For most of the twentieth century, the most widely used non-cash payment form was checks. Now seen as relatively inefficient, check use overall has waned in favor of electronic methods with the goal of making the payment system more efficient, less time consuming and less costly. While there are many examples that support the move away from checks, at the end of the day, many companies still see hurdles in moving away from checks.

For most of the twentieth century, the most widely used non-cash payment form was checks. Now seen as relatively inefficient, check use overall has waned in favor of electronic methods with the goal of making the payment system more efficient, less time consuming and less costly. While there are many examples that support the move away from checks, at the end of the day, many companies still see hurdles in moving away from checks.

One group of organizations and individuals that is working together to promote greater use of B2B payments and electronic remittance data exchanges is The Remittance Coalition. They are working to change the fact that many small and medium enterprises lack a major incentive for to switch from paper checks due to, among other things, lack of resources and information

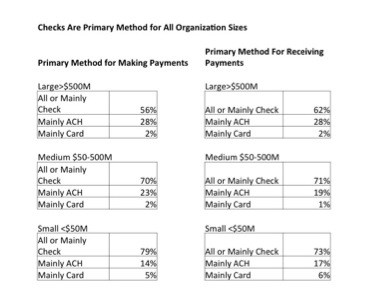

Their most recent study, dedicated to business with revenues of less than $2M, shows that almost all of them have checks or other options (presumably cash) as their primary accounts payable methods and for most of their accounts receivable methods as well. They go on to report that “90% of the smallest business respondents describe their internal processes and 86% describe their banking services as extremely or very effective in meeting their A/P needs (i.e., for making payments)”. In other words, most of the businesses in this segment pay with checks and think that it’s just a-okay to do so.

One of the remarkable aspects of the B2B switch from paper to e-payments is the amount of effort and resources required to make the transition.

For example, for an energy provider in the Midwest, Ameren, to go electronic, there had to be a big push for change with their suppliers. It took many 5 years, beginning with Ameren starting in 2008 to migrate a corporate credit card program to AP and promote the use of the cards. In 2009 a corporate procurement policy was implemented. One year later Ameren started to collect supplier’s ACH information. Then in 2011 an e-payable strategy was and since 2012 it has been further pushing for conversion from checks to e-payments. As a result checks share of payments dropped from 79.2% in 2006 to 13.5% in 2013 while the share of e-payments increased from 19.8% to 86.1%.

Naturally, we all know the benefits from using B2B e-payments include cost savings, improved cash flow financing and fraud control. However, there is an inverse relationship between the size of the firm (as measured per revenues) and the use of checks. The major difficulties for the implementation of e-payments in small businesses are lack of internal IT resources and the lack of back office systems and processes to support designing and then implementing a new way f working. These problems diminish with the size of the firm. This means small firms – unlike big corporations – would need to deploy resources on IT and back-offices as a first step before getting to e-payments.

The same study attempts to explain the causes behind small firms not switching from checks citing “lack of comparable services made available to larger businesses by vendors or banks, cost structures that disadvantage low payment volumes, lack of education about e-payments and e-remittance, or the lack of a perceived need.” Even further the study says “some small business customers do not see an ACH reconciliation service as a value-added service and are unwilling to pay extra for it”. This is evident in a business case about a small business experience with ACH which showed that the business could not access to all the details embedded in it (an ACH can contain much more data other than sums of money) due to him not signing to the bank’s special service which carried an extra-cost.

One of the Remittance Coalition objectives for 2014 is to open a dialog channel with software and technological vendors so that they can add features, which facilitate the adoption of e-payments. In this way the coalition aims to reduce the technological gap that there is between small businesses and large corporations and assist companies in the transition away from checks.