Only one in four credit card holders and one in 10 debit card holders say their banks provide that option. There are also 10.7 percent of credit card holders and 3.1 percent of debit card holders who are given the option of earning special rates for use at hotel chains, and only 6.6 percent of credit card holders and 1.5 percent of debit card holders who say they are given the option to earn rewards that would allow them to get VIP access at airport lounges.

The rarity with which financial institutions (FIs) offer such rewards could come at a real cost. PYMNTS research shows that roughly one in every five consumers is not only willing, but very or extremely likely to leave their current FIs for competitors if it means being able to access the types of rewards programs they want. It is therefore critical for FIs to provide consumers’ rewards programs of choice if they want to retain loyal customers and sign new cardholders.

The rarity with which financial institutions (FIs) offer such rewards could come at a real cost. PYMNTS research shows that roughly one in every five consumers is not only willing, but very or extremely likely to leave their current FIs for competitors if it means being able to access the types of rewards programs they want. It is therefore critical for FIs to provide consumers’ rewards programs of choice if they want to retain loyal customers and sign new cardholders.

So which types of rewards programs do cardholders really want? And which consumers are most likely to be persuaded by access to them?

In the Cardholder Loyalty Engagement Report: How Rewards Programs Give FIs A Top-Of-Wallet Advantage, PYMNTS, in collaboration with novae, aims to understand which types of loyalty and rewards programs FIs must provide to meet consumers’ expectations, retain existing customers and boost their chances of earning new ones. We surveyed 2,115 U.S. consumers to get a first-hand account of what they want from their FIs’ credit and debit cards rewards programs and what FIs risk by not providing them.

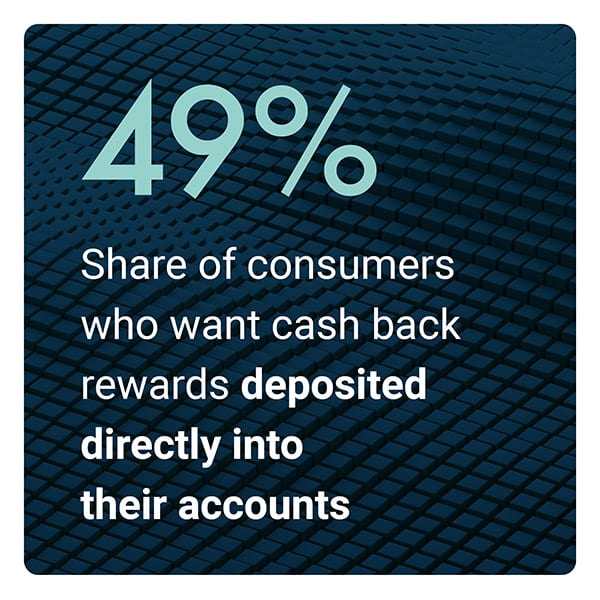

PYMNTS research shows that cash back is the most in-demand type of reward FIs can offer, with 48.7 percent of consumers saying they want to be able to earn cash back that can be deposited directly into their bank accounts and 45.5 percent expressing interest in being able to earn cash back that they can apply to help pay for their immediate purchases. This compares to 38.4 percent of consumers who want to earn points they can spend on the products of their choosing and 24 percent who want to be able to spend them at the stores of their choosing.

It is also clear that different generations and income brackets tend to gravitate toward particular types of rewards programs. Millennials are the most likely to want to be able to earn points they can apply to their immediate purchases, for example, with 51.5 percent saying they would like to use a rewards program that allowed them to do so. This compares to 41.1 percent of baby boomers and seniors and 46.5  percent of Generation X.

percent of Generation X.

Generation Z is the most likely to want to earn points they can spend at stores of their choice, by contrast. PYMNTS research shows that 33.1 percent want to do so, compared to 27.1 percent of millennials. Adopting different types of rewards programs will therefore tend to attract very different types of cardholders.

The relationship between cardholders and their desire to use specific rewards programs is far more complex than a matter of generation gaps, however. The Cardholder Loyalty Engagement Report: How Rewards Programs Give FIs A Top-Of-Wallet Advantage details why.

To learn more about how FIs can use rewards programs to boost cardholder engagement and loyalty, download the report.

Loyalty and rewards programs have long been a common way for banks to persuade consumers to sign up for and use their credit and debit cards, but a surprisingly few number of cardholders say they are offered the types of rewards programs they really want.

Loyalty and rewards programs have long been a common way for banks to persuade consumers to sign up for and use their credit and debit cards, but a surprisingly few number of cardholders say they are offered the types of rewards programs they really want.