they are faced with lots of competition but not just from other retailers but from social shopping sites, deals and discount sites and aggregators who are all plying the consumer with offers to download their apps too.

Apps and Retailers and Payments, Oh My!

Ok, so back to the Land of Oz.

As retailers navigate the yellow brick road to mobile commerce, there are a number of scary things that can come out of that forest. . The biggest scary thing of all is apathy – consumers just don’t want to download their app. Instead of a harmless competitor without courage (or deep pockets), the Yellow Brick road to mobile commerce is filled with lots of apps that aggregate just about everything under the sun and make those goods available at a cheaper price to those consumers. Getting consumers to download a specific retailer’s app then, is what retailers are off to see the Wizard about.

One of the questions that they might be taking to the great and powerful mobile commerce Oz is the role of third party wallets and apps in helping them solve for this. Oz might point them to the experiences of Alibaba and eBay who are each taking very different approaches to helping bridge the retail and consumer and mobile gap. Instead of asking consumers to download different merchant apps, they are each using payment enabled marketplaces to make it easy for consumers to have an aggregated shopping experience coupled with the convenience of a single method of payment. Their MO is to make it attractive to retailers to want to be part of their marketplaces. With more merchants, comes more consumers. With more consumers comes more third party wallets – AliPay and PayPal can be used offline as well as online outside of their marketplaces.

Alibaba, in particular, is doing a number of clever things in China today to get more AliPay users and retailers to sign-on. Their “Singles Day” in November, their March 8th shopping day and recent merchant and consumer funded taxi app subsidies are but three ways that they are assembling merchants and consumers around a shopping experience that pulls thru payment for their proprietary payment application.

Certainly, retailers will want to have their own mobile apps for all of the reasons that I mentioned earlier. But maybe the Wizard’s trick for getting consumers to download their apps is the promise of an omnichannel experience for their consumers via a payment method that moves seamlessly across devices and channels. At the moment, everyone, including the retailer, views retailer apps as a zero sum game. Maybe third party wallet providers are the ruby red slippers that help consumers find their way home to the retailers’ apps.