The rise of embedded finance means that just about every consumer-facing app can create an account capable of receiving a deposit and making a payment, and even more consumers will open them.

But keeping those accounts active will depend on issuers making it easy to move money safely, securely and to whatever endpoint consumers want, Ingo Money’s CEO Drew Edwards and Executive Vice President and Chief Product Officer Lisa McFarland told PYMNTS’ Karen Webster.

“There are a lot of things that consumers need to and want to do with their money,” McFarland said. “Enabling that capability, and enabling it in a frictionless way, is a reason for them to engage with you more.”

Yet, as Edwards observed, all those payment choices are now being cobbled together. Issuers have to deal with old school mediums like checks, wires and cash, while also solving for the new digital mediums like The Clearing House, the Federal Reserve (FedNow is on the horizon), PayPal, Venmo and Amazon. And what about products that involve moving money, like bill pay and peer-to-peer (P2P) and B2B payments?

“I’ve lost count of how many apps I have on my phone that are holding money, and every time you add one — well, that becomes another choice where I might want to move money to or from,” Edwards said.

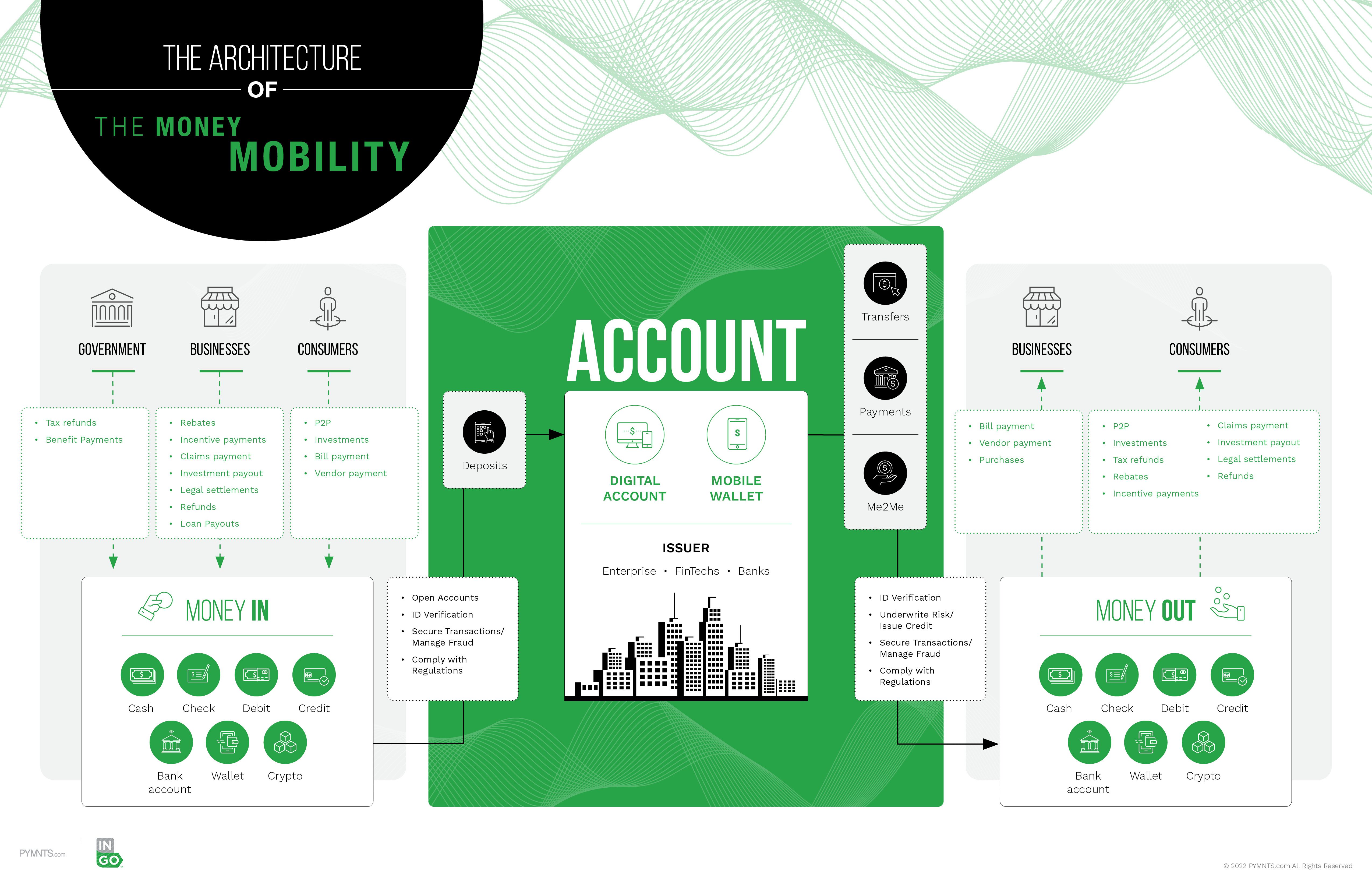

Although issuers have been focused on making sure that money can be moved out of accounts to a variety of endpoints with confidence, it’s become imperative to make sure that money can be just as easily moved into accounts.

Advertisement: Scroll to Continue

Edwards noted that “the actual execution of true choice and ubiquity is complicated, because it involves managing relationships, either proprietary or ‘network of network’ relationships, across all kinds of different rule sets and all kinds of different methods.”

Too Many Cooks in the Kitchen

Different companies are approaching money mobility from their strong suits, but there are too many cooks in the kitchen, as Edwards sees it, and it’s causing unnecessary drag.

Asked how issuers are solving for mobility in a more congested collection of tools, he noted, “They’re stitching stuff together, one partner at a time, one vendor a time, and I think that’s a mistake, because of fraud. If you can’t see the whole picture, then it’s hard to control the bad actors. It’s really hard to offer great customer experiences and control the risk at the same time.”

In short, money mobility is a complex, and sometimes risky, endeavor. The protocols for authentication, fraud monitoring, chargebacks and all manner of business processes can vary widely depending on where you look.

Rethinking the Value Prop

Edwards’ comments reflect Ingo’s take on the need for issuers to rethink their value to their accountholder: The friend who’s getting a P2P payment from you, for example, should be able to choose how they get it. A consumer with multiple accounts should be able to move money into, between and among each of those accounts with instant money choices.

Along the way, we’ll see the rise of a new money mobility ecosystem that gives issuers the ability to accept deposits from any funding source using any payment method — and gives accountholders the ability to move those funds anywhere they wish.

From increased engagement comes coveted top-of-wallet status, Edwards said, which may give a leg up for traditional players that have been jousting with digital-only upstarts.

“The rise of neobanks and super apps is really raising the bar for all issuers to deliver that sort of frictionless money mobility experience,” he explained.

Banks used to make it a difficult experience to open accounts, Edwards noted, with a slew of paperwork involved and regulatory checks done on-site. Consumers also had to fund accounts before they left the branch.

However, he said that the digital-first companies have winnowed down an account opening process that used to take hours (or days) into minutes.

“That account opening process got super-slick,” Edwards said. “Now you have to solve for the rest of it, the moving money in and out, day in and day out, and all of those entities are lacking branches or lacking many of the normal tools, such as ATMs.”

See also: 2022’s Next Big Thing: Solving the ‘Money Mobility’ Problem

McFarland added that for the issuers, the urgency to streamline money-in processes is there: After all, you can’t spend or invest with an account if you can’t fund it. No payment method can be truly ubiquitous unless that two-way street — inbound and outbound — is well-established.

As McFarland told Webster, “Inbound funding is just as important, and for many issuers, that’s becoming a real area of focus for them.”

Guarding Against Fraud

Edwards said that all too often, many firms — especially digital ones — are getting into payments, offering endpoints while focusing purely on connectivity, touting easy application programming interfaces (APIs) and developer forward solutions.

But it’s when the funds start to flow that they see the danger. At first glance, inbound account transfers should not be tougher or riskier than selling the proverbial toaster, but that danger is real, McFarland explained.

“With real-time funds in a digital environment, if you’re an issuer of an account, you want that ability to be able to have someone transfer funds from an account they own already into their new account, which has historically been a very risky transaction, and the risk of that transaction is actually one we’re going to solve very soon,” McFarland said.

Inbound fraud from cards presents yet another wrinkle, as stolen identities and card credentials flood the dark web and are responsible for billions of dollars in fraud annually. There’s the risk, too, of friendly fraud, said Edwards — where consumers simply stating that they did not authorize a transaction is enough to get it reversed.

Of Ingo’s own experience, he said, “We pay out a lot of insurance claims, and there are people who simply say, ‘I did not get my money.’ The risk is whether you [paid out] to the right person.”

See also: 33% of Consumers Will Pay a Fee for Instant Access to Payouts

Mobility Means Utility in the Connected Economy

In the end, money mobility is about providing utility and convenience to account holders.

With instant and near-instant methods injecting more fraud potential into transactions, McFarland said it can be easier talking about money mobility needs with companies that have been burned by fraud inherent in new and faster systems.

McFarland said that “becomes a very easy conversation to have, because it’s an experience that they’ve undergone. They may come to us [asking], ‘How can you guys do this and control the fraud? How can you do this and protect me? Can we get the service from you in a way that you’ll guarantee the transactions?’

“What my team does is to look at how we can deliver those kinds of solutions to our partners,” she said.

Those solutions are needed as money mobility becomes a more important part of customer experience in 2022 and beyond.

As Edwards told Webster, “We think the new ‘sticky’ is frictionless money mobility. Those players that make that the best experience and the easiest to move money in and out of an account are the ones that’ll win the hearts and mind of those account holders.”

See also: New Study: Instant Disbursements an Instant Winner With Consumers