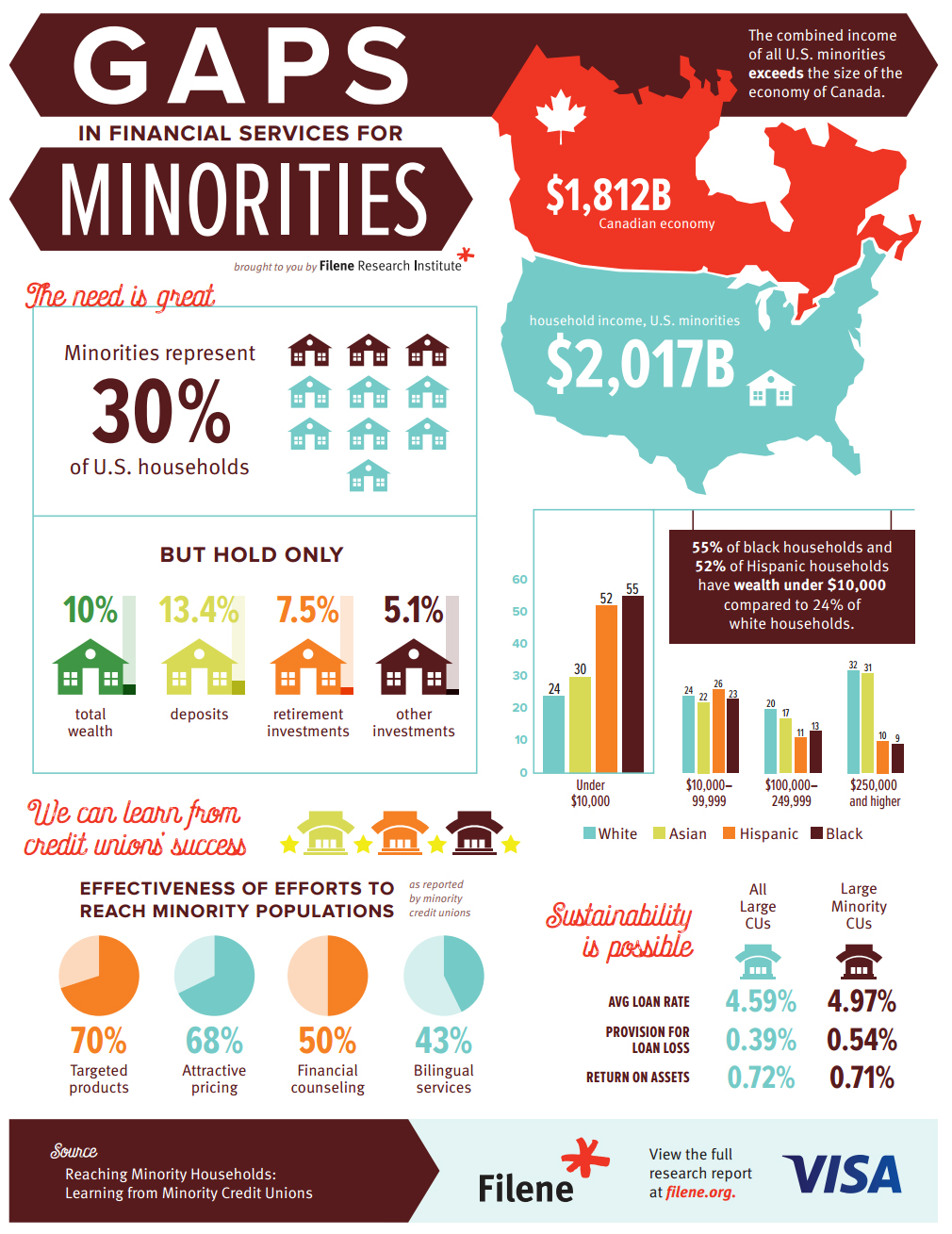

As research from Filene, titled “Reaching Minority Households: Learning from Minority Credit Unions” shows, minorities, though relatively less wealthy than non-minorities, are indeed significant stakeholders and customers for non-minority-owned and run financial providers, and they have a history of using several different financial services products. For instance, noted Filene, these households accounted for 13 percent of the national total holdings of deposit funds, at nearly $260 billion; and 25 percent of home mortgages, at $1.7 trillion; and 26 percent of nationally held credit card debt, or $236 billion.

And yet, according to the survey, there’s a “wealth gap” in the works, with a threshold of less than $10,000 in wealth being reported by more than half of African American and Hispanic households, at a respective 55 percent and 52 percent. Drilling down a bit farther, the saved-up wealth is higher among Caucasians, where only 24 percent of those households report less than $10,000 in wealth held.

The impact, then, is that life’s emergencies are considerably more financially dire for minorities than for non-minorities. Taking out loans to deal with those emergencies, or if loans are already in place, means that payback of principle and keeping up with interest payments becomes an arduous and at times impossible task. The vicious cycle continues as consumers, unable to get the discounts that might otherwise be available to them were they able to buy greater quantities (of everything, notes the research, from groceries to bank accounts), must settle for terms that may be tougher to honor.

By default, found Filene, as financial service firms that could be considered more marquee do not offer favorable terms on smaller purchases, many minorities thus chose to go around the “financial gap” by bringing their business to minority-focused institutions that include more than 820 credit unions with $53 billion in assets on the books (13 percent of the industry total).

Those institutions have a direct view of income and wealth swings, with higher delinquencies at 1.1 percent of loans, roughly 30 basis points higher than non-minority credit unions. In part to compensate, minority credit unions charge rates or about 5.4 percent, about 90 basis points higher than others. However, as the data show, returns on assets are similar between non-minority and minority credit unions. This implies that the firms have figured out a way to be valuable to their consumers – and also the consumers have found prospective rates similar at non-minority and minority firms.

Among the key efforts that could be constructive to non-minority institutions: targeting products to lower income households, financial education and financial literacy workshops. What shouldn’t be top of list for successful overtures: simply opening new branches, or simply offering assistance via government agencies.

To learn more about this study take a look at the infographic “Reaching Minority Households: Learning from Minority Credit Unions.”