Walmart Pay Takes The Field

Remember that time Tim Cook said that 2015 was going to be the “year of Apple Pay?”

Well, it might have taken just about 11 months, but it looks like Walmart has formulated a response.

Sure, Walmart’s announcement today (Dec. 10) that it is taking the mobile payments playing field and launching its own proprietary payments platform was probably not much of a surprise, but what was was how it chose to do it.

Which was not to leverage MCX.

But to turn the Walmart.com app into the way that consumers can pay at the physical point of sale.

Using QR codes.

Which, Walmart Senior Vice President of Services Daniel Eckert told MPD CEO Karen Webster in an interview shortly after a briefing on the new product was held, makes total sense given how much mobile rules the roost when it comes to consumers’ shopping behavior.

“What Sam Walton taught us is that there is really only one boss and that is the customer. And they can fire us at any time by just not shopping with us anymore. So, you are probably seeing a healthy dose of just general paranoia about making sure we keep up with how fast customers are changing their preferences about how they want to shop with us,” Eckert told Webster during their conversation.

And while Eckert’s tone was light, Walmart’s announcement of Walmart Pay, which is rolling out today in Walmart’s HQ hometown, Bentonville, Arkansas, couldn’t be more serious.

In fact, Walmart’s buzzer-beater of a year-end announcement could sort of qualify as mobile payments’ 2015 Black Swan.

“This is about a laser focus on the customer, it really is,” Eckert told Webster. “We really have taken a lot of the things we see [in mobile payments] as being limiting and full of friction and really began with asking different questions. We decided to stop trying to improve payment for payments’ sake and instead use mobile to improve checkout and shopping.”

A far cry from how Walmart once thought it might own mobile payments. Like MCX, economics is at the heart of Walmart Pay.

But rather than a “holy war on interchange fees” with a focus on the cost side of the ledger, Walmart Pay, according to Eckert, is all about one and only one thing: making customers happy in its stores and making sales.

“[Walmart Pay] isn’t exclusively a payments discussion. We wanted to think much more holistically about how [payment] is brought to life,” Eckert noted.

And how it’s brought to life at Walmart could have some pretty interesting implications for the mobile payments landscape going forward.

So How Does It Work?

Walmart Pay, according to Eckert, was built to leverage a habit that its customers already know how to do really well: shop online at Walmart.com. With Walmart Pay, any of the tens of millions of customers who already make purchases on Walmart.com should be able to pay in pretty much exactly the same way in any one of Walmart’s 5,000 U.S. stores.

That means, using the Walmart.com app, a customer can use any payment method and any smartphone running any operating system to pay — something that Eckert said is unique to Walmart and offers the millions of customers who already use the Walmart.com app in the store a more convenient way to checkout.

“We have 22 million Walmart.com customers that are actively using the mobile app at our stores every month — that’s comScore’s stat, not ours. We think it’s more, but that is a big number. They are looking for a level of thoughtfulness about how retail can deliver for them with the tools that make their lives easier,” Eckert noted.

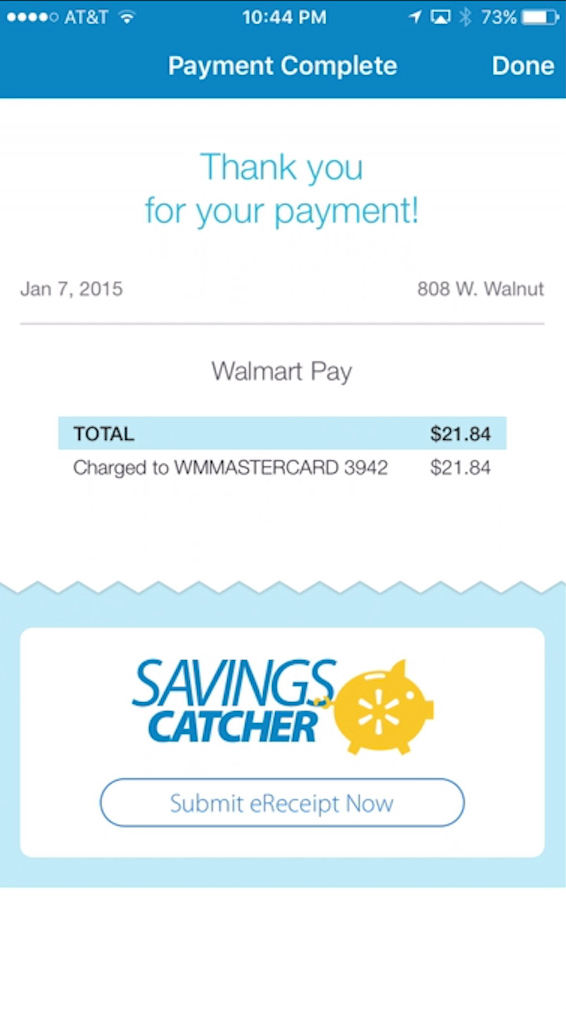

Eckert also said that making in-store checkout the equivalent of an in-store eCommerce experience took more than a few technical gymnastics. It delivers a simple and slick experience for the customers. Registration, he noted, takes about 30 to 45 seconds since it is nothing more than opening the app, logging in and tapping Walmart Pay. Cards registered to the app are what’s used to pay, which includes debit, credit, prepaid, gift cards and redemption of Savings Catcher savings. Other wallets, Eckert said, should they be desired by the consumer, are something that Walmart Pay may also support.

“Let’s leave open that some wallets are going to be widely adopted and customers may have a preferred type of mobile wallet they want to use across retail. Let’s allow those wallets to be a payment type within Walmart Pay,” Eckert noted, after having fielded several variations of questions from various reporters about whether Apple Pay might work in Walmart Pay (no direct answer was given, but we wouldn’t hold our breath).

What Walmart Pay can do right now is accommodate split payments, including among methods not currently compatible with Walmart Pay (cash, EBT, WIC) and/or any combination of those that are debit/credit, gift/prepaid and savings balances.

“A consumer can, with one tap, move their Savings Catcher dollars into Walmart Pay and add their gift card, and that will show as one amount in Walmart Pay,” Eckert noted. “Walmart Pay will also let the user decide what order the payments methods should be charged.”

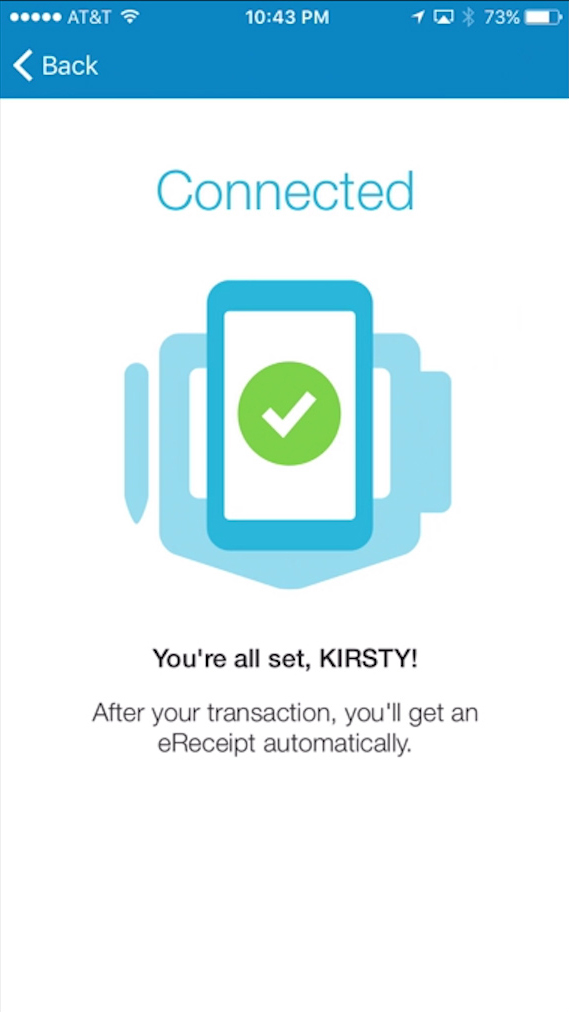

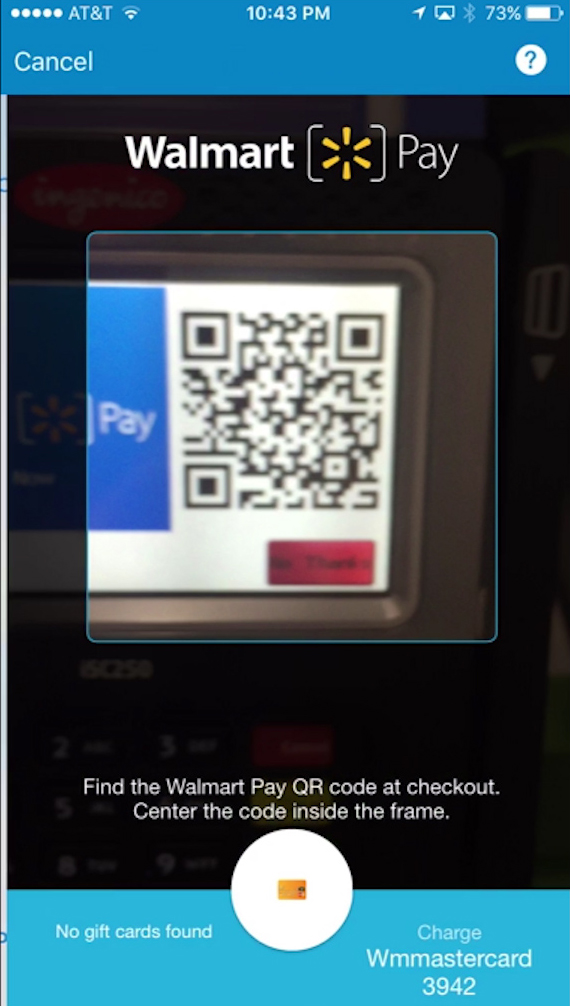

Once that setup is done and it’s time to checkout, Walmart Pay-ers use their phone’s camera to scan a dynamic QR code on the counter-facing terminals in checkout lanes (using either Touch ID or a PIN to authorize the scan), and the QR code connects the physical order to the consumer’s digital basket then applies the desired payments method in the cloud. Presto, the transaction is done. Once the QR code has been scanned, the consumer can put her mobile phone away.

“This is the same tech we use for Savings Catcher, so we know it deploys in an easily understandable and seamless way,” Eckert told Webster. “The thing we have heard most often when people use it is: ‘Is that it?’ It’s so fast, simple and easy that customers, we think, are really going to love this.”

And, Boy, Does Walmart Have A Lot Of Customers To Feel That Love

As we’ve seen now over a period of many years, igniting mobile payments is hard. No matter how slick the tech, how sleek the design or how clever their idea, many mobile payments schemes run into the exact same problem: Not enough merchants and consumers get excited enough about it to make it past first base.

Walmart is a bit different.

First, Walmart is an enormous merchant.

There are ~5,000 stores in the U.S. It is said that there is a Walmart within 15 minutes of 87 percent of the American population. On top of that, Walmart’s average revenue every 90 days beats Amazon’s revenue in its best performing year.

This enormous merchant has an enormous customer base.

Walmart reports that 140 million consumers (or 77 percent of the U.S. adult population) visit its physical stores each week. Online, in November and December alone, Walmart.com is anticipating 210 million visits, up from 18 million two years ago. The Walmart app ranks among the Top 3 retail apps in the Google and Apple app stores every month. During the Thanksgiving weekend, half of Walmart’s mobile sales came via mobile — a stat, Eckert noted, that is much higher than average for retailers.

Walmart is in the enviable position as a new mobile payments entrant of starting out by having both sides of its platform on board.

And it’s perhaps even one of the most serious mobile payments contenders to enter the fray in a while.

If Walmart Pay works as advertised, it will show every other large merchant how to do the exact same thing, giving merchants a whole new option to consider. And although Eckert emphasized that Walmart Pay is different than MCX and that Walmart remains committed to it, the whole situation surrounding MCX’s future just got a little more interesting — and even a bit muddier, it seems.

If Walmart Pay works as advertised, it could also become card networks’ worst nightmare.

Today, Walmart Pay allows payment by any card, any type. Over time, you gotta believe that those consumers will be incentivized to move to ACH payments. If the networks are worried about PayPal moving consumers to ACH, Walmart Pay should positively terrify them.

And Walmart Pay certainly underscores that app-based and cloud-based mobile payments are far from dead. NFC seems less and less like the slam dunk at the point of sale that it once did.

Thanks to Walmart, the mobile payments race, far from being decided in 2015, might have just gotten really, really interesting right at the end.