Keeping Pace In An Accelerating Payments Race

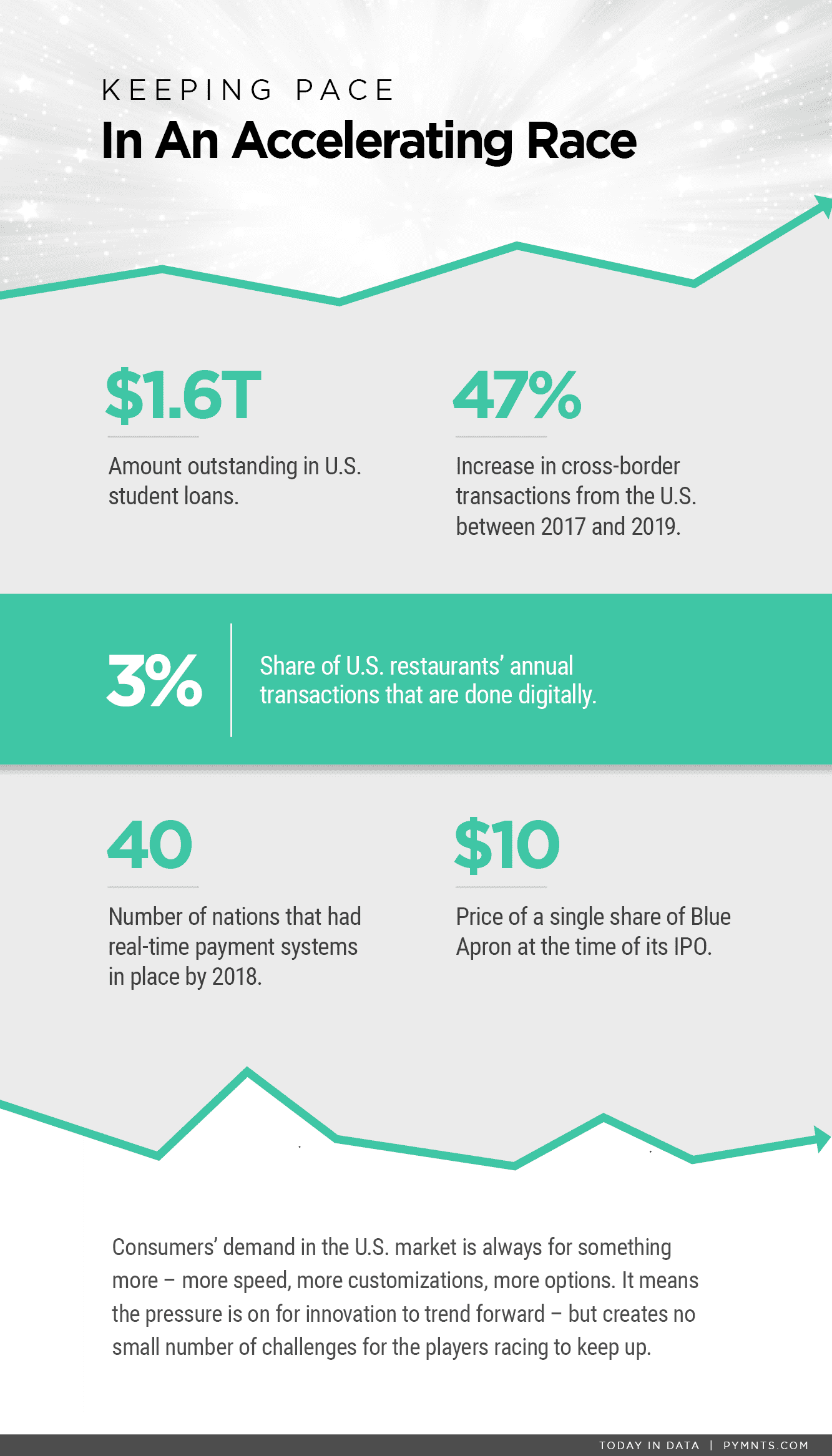

The U.S. is known for, among other things, being a “more is more” kind of place. Sometimes that is a good thing (case in point: our $1 trillion-a-year restaurant industry). Sometimes, not so much (check out our student debt numbers). The question for U.S. merchants and payments players is how to offer up more – more speed, more service options – and then make those options scalable and exportable. And, for good measure, to future-proof them against markets that tend to swing wildly.

Data:

Data: