Higher capital requirements may have a negative ripple effect on banks — tightening the lending spigots even further.

And the winners may be the FinTechs that gain more lending business from consumers and enterprises as they pivot to a relatively newer corner of financial services to get the capital they need.

As has been widely reported, the Federal Reserve is proposing higher — and thus more stringent — bank capital requirements.

The move would be one designed to ensure that banks with at least $100 billion in assets on the books hold an additional 2% of capital — which in turn, means that $2 for every $100 in assets would be held back.

As to the ripple effects, holding more capital means that banks have more in the coffers to deal with exogenous shocks. But the more money that is held back, the less money there is to lend into the general financial system. And to generate at least some of the profits that would otherwise be lost by keeping more capital in reserve, banks might opt to hike rates.

Looking Down the Road

There’s at least some discussion of what might happen down the road. Banks, of course, have kicked off earnings season by discussing possible capital-related impact.

And as noted on the most recent conference call with analysts, JPMorgan Chief Financial Officer Jeremy Barnum said that higher capital requirements could lead to the “possibility of a repricing of products and services, which, of course, goes back to our point that these capital increases do have impacts on the real economy… a little bit of a straight-up across-the-board tax on everything.”

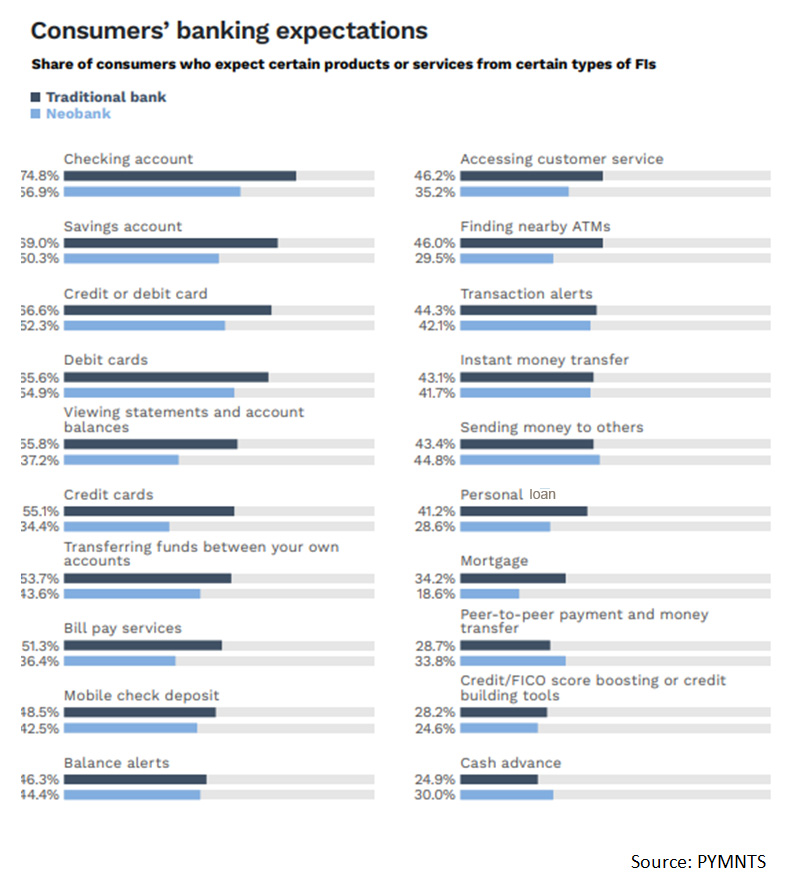

The competitive landscape may get more heated as traditional FIs and digital-only neobanks jockey for deposits and, by extension, lending activity. As detailed in the report “How Consumers Use Digital Banks,” done in collaboration with Treasury Prime, we found that fewer than 10% of consumers have opted to use FinTechs as their primary banks. But the survey of 2,124 U.S. consumers also found that as many as 50% see themselves using FinTechs as a home base for savings accounts and that about 29% would tap these digital-only players for personal loans. The interest is there, as detailed in the chart below.

The competitive edge may be in place for FinTechs to make inroads with younger consumers. As detailed in a separate report, roughly 60% of millennials report having subprime credit scores — and as FinTechs create new credit channels with alternative data sources, they can cement loyalty for those consumers at a relatively young age. Companies like Pismo, Foro, and other FinTechs have been in the news and are busy announcing their lending features and products. With new capital requirements on the horizon, the banks may feel a bit of competition nipping at their heels.