The ranks are thinning at FinTech firms.

In a week that’s seen its share of earnings announcements and a fourth rate hike from the Federal Reserve, a spate of layoffs also rocked the sector, including a few members of the FinTech IPO Index.

The cuts are a response to a macro climate that scarcely could have been predicted a year ago. The fact that mortgage rates are now at multi-decade highs has done no favors to platforms that promised to disrupt the housing industry, and particularly how the financing of buying and selling is done. It’s no longer a buyer’s market or a seller’s market — indeed, it’s tough to see whose market it is at all.

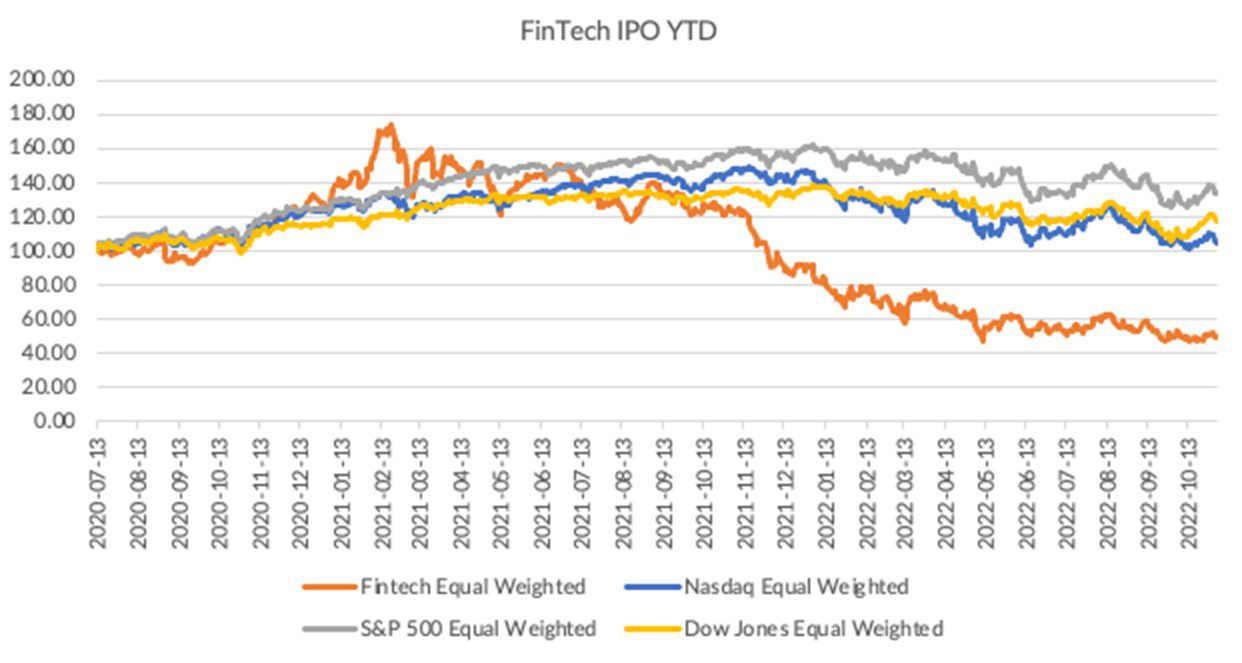

Headed into Friday’s (Nov. 4) session, the Index, overall, was 2.7% lower.

Upstart cut staff, stating in filings it had eliminated 140 positions — about 7% of its staff — due to a “challenging economy” that in turn is reducing loan volumes. The staffers, according to the 8-K with the SEC, had been focused on helping to process loan applications. The stock sank 15%.

Opendoor Technologies’ stock was down 11%. In a blog post Wednesday (Nov. 2), CEO Eric Wu said that the company was laying off 18% of its staff, or 550 individuals.

“The reality is, we’re navigating one of the most challenging real estate markets in 40 years and need to adjust our business,” said Wu. The announcement came against a backdrop where mortgage rates are touching levels not seen in 40 years and the surge is negatively impacting the real estate market in general. Opendoor operates a platform focused on acquiring and selling properties.

Earnings Parade Continues

Beyond those staffing cuts, earnings continue to roll in. At least among some of the platforms — the ones that are not exposed to rate sensitive verticals (like housing) or have a diversification of revenue streams — the current economy’s impact has been notably more sanguine.

Sofi reported this week that its “one-stop shop” approach to finance, checking and personal loans continues to gain traction. The company said deposits soared by 86%, reaching $5 billion at the end of the quarter.

CEO Anthony Noto said the company is taking deposit share from traditional banks as it offers higher APY than other players by virtue of its bank charter — the rate stood at 2.5% during the quarter, and that rate is now being boosted to 3% as soon as this week.

Demand for personal loans continues to be strong, too, Sofi management said. Originations increased 71% year-on-year to $2.8 billion. SoFi new member additions stood at about 424,000, and at the quarter’s end total members stood at 4.7 million, up 61% year-on-year. The stock’s been volatile, rocketing 18% during intraday trading immediately after results were posted, and yet settling roughly flat through the past five sessions.

Remitly’s own results, released on Wednesday (Nov. 2), showed that active customers were up 49% to 3.8 million year-over-year; and send volume was up 44% year-over-year to $7.5 billion.

NerdWallet’s Wednesday release of its own results helped send shares soaring more than 37% on Thursday (Nov. 3) alone, and 26% through the week. Credit card-related revenue was up 59% year-on-year, while loans revenue was off 12%, tied in part to a decline in mortgage-related demand. Total average monthly unique users were up 11% to 19 million.

Separately, OneConnect shares sank 19% this week. The fall came after the company announced that it received a letter from the New York Stock Exchange saying it was below the NYSE’s continued listing standards due to the trading price of OneConnect’s American depositary shares (though there is no immediate impact on the listing of the ADS themselves).